What is Global Oil-Free Compressors Market?

The Global Oil-Free Compressors Market refers to the worldwide industry focused on the production and distribution of compressors that operate without the use of oil. These compressors are designed to provide clean, contaminant-free air, making them ideal for applications where air purity is crucial. Unlike traditional compressors that use oil for lubrication and cooling, oil-free compressors use alternative methods such as water or air cooling, or advanced materials that reduce friction and wear. This market is driven by the increasing demand for high-quality compressed air in various industries, including healthcare, food and beverage, electronics, and pharmaceuticals. The need for energy-efficient and environmentally friendly solutions also fuels the growth of this market. As industries continue to prioritize sustainability and regulatory compliance, the adoption of oil-free compressors is expected to rise, making this a significant segment within the broader compressor market.

Rotary Screw Compressors, Reciprocating Type, Centrifugal Type, Others in the Global Oil-Free Compressors Market:

Rotary Screw Compressors, Reciprocating Type, Centrifugal Type, and others are key categories within the Global Oil-Free Compressors Market. Rotary Screw Compressors are widely used due to their efficiency and reliability. They operate by using two helical screws that rotate in opposite directions, compressing the air as it moves through the chamber. This type of compressor is known for its continuous operation and ability to deliver a steady flow of compressed air, making it suitable for industrial applications where a constant air supply is essential. Reciprocating Type compressors, on the other hand, use a piston-driven mechanism to compress air. These compressors are typically used in applications requiring high pressure and are known for their durability and ability to handle intermittent duty cycles. They are often found in smaller-scale operations or where portability is a factor. Centrifugal Type compressors use a high-speed rotating impeller to impart velocity to the air, which is then converted into pressure. These compressors are ideal for large-scale industrial applications due to their ability to produce high volumes of compressed air with minimal maintenance. They are commonly used in power generation, petrochemical, and large manufacturing plants. Other types of oil-free compressors include scroll compressors and diaphragm compressors. Scroll compressors use two interleaving scrolls to compress air, offering a compact and quiet solution ideal for medical and laboratory applications. Diaphragm compressors use a flexible diaphragm to compress air, providing a contamination-free solution suitable for applications requiring ultra-pure air. Each type of oil-free compressor has its unique advantages and is chosen based on the specific requirements of the application, such as the desired pressure, flow rate, and air purity. The diversity in compressor types ensures that there is a suitable solution for a wide range of industrial and commercial needs, contributing to the overall growth and development of the Global Oil-Free Compressors Market.

Chemical Industry, Oil & Gas Industry, Power Generation, Electronics Industry, Medical and Pharma., Food and Beverage Industry, Automobile & Auto Ancillaries, Others in the Global Oil-Free Compressors Market:

The Global Oil-Free Compressors Market finds extensive usage across various industries, each with specific requirements for clean and efficient compressed air. In the Chemical Industry, oil-free compressors are essential for processes that require contaminant-free air to ensure product purity and prevent chemical reactions that could be triggered by oil particles. These compressors are used in applications such as pneumatic conveying, air separation, and chemical synthesis. In the Oil & Gas Industry, oil-free compressors are used for gas compression, pipeline transportation, and offshore drilling operations. The absence of oil in the compressed air is crucial to prevent contamination of the gas and ensure the safety and efficiency of the operations. In Power Generation, oil-free compressors are used for instrument air, cooling, and other auxiliary processes. The reliability and efficiency of these compressors are vital for maintaining continuous power plant operations. The Electronics Industry relies on oil-free compressors for manufacturing processes that require ultra-pure air, such as semiconductor production and cleanroom environments. Any contamination in the air can lead to defects in electronic components, making oil-free compressors a critical component in this industry. In the Medical and Pharmaceutical sectors, oil-free compressors are used for applications such as respiratory equipment, dental tools, and pharmaceutical manufacturing. The need for sterile and contaminant-free air is paramount to ensure patient safety and product quality. The Food and Beverage Industry uses oil-free compressors for packaging, bottling, and food processing applications. The absence of oil in the compressed air prevents contamination of food products, ensuring compliance with health and safety regulations. In the Automobile and Auto Ancillaries sector, oil-free compressors are used for painting, assembly, and testing processes. The clean air provided by these compressors ensures high-quality finishes and prevents defects in automotive components. Other industries that benefit from oil-free compressors include textiles, pulp and paper, and aerospace, where the need for clean and efficient compressed air is critical for various manufacturing and operational processes. The versatility and reliability of oil-free compressors make them an indispensable tool across these diverse industries, driving their adoption and growth in the global market.

Global Oil-Free Compressors Market Outlook:

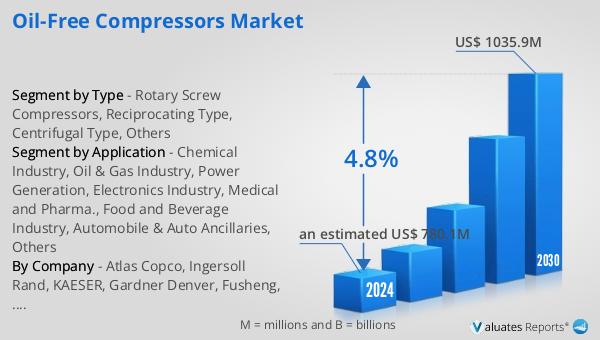

The global Oil-Free Compressors market is anticipated to grow significantly, reaching an estimated value of US$ 1035.9 million by 2030, up from US$ 780.1 million in 2024, with a compound annual growth rate (CAGR) of 4.8% during the period from 2024 to 2030. The market is dominated by five major manufacturers: Atlas Copco, Ingersoll Rand, Hitachi, Kobelco, and Fusheng, which collectively account for over 60% of the market share. Among these, Atlas Copco leads the market with nearly 40% of the production value share, followed by Ingersoll Rand with 20%, and Hitachi with 7%. The Asia-Pacific region holds the largest market share, exceeding 40%, followed by Europe and North America, which hold shares of 27% and 20%, respectively. Rotary Screw Compressors are the leading type within the market, holding a market share of over 55%. The Chemical Industry is the largest segment, accounting for over 15% of the market. This growth is driven by the increasing demand for clean and efficient compressed air solutions across various industries, as well as the ongoing advancements in compressor technology that enhance performance and energy efficiency. The market's expansion is also supported by the growing emphasis on sustainability and regulatory compliance, which encourages the adoption of oil-free compressors.

| Report Metric | Details |

| Report Name | Oil-Free Compressors Market |

| Accounted market size in 2024 | an estimated US$ 780.1 million |

| Forecasted market size in 2030 | US$ 1035.9 million |

| CAGR | 4.8% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Atlas Copco, Ingersoll Rand, KAESER, Gardner Denver, Fusheng, Kobelco, Boge, Aerzen, Mitsui, Hitachi |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |