What is Global Pianoforte Market?

The global Pianoforte market is a dynamic and evolving sector that encompasses the production, distribution, and sale of pianos worldwide. This market includes various types of pianos such as grand pianos, upright pianos, digital pianos, and hybrid pianos. The demand for pianos is influenced by several factors including cultural trends, economic conditions, and advancements in technology. The market is driven by a growing interest in music education, the popularity of live performances, and the increasing use of pianos in entertainment and media. Additionally, the rise of digital and hybrid pianos has expanded the market by offering more affordable and versatile options for consumers. The global Pianoforte market is characterized by a mix of established brands and new entrants, with competition based on factors such as quality, price, and innovation. The market is also influenced by regional preferences and the availability of skilled labor for piano manufacturing. Overall, the global Pianoforte market is a vibrant and competitive industry that continues to adapt to changing consumer preferences and technological advancements.

Grand Piano, Upright Piano in the Global Pianoforte Market:

Grand pianos and upright pianos are two of the most prominent types of pianos in the global Pianoforte market. Grand pianos are known for their large size, horizontal frame, and superior sound quality. They are often used in concert halls, recording studios, and high-end residential settings. The grand piano's design allows for longer strings and larger soundboards, which produce a richer and more resonant sound. This makes them the preferred choice for professional musicians and serious piano enthusiasts. On the other hand, upright pianos are more compact and have a vertical frame, making them suitable for smaller spaces such as homes, schools, and smaller performance venues. Despite their smaller size, modern upright pianos are designed to deliver high-quality sound and are often used for practice, teaching, and casual playing. The global Pianoforte market sees a significant demand for both types of pianos, with upright pianos holding a larger share due to their affordability and space-saving design. The choice between a grand piano and an upright piano often depends on the intended use, available space, and budget. Both types of pianos have their unique advantages and cater to different segments of the market. Grand pianos are typically more expensive and are considered a long-term investment, while upright pianos offer a more accessible entry point for beginners and casual players. The global Pianoforte market continues to innovate with new designs and technologies, ensuring that both grand and upright pianos remain relevant and appealing to a wide range of consumers.

Performance, Learning and teaching, Entertainment in the Global Pianoforte Market:

The global Pianoforte market plays a crucial role in various areas such as performance, learning and teaching, and entertainment. In the realm of performance, pianos are indispensable instruments in classical music, jazz, and contemporary genres. Concert pianists and musicians rely on high-quality pianos to deliver exceptional performances in concert halls, theaters, and other venues. The rich and versatile sound of pianos makes them a favorite choice for solo performances, as well as for accompaniment in orchestras and bands. In the context of learning and teaching, pianos are fundamental tools in music education. They are widely used in schools, music academies, and private lessons to teach students the basics of music theory, technique, and performance. The tactile and visual nature of the piano keyboard makes it an excellent instrument for beginners to understand musical concepts. Moreover, the global Pianoforte market supports a wide range of educational materials and resources, including method books, online tutorials, and interactive apps, which enhance the learning experience. In the entertainment industry, pianos are featured prominently in movies, television shows, and live performances. They add a layer of sophistication and emotional depth to soundtracks and are often used to create memorable musical moments. Additionally, pianos are popular in casual entertainment settings such as bars, restaurants, and hotels, where they provide live music and ambiance. The versatility and timeless appeal of pianos ensure their continued relevance in various entertainment contexts. Overall, the global Pianoforte market is integral to the performance, education, and entertainment sectors, providing high-quality instruments that enrich the musical experience for professionals, students, and audiences alike.

Global Pianoforte Market Outlook:

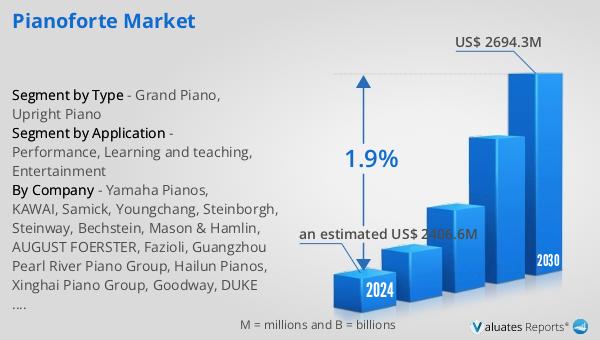

The global Pianoforte market is anticipated to grow from an estimated US$ 2406.6 million in 2024 to US$ 2694.3 million by 2030, reflecting a compound annual growth rate (CAGR) of 1.9% during the forecast period. China dominates the global Pianoforte market, accounting for approximately 72% of global consumption. The Guangzhou Pearl River Piano Group is a leading player in the market, holding a 26% share of global sales. The primary driver of the global Pianoforte market is the increasing demand for learning and teaching, which constitutes nearly 44% of the total downstream consumption. Upright pianos are the most popular type of piano, capturing 83% of the market share. This preference is largely due to their affordability and space-saving design, making them accessible to a broader range of consumers. The market's growth is supported by a combination of factors including the rising interest in music education, the popularity of live performances, and the integration of pianos in various entertainment mediums. As the market continues to evolve, manufacturers are focusing on innovation and quality to meet the diverse needs of consumers. The global Pianoforte market remains a vibrant and competitive industry, driven by a blend of tradition and modernity.

| Report Metric | Details |

| Report Name | Pianoforte Market |

| Accounted market size in 2024 | an estimated US$ 2406.6 million |

| Forecasted market size in 2030 | US$ 2694.3 million |

| CAGR | 1.9% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Yamaha Pianos, KAWAI, Samick, Youngchang, Steinborgh, Steinway, Bechstein, Mason & Hamlin, AUGUST FOERSTER, Fazioli, Guangzhou Pearl River Piano Group, Hailun Pianos, Xinghai Piano Group, Goodway, DUKE Piano, Shanghai Mendelssohn Piano, Nanjing Schumann Piano, Harmony Piano, Artfield Piano, Shanghai Piano, J-Sder Piano, Kingsburg Piano, Huapu Piano |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |