What is Global Near Infrared (NIR) Analyzers Market?

The Global Near Infrared (NIR) Analyzers Market refers to the worldwide industry focused on the development, production, and application of NIR analyzers. These devices utilize near-infrared light to analyze the composition of various materials, providing rapid and non-destructive testing capabilities. NIR analyzers are widely used in industries such as pharmaceuticals, food and agriculture, polymers, and oil and gas, among others. They help in determining the chemical and physical properties of substances, ensuring quality control, and optimizing production processes. The market for NIR analyzers is driven by the increasing demand for efficient and accurate analytical techniques, advancements in technology, and the growing need for regulatory compliance in various industries. As a result, the Global NIR Analyzers Market is expected to witness significant growth in the coming years, with a focus on innovation and expanding applications across different sectors.

FT - NIR(Interferometer), Others(AOTF,Filter) in the Global Near Infrared (NIR) Analyzers Market:

Fourier Transform Near Infrared (FT-NIR) analyzers, based on interferometer technology, are a significant segment within the Global Near Infrared (NIR) Analyzers Market. FT-NIR analyzers utilize an interferometer to modulate the infrared light, producing an interferogram that is then transformed into a spectrum using Fourier Transform algorithms. This technology offers high resolution, accuracy, and sensitivity, making it ideal for complex sample analysis. FT-NIR analyzers are widely used in various industries, including pharmaceuticals, food and agriculture, and polymers, due to their ability to provide detailed molecular information and detect minor components in mixtures. Another segment within the NIR analyzers market includes analyzers based on Acousto-Optic Tunable Filters (AOTF) and filter-based technologies. AOTF-based NIR analyzers use acousto-optic devices to selectively filter specific wavelengths of light, allowing for rapid and precise spectral measurements. These analyzers are known for their robustness, speed, and ability to handle a wide range of sample types. Filter-based NIR analyzers, on the other hand, use optical filters to isolate specific wavelengths of light, providing a simpler and cost-effective solution for routine analysis. These analyzers are commonly used in applications where high throughput and ease of use are essential. Both AOTF and filter-based NIR analyzers offer advantages such as compact design, low maintenance, and suitability for on-site and in-line analysis. The choice between FT-NIR, AOTF, and filter-based analyzers depends on the specific requirements of the application, including the level of detail needed, sample complexity, and operational environment. Overall, the Global Near Infrared (NIR) Analyzers Market is characterized by a diverse range of technologies, each offering unique benefits and catering to different industry needs. As technology continues to advance, the market is expected to see further innovations and improvements in NIR analyzer performance, expanding their applications and driving growth across various sectors.

Polymer Industry, Food and Agriculture Industry, Pharmaceutical Industry, Oil and Gas, Others in the Global Near Infrared (NIR) Analyzers Market:

The Global Near Infrared (NIR) Analyzers Market finds extensive usage across multiple industries, including the polymer industry, food and agriculture industry, pharmaceutical industry, oil and gas sector, and others. In the polymer industry, NIR analyzers are used to monitor the composition and quality of raw materials, intermediates, and finished products. They help in identifying polymer types, measuring moisture content, and detecting contaminants, ensuring consistent product quality and optimizing production processes. In the food and agriculture industry, NIR analyzers play a crucial role in assessing the quality and safety of food products. They are used to analyze the nutritional content, moisture levels, and adulterants in various food items, including grains, dairy products, meat, and beverages. NIR analyzers also aid in precision agriculture by providing real-time data on soil composition, crop health, and yield prediction, enabling farmers to make informed decisions and improve productivity. In the pharmaceutical industry, NIR analyzers are employed for quality control and assurance throughout the drug development and manufacturing process. They help in identifying active pharmaceutical ingredients (APIs), monitoring blend uniformity, and ensuring the consistency of tablet coatings. NIR analyzers also support regulatory compliance by providing non-destructive testing methods that meet stringent industry standards. In the oil and gas sector, NIR analyzers are used to analyze the composition of crude oil, natural gas, and refined products. They help in determining the quality and purity of hydrocarbons, monitoring process parameters, and optimizing refining operations. NIR analyzers also assist in detecting contaminants and ensuring compliance with environmental regulations. Other industries that benefit from NIR analyzers include textiles, chemicals, and environmental monitoring. In textiles, NIR analyzers are used to identify fiber types, measure moisture content, and assess dye quality. In the chemical industry, they help in analyzing raw materials, intermediates, and final products, ensuring consistent quality and process efficiency. In environmental monitoring, NIR analyzers are used to detect pollutants, analyze soil and water samples, and monitor air quality. Overall, the Global Near Infrared (NIR) Analyzers Market offers versatile and reliable analytical solutions that enhance quality control, process optimization, and regulatory compliance across various industries.

Global Near Infrared (NIR) Analyzers Market Outlook:

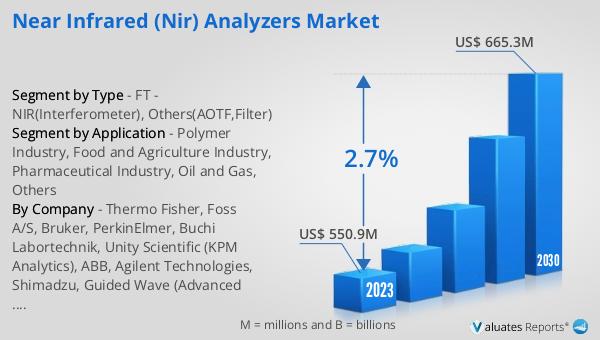

The global Near Infrared (NIR) Analyzers market is anticipated to grow significantly, reaching an estimated value of US$ 665.3 million by 2030, up from US$ 567 million in 2024, with a compound annual growth rate (CAGR) of 2.7% between 2024 and 2030. North America currently holds the largest share of the market, accounting for approximately 54%, followed by Europe with about 34%. The market is characterized by a high level of competition, with the top three companies collectively occupying around 41% of the market share. This competitive landscape is driven by the increasing demand for advanced analytical solutions across various industries, including pharmaceuticals, food and agriculture, polymers, and oil and gas. Companies are focusing on innovation, technological advancements, and expanding their product portfolios to meet the evolving needs of their customers. The growth of the NIR analyzers market is also supported by the rising awareness of the benefits of NIR technology, such as non-destructive testing, rapid analysis, and high accuracy. As industries continue to prioritize quality control, process optimization, and regulatory compliance, the demand for NIR analyzers is expected to increase, driving further market growth.

| Report Metric | Details |

| Report Name | Near Infrared (NIR) Analyzers Market |

| Accounted market size in 2024 | an estimated US$ 567 million |

| Forecasted market size in 2030 | US$ 665.3 million |

| CAGR | 2.7% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Thermo Fisher, Foss A/S, Bruker, PerkinElmer, Buchi Labortechnik, Unity Scientific (KPM Analytics), ABB, Agilent Technologies, Shimadzu, Guided Wave (Advanced Group), Jasco, ZEUTEC, Sartorius, Yokogawa Electric |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |