What is Global Hygienic and Aseptic Valves Market?

The Global Hygienic and Aseptic Valves Market refers to the industry focused on the production and distribution of valves designed to maintain high levels of cleanliness and sterility in various applications. These valves are essential in industries where contamination control is critical, such as food and beverage processing, pharmaceuticals, biotechnology, and dairy processing. Hygienic valves are designed to prevent the growth of bacteria and other microorganisms, ensuring that the products remain safe for consumption or use. Aseptic valves, on the other hand, are specifically designed to maintain sterility by preventing any form of contamination during the production process. The market for these valves is driven by the increasing demand for high-quality, contamination-free products, stringent regulatory standards, and the growing awareness of hygiene and safety among consumers and manufacturers. The market is characterized by continuous innovation and technological advancements to meet the evolving needs of various industries.

Hygienic Single Seat Valves, Hygienic Double Seat Valves, Hygienic Butterfly Valves, Hygienic Control Valves, Aseptic Valves in the Global Hygienic and Aseptic Valves Market:

Hygienic Single Seat Valves are designed for applications requiring strict hygiene standards. These valves are typically used in processes where the product must remain uncontaminated, such as in the food and beverage industry. They are easy to clean and maintain, ensuring that there is no residue left that could lead to contamination. Hygienic Double Seat Valves, also known as mix-proof valves, allow for the simultaneous flow of two different fluids without the risk of cross-contamination. This makes them ideal for applications where different products need to be processed in the same system without mixing. Hygienic Butterfly Valves are lightweight and compact, making them suitable for applications where space is limited. They are commonly used in the food and beverage industry for their ease of use and ability to provide a tight seal, preventing any leakage. Hygienic Control Valves are used to regulate the flow of fluids in a system, ensuring that the process remains within the desired parameters. These valves are essential in maintaining the quality and consistency of the final product. Aseptic Valves are designed to maintain sterility throughout the production process. They are used in applications where even the slightest contamination can lead to significant issues, such as in the pharmaceutical and biotechnology industries. These valves are designed to be easily sterilized and are often used in processes that require a high level of cleanliness and sterility. The Global Hygienic and Aseptic Valves Market is driven by the increasing demand for high-quality, contamination-free products, stringent regulatory standards, and the growing awareness of hygiene and safety among consumers and manufacturers. The market is characterized by continuous innovation and technological advancements to meet the evolving needs of various industries.

Dairy Processing, Food Processing, Beverage, Pharmaceuticals, Biotechnology in the Global Hygienic and Aseptic Valves Market:

The Global Hygienic and Aseptic Valves Market finds extensive usage in various industries, including dairy processing, food processing, beverages, pharmaceuticals, and biotechnology. In dairy processing, these valves are crucial for maintaining the cleanliness and sterility of milk and other dairy products. They ensure that the products remain free from contamination, which is essential for maintaining their quality and safety. In the food processing industry, hygienic and aseptic valves are used to prevent contamination during the production process. This is particularly important in the production of ready-to-eat meals, canned foods, and other processed food products. The valves help maintain the quality and safety of the products, ensuring that they are safe for consumption. In the beverage industry, these valves are used to maintain the cleanliness and sterility of various beverages, including soft drinks, juices, and alcoholic beverages. They help prevent contamination during the production process, ensuring that the beverages remain safe for consumption. In the pharmaceutical industry, hygienic and aseptic valves are used to maintain the sterility of various pharmaceutical products. This is crucial for ensuring the safety and efficacy of the products. The valves help prevent contamination during the production process, ensuring that the products remain free from harmful microorganisms. In the biotechnology industry, these valves are used to maintain the sterility of various biotechnological products. This is essential for ensuring the safety and efficacy of the products. The valves help prevent contamination during the production process, ensuring that the products remain free from harmful microorganisms. The Global Hygienic and Aseptic Valves Market is driven by the increasing demand for high-quality, contamination-free products, stringent regulatory standards, and the growing awareness of hygiene and safety among consumers and manufacturers. The market is characterized by continuous innovation and technological advancements to meet the evolving needs of various industries.

Global Hygienic and Aseptic Valves Market Outlook:

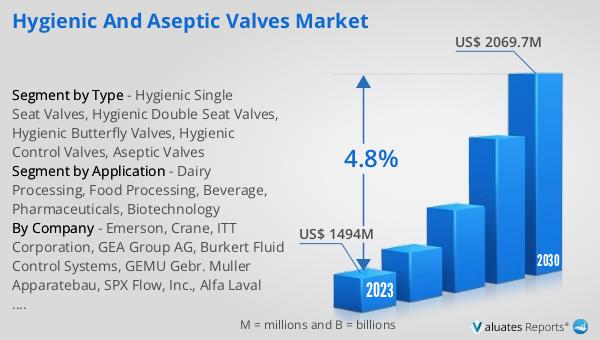

The global Hygienic and Aseptic Valves market is anticipated to grow significantly, reaching an estimated value of US$ 2069.7 million by 2030, up from US$ 1560.5 million in 2024, reflecting a compound annual growth rate (CAGR) of 4.8% between 2024 and 2030. The top five players in the Hygienic and Aseptic Valves market collectively hold around 28% of the total global market share. Europe stands as the largest market for these valves, accounting for approximately 34% of the global market, followed by the Asia-Pacific region and North America. Among the various types of valves, Aseptic Valves represent the largest segment, holding a 25% share of the market. This growth is driven by the increasing demand for high-quality, contamination-free products, stringent regulatory standards, and the growing awareness of hygiene and safety among consumers and manufacturers. The market is characterized by continuous innovation and technological advancements to meet the evolving needs of various industries.

| Report Metric | Details |

| Report Name | Hygienic and Aseptic Valves Market |

| Accounted market size in 2024 | an estimated US$ 1560.5 million |

| Forecasted market size in 2030 | US$ 2069.7 million |

| CAGR | 4.8% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Emerson, Crane, ITT Corporation, GEA Group AG, Burkert Fluid Control Systems, GEMU Gebr. Muller Apparatebau, SPX Flow, Inc., Alfa Laval AB, Evoguard GmbH (Krones), Bardiani Valvole SpA, M&S Armaturen GmbH, Gebr. Rieger GmbH & Co. KG, Armaturenwerk Hotensleben GmbH, Zhejiang Yuanan Liquid Equipment, INOXPA S.A. (Interpump Group), Keiselmann Fluid Process Group, Chinaanix, Nocado GmbH, Cipriani Harrison Valves Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |