What is Global Medical Absorbable Interference Screws Market?

The Global Medical Absorbable Interference Screws Market is a specialized segment within the broader medical devices industry, focusing on screws that are designed to be absorbed by the body over time. These screws are primarily used in orthopedic surgeries to secure grafts, such as in anterior cruciate ligament (ACL) reconstruction. Unlike traditional metal screws, absorbable interference screws eliminate the need for a second surgery to remove the hardware, thereby reducing patient recovery time and minimizing the risk of complications. The market for these screws is driven by advancements in medical technology, an aging population, and an increasing number of sports-related injuries. Additionally, the growing preference for minimally invasive surgical procedures has further fueled the demand for absorbable interference screws. These screws are made from various materials, including polymers, inorganic materials, and composites, each offering unique benefits and applications. The market is highly competitive, with numerous players striving to innovate and improve the efficacy and safety of their products. Overall, the Global Medical Absorbable Interference Screws Market is poised for significant growth, driven by technological advancements and an increasing focus on patient-centric care.

Polymer Materials, Inorganic Materials, Composite Material in the Global Medical Absorbable Interference Screws Market:

Polymer materials are a cornerstone in the Global Medical Absorbable Interference Screws Market. These materials are primarily composed of polylactic acid (PLA), polyglycolic acid (PGA), and their copolymers. PLA and PGA are favored for their biocompatibility and predictable degradation rates, which are crucial for ensuring that the screws provide adequate support during the healing process before being absorbed by the body. The degradation products of these polymers are lactic acid and glycolic acid, which are naturally metabolized by the body, minimizing the risk of adverse reactions. Inorganic materials, on the other hand, include substances like calcium phosphate and hydroxyapatite. These materials are known for their excellent osteoconductive properties, meaning they support bone growth and integration. Calcium phosphate, for instance, is a major component of bone mineral, making it highly compatible with the body's natural tissues. However, the degradation rate of inorganic materials can be slower compared to polymers, which may be a consideration in certain clinical scenarios. Composite materials combine the best of both worlds, incorporating both polymers and inorganic substances to create screws that offer a balance of strength, biocompatibility, and controlled degradation. For example, a composite screw might have a polymer matrix reinforced with calcium phosphate particles, providing both mechanical support and osteoconductivity. The use of composite materials allows for the customization of screw properties to meet specific surgical requirements. Each type of material has its own set of advantages and limitations, and the choice often depends on the specific clinical application and the surgeon's preference. The ongoing research and development in this field aim to optimize these materials further, enhancing their performance and expanding their range of applications. Overall, the diversity of materials used in the Global Medical Absorbable Interference Screws Market reflects the complexity and sophistication of modern medical technology, offering tailored solutions to meet the varied needs of patients and healthcare providers.

Hospital, Ambulatory Surgery Center, Others in the Global Medical Absorbable Interference Screws Market:

The usage of Global Medical Absorbable Interference Screws Market spans various healthcare settings, including hospitals, ambulatory surgery centers (ASCs), and other specialized medical facilities. In hospitals, these screws are predominantly used in orthopedic departments for procedures such as ACL reconstruction, rotator cuff repair, and other ligament and tendon surgeries. Hospitals often handle complex cases that require a high level of expertise and advanced medical equipment. The availability of multidisciplinary teams and comprehensive post-operative care makes hospitals a preferred setting for surgeries involving absorbable interference screws. The use of these screws in hospitals not only enhances surgical outcomes but also reduces the need for follow-up surgeries to remove hardware, thereby improving patient satisfaction and reducing healthcare costs. Ambulatory Surgery Centers (ASCs) are another significant setting for the use of absorbable interference screws. ASCs specialize in providing same-day surgical care, including diagnostic and preventive procedures. The minimally invasive nature of surgeries involving absorbable interference screws aligns well with the operational model of ASCs, which focuses on efficiency and patient convenience. The use of these screws in ASCs allows for quicker recovery times and shorter hospital stays, making it an attractive option for both patients and healthcare providers. Additionally, the cost-effectiveness of ASCs compared to traditional hospitals makes them a growing market for absorbable interference screws. Other specialized medical facilities, such as sports medicine clinics and orthopedic centers, also utilize absorbable interference screws extensively. These facilities often cater to athletes and individuals with sports-related injuries, providing targeted treatments that require the use of advanced medical devices. The use of absorbable interference screws in these settings helps in achieving optimal surgical outcomes, enabling patients to return to their active lifestyles more quickly. Overall, the versatility and effectiveness of absorbable interference screws make them a valuable asset across various healthcare settings, contributing to improved patient outcomes and streamlined surgical procedures.

Global Medical Absorbable Interference Screws Market Outlook:

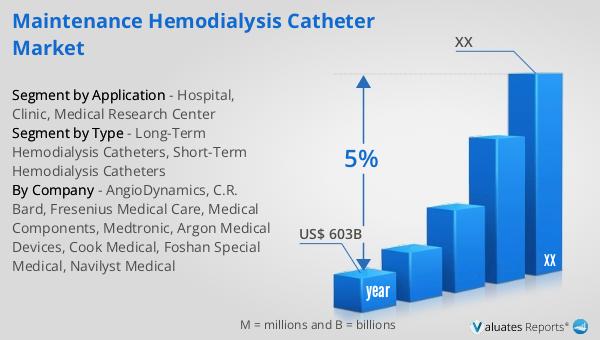

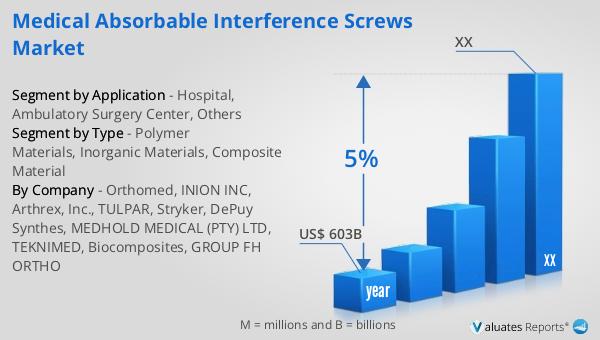

According to our research, the global market for medical devices is projected to reach approximately $603 billion by the year 2023, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth trajectory underscores the increasing demand for advanced medical technologies and devices, driven by factors such as an aging global population, rising prevalence of chronic diseases, and advancements in medical research and development. The medical devices market encompasses a wide range of products, including diagnostic equipment, surgical instruments, and therapeutic devices, all of which play a crucial role in modern healthcare. The projected growth rate indicates a robust expansion of the market, reflecting the continuous innovation and adoption of new technologies in the medical field. As healthcare systems worldwide strive to improve patient outcomes and operational efficiencies, the demand for cutting-edge medical devices is expected to rise steadily. This growth also highlights the importance of regulatory frameworks and quality standards in ensuring the safety and efficacy of medical devices. Overall, the positive market outlook for medical devices signifies a promising future for the industry, with significant opportunities for innovation and investment.

| Report Metric | Details |

| Report Name | Medical Absorbable Interference Screws Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Orthomed, INION INC, Arthrex, Inc., TULPAR, Stryker, DePuy Synthes, MEDHOLD MEDICAL (PTY) LTD, TEKNIMED, Biocomposites, GROUP FH ORTHO |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |