What is Global Non-asbestos Organic Brake Pads Market?

The Global Non-asbestos Organic Brake Pads Market refers to the industry focused on the production and distribution of brake pads that do not contain asbestos. Asbestos was once a common material in brake pads due to its heat resistance and durability. However, it was found to be hazardous to health, leading to a shift towards non-asbestos organic (NAO) materials. These brake pads are made from a mixture of fibers, fillers, and binders that are safer for both the environment and human health. The market for these brake pads is growing as more countries implement stringent regulations against asbestos use. Additionally, the increasing awareness about the health risks associated with asbestos has driven both manufacturers and consumers to opt for safer alternatives. The global market encompasses various regions, including North America, Europe, Asia-Pacific, and others, each with its own set of regulations and market dynamics. The demand for non-asbestos organic brake pads is also influenced by the automotive industry's growth, technological advancements, and consumer preferences for safer and more sustainable products.

Ceramic Material, Fiber Material, Other in the Global Non-asbestos Organic Brake Pads Market:

In the Global Non-asbestos Organic Brake Pads Market, materials such as ceramic, fiber, and other composites play a crucial role. Ceramic materials are popular due to their excellent heat resistance, low noise, and minimal dust production. These brake pads are made from a combination of ceramic fibers, nonferrous filler materials, and bonding agents. They are known for providing a smooth braking experience and longer lifespan compared to traditional materials. Ceramic brake pads are particularly favored in high-performance vehicles and luxury cars where braking efficiency and comfort are paramount. On the other hand, fiber materials used in non-asbestos organic brake pads include aramid fibers, glass fibers, and other synthetic fibers. These fibers are chosen for their strength, durability, and ability to withstand high temperatures. Fiber-based brake pads offer a good balance between performance and cost, making them suitable for a wide range of vehicles, from passenger cars to commercial trucks. Other materials used in the production of non-asbestos organic brake pads include various organic compounds and resins that act as binders. These materials help in enhancing the overall performance of the brake pads by improving their structural integrity and wear resistance. The choice of material often depends on the specific requirements of the vehicle and the driving conditions. For instance, vehicles that are frequently used in urban areas with stop-and-go traffic may benefit from brake pads with higher heat resistance and durability. In contrast, vehicles used in less demanding conditions might opt for more cost-effective options. The development and innovation in materials for non-asbestos organic brake pads are driven by the need to meet regulatory standards, improve safety, and enhance the overall driving experience. Manufacturers invest in research and development to create brake pads that not only comply with environmental regulations but also offer superior performance and longevity. The competition in the market is intense, with numerous players striving to introduce advanced materials and technologies to gain a competitive edge. As a result, the Global Non-asbestos Organic Brake Pads Market continues to evolve, offering a wide range of products tailored to meet the diverse needs of the automotive industry.

OEMs Market, Aftermarket in the Global Non-asbestos Organic Brake Pads Market:

The usage of Global Non-asbestos Organic Brake Pads Market can be broadly categorized into two main areas: Original Equipment Manufacturers (OEMs) Market and Aftermarket. In the OEMs market, non-asbestos organic brake pads are supplied directly to vehicle manufacturers for installation in new vehicles. This segment is driven by the automotive industry's growth and the increasing demand for safer and more environmentally friendly components. OEMs prefer non-asbestos organic brake pads because they comply with stringent regulatory standards and offer reliable performance. The collaboration between brake pad manufacturers and vehicle manufacturers is crucial in this segment, as it ensures that the brake pads are designed and tested to meet the specific requirements of each vehicle model. The OEMs market is characterized by long-term contracts and partnerships, which provide stability and predictability for both suppliers and manufacturers. On the other hand, the aftermarket segment involves the sale of non-asbestos organic brake pads to consumers and repair shops for replacement purposes. This segment is driven by the need for regular maintenance and replacement of brake pads due to wear and tear. The aftermarket offers a wide range of options for consumers, from premium high-performance brake pads to more affordable alternatives. The availability of non-asbestos organic brake pads in the aftermarket is essential for ensuring that vehicles remain safe and compliant with environmental regulations throughout their lifespan. Consumers in the aftermarket segment are often influenced by factors such as price, brand reputation, and product performance. As a result, brake pad manufacturers invest in marketing and distribution strategies to capture a significant share of the aftermarket. The competition in the aftermarket is intense, with numerous brands vying for consumer attention. Additionally, the rise of e-commerce platforms has made it easier for consumers to access a wide range of non-asbestos organic brake pads, further driving the growth of this segment. Both the OEMs market and the aftermarket play a vital role in the overall growth of the Global Non-asbestos Organic Brake Pads Market. The continuous demand from these segments ensures that manufacturers remain focused on innovation and quality to meet the evolving needs of the automotive industry.

Global Non-asbestos Organic Brake Pads Market Outlook:

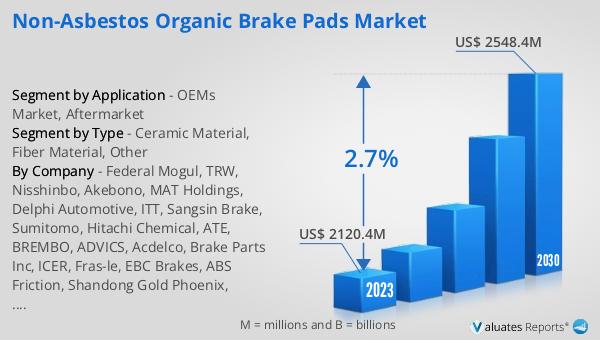

The global Non-asbestos Organic Brake Pads market was valued at US$ 2120.4 million in 2023 and is anticipated to reach US$ 2548.4 million by 2030, witnessing a CAGR of 2.7% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for non-asbestos organic brake pads over the next several years. The increasing awareness about the health risks associated with asbestos and the stringent regulations against its use are key drivers of this growth. As more countries adopt regulations to phase out asbestos-containing products, the demand for safer alternatives like non-asbestos organic brake pads is expected to rise. Additionally, the growth of the automotive industry, particularly in emerging markets, is likely to contribute to the increasing demand for these brake pads. The market's steady growth rate reflects the ongoing efforts by manufacturers to innovate and improve the performance and safety of non-asbestos organic brake pads. This includes the development of new materials and technologies that enhance the durability, heat resistance, and overall performance of the brake pads. The market outlook also highlights the importance of both the OEMs market and the aftermarket in driving the demand for non-asbestos organic brake pads. As vehicle manufacturers continue to prioritize safety and environmental compliance, the adoption of non-asbestos organic brake pads in new vehicles is expected to increase. Similarly, the aftermarket segment will continue to play a crucial role in ensuring that existing vehicles remain safe and compliant with regulations. Overall, the market outlook for non-asbestos organic brake pads is positive, with steady growth anticipated over the forecast period.

| Report Metric | Details |

| Report Name | Non-asbestos Organic Brake Pads Market |

| Accounted market size in 2023 | US$ 2120.4 million |

| Forecasted market size in 2030 | US$ 2548.4 million |

| CAGR | 2.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Federal Mogul, TRW, Nisshinbo, Akebono, MAT Holdings, Delphi Automotive, ITT, Sangsin Brake, Sumitomo, Hitachi Chemical, ATE, BREMBO, ADVICS, Acdelco, Brake Parts Inc, ICER, Fras-le, EBC Brakes, ABS Friction, Shandong Gold Phoenix, Shangdong xinyi, SAL-FER, Hunan BoYun, Double Link |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |