What is Global Through Hole Zener Diodes Market?

The global Through Hole Zener Diodes market is a specialized segment within the broader semiconductor industry. Zener diodes are a type of diode that allows current to flow in the reverse direction when a specific voltage, known as the Zener breakdown voltage, is reached. These components are crucial in various electronic circuits for voltage regulation, protection, and switching applications. The "through hole" designation refers to the method of mounting the diode on a printed circuit board (PCB), where the leads of the diode are inserted into holes and soldered to pads on the opposite side. This traditional mounting technique offers robust mechanical stability and is preferred in applications where durability and reliability are paramount. The market for these diodes is driven by their widespread use in consumer electronics, automotive systems, telecommunications, and industrial equipment. As technology advances, the demand for efficient and reliable electronic components continues to grow, fueling the expansion of the Through Hole Zener Diodes market.

Ultra Small, Small, Normal in the Global Through Hole Zener Diodes Market:

In the Global Through Hole Zener Diodes Market, products are often categorized based on their physical size and power handling capabilities, which can be broadly classified into Ultra Small, Small, and Normal sizes. Ultra Small Zener diodes are designed for applications where space is at a premium. These diodes are typically used in compact electronic devices such as smartphones, tablets, and wearable technology. Their small size allows for high-density circuit designs, which is crucial in modern consumer electronics where miniaturization is a key trend. Despite their tiny form factor, Ultra Small Zener diodes maintain high performance and reliability, making them indispensable in the design of portable and space-constrained devices. Small Zener diodes, while slightly larger than their ultra-small counterparts, still offer a compact solution for a variety of applications. These diodes are commonly found in computing devices, telecommunications equipment, and automotive electronics. They strike a balance between size and power handling, making them versatile components in many electronic circuits. Small Zener diodes are often used in voltage regulation and protection circuits, ensuring the stability and safety of electronic systems. Normal-sized Zener diodes are the largest in this classification and are typically used in industrial and high-power applications. These diodes can handle higher currents and voltages, making them suitable for use in power supplies, industrial machinery, and large-scale electronic systems. Their robust construction and higher power ratings ensure reliable performance in demanding environments. Normal-sized Zener diodes are essential in applications where durability and long-term reliability are critical. Each size category of Zener diodes serves a specific purpose and is chosen based on the requirements of the application. The diversity in size and power handling capabilities allows designers to select the most appropriate diode for their specific needs, ensuring optimal performance and efficiency in their electronic circuits. The Global Through Hole Zener Diodes Market continues to evolve, with advancements in technology driving the development of smaller, more efficient, and more reliable components. As electronic devices become more sophisticated and compact, the demand for Ultra Small and Small Zener diodes is expected to increase. However, the need for Normal-sized diodes in industrial and high-power applications remains strong, highlighting the diverse and dynamic nature of this market.

Consumer Electronics, Computing, Industrial, Telecommunications, Automotive, Others in the Global Through Hole Zener Diodes Market:

The usage of Global Through Hole Zener Diodes spans across various sectors, including Consumer Electronics, Computing, Industrial, Telecommunications, Automotive, and others. In Consumer Electronics, Zener diodes are integral for voltage regulation and protection in devices such as smartphones, tablets, and home appliances. They ensure that these devices operate within safe voltage limits, protecting sensitive components from voltage spikes and ensuring longevity. In the Computing sector, Zener diodes are used in power supplies, motherboards, and other critical components to maintain stable voltage levels and protect against electrical surges. Their reliability and efficiency are crucial in maintaining the performance and safety of computing devices, from personal computers to large data centers. In Industrial applications, Zener diodes are employed in machinery, control systems, and power supplies. They provide voltage regulation and protection in harsh environments, ensuring the reliable operation of industrial equipment. Their robust construction and ability to handle higher currents and voltages make them suitable for demanding industrial applications. In Telecommunications, Zener diodes are used in networking equipment, base stations, and communication devices. They help maintain stable voltage levels and protect sensitive components from voltage fluctuations, ensuring reliable communication and data transmission. The Automotive sector relies on Zener diodes for various applications, including voltage regulation in electronic control units (ECUs), protection of sensors and actuators, and ensuring the stability of power supplies in vehicles. Their ability to withstand harsh automotive environments and provide reliable performance is crucial for the safety and efficiency of modern vehicles. Other applications of Zener diodes include medical devices, aerospace, and defense systems, where reliable voltage regulation and protection are essential. The versatility and reliability of Zener diodes make them indispensable in a wide range of electronic applications, driving their demand across various industries.

Global Through Hole Zener Diodes Market Outlook:

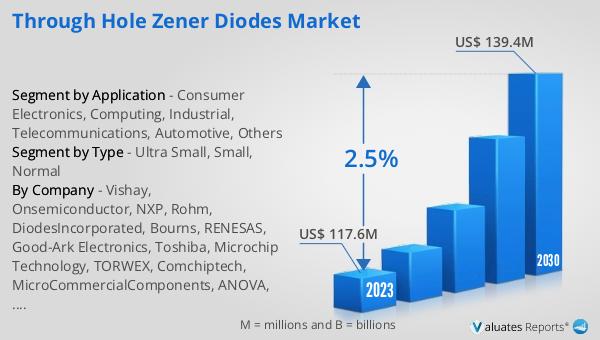

The global Through Hole Zener Diodes market was valued at US$ 117.6 million in 2023 and is anticipated to reach US$ 139.4 million by 2030, witnessing a CAGR of 2.5% during the forecast period 2024-2030. This market outlook highlights the steady growth and increasing demand for Through Hole Zener Diodes across various industries. The projected growth reflects the ongoing advancements in technology and the rising need for reliable and efficient electronic components. As industries continue to evolve and adopt more sophisticated electronic systems, the demand for Zener diodes is expected to grow. The market's growth is driven by the widespread use of these diodes in consumer electronics, automotive systems, telecommunications, and industrial equipment. The increasing complexity and miniaturization of electronic devices further fuel the demand for high-performance Zener diodes. The steady CAGR of 2.5% indicates a stable and growing market, with opportunities for innovation and development in the field of Zener diodes. The market outlook underscores the importance of Zener diodes in modern electronic systems and their critical role in ensuring the reliability and efficiency of various applications.

| Report Metric | Details |

| Report Name | Through Hole Zener Diodes Market |

| Accounted market size in 2023 | US$ 117.6 million |

| Forecasted market size in 2030 | US$ 139.4 million |

| CAGR | 2.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Vishay, Onsemiconductor, NXP, Rohm, DiodesIncorporated, Bourns, RENESAS, Good-Ark Electronics, Toshiba, Microchip Technology, TORWEX, Comchiptech, MicroCommercialComponents, ANOVA, Kexin |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |