What is Global Reusable Latex Gloves Market?

The Global Reusable Latex Gloves Market refers to the worldwide industry focused on the production, distribution, and sale of latex gloves that can be used multiple times. These gloves are made from natural rubber latex and are designed to provide protection and durability for various applications. Unlike disposable gloves, reusable latex gloves are thicker and more robust, allowing them to withstand multiple uses and cleanings. They are commonly used in settings where hand protection is essential, such as in healthcare, industrial environments, household chores, and food service. The market for these gloves is driven by factors such as increasing awareness about hygiene and safety, the need for cost-effective protective solutions, and the growing demand from various end-use industries. The market is characterized by a wide range of products that vary in terms of size, thickness, and additional features like textured surfaces for better grip. Manufacturers in this market are continually innovating to improve the quality and functionality of reusable latex gloves, making them more comfortable and effective for users.

Natural Rubber, Neoprene, Nitrile Rubber, Other in the Global Reusable Latex Gloves Market:

Natural rubber, neoprene, nitrile rubber, and other materials play significant roles in the Global Reusable Latex Gloves Market. Natural rubber latex is the most traditional material used for making reusable gloves. It is derived from the sap of rubber trees and is known for its excellent elasticity, comfort, and tactile sensitivity. Natural rubber gloves are highly flexible and provide a snug fit, making them ideal for tasks that require precision and dexterity. However, they can cause allergic reactions in some individuals, which has led to the development of alternative materials. Neoprene, also known as polychloroprene, is a synthetic rubber that offers excellent chemical resistance and durability. Neoprene gloves are less likely to cause allergic reactions compared to natural rubber gloves and are often used in chemical industries and laboratories where exposure to hazardous substances is common. Nitrile rubber is another synthetic material that has gained popularity in the reusable gloves market. Nitrile gloves are known for their superior puncture resistance and are an excellent choice for tasks that involve handling sharp objects or abrasive materials. They also provide good chemical resistance and are less likely to cause allergic reactions, making them suitable for a wide range of applications, including medical and food service industries. Other materials used in the production of reusable latex gloves include vinyl and polyurethane. Vinyl gloves are made from polyvinyl chloride (PVC) and are a cost-effective alternative to natural rubber and nitrile gloves. They offer good resistance to oils and fats but are less durable and flexible compared to other materials. Polyurethane gloves are known for their excellent tactile sensitivity and are often used in applications that require a high degree of precision. Each of these materials has its own set of advantages and disadvantages, and the choice of material depends on the specific requirements of the task at hand. Manufacturers in the Global Reusable Latex Gloves Market continue to explore new materials and technologies to enhance the performance and safety of their products.

Household, Chemical Industry, Industrial, Foodservice, Others in the Global Reusable Latex Gloves Market:

The usage of reusable latex gloves spans across various sectors, including household, chemical industry, industrial, foodservice, and others. In households, reusable latex gloves are commonly used for cleaning, dishwashing, and gardening. They provide protection against harsh cleaning chemicals, hot water, and dirt, ensuring that the hands remain safe and clean. The gloves' durability allows them to be used multiple times, making them a cost-effective solution for everyday chores. In the chemical industry, reusable latex gloves are essential for protecting workers from hazardous substances. These gloves offer excellent chemical resistance, preventing harmful chemicals from coming into contact with the skin. They are used in laboratories, manufacturing plants, and other settings where exposure to chemicals is a common occurrence. In industrial settings, reusable latex gloves are used to protect workers from mechanical hazards, such as cuts, abrasions, and punctures. They are commonly used in construction, automotive, and manufacturing industries, where handling sharp tools and materials is a part of the job. The gloves' durability and resistance to wear and tear make them suitable for heavy-duty tasks. In the foodservice industry, reusable latex gloves are used to maintain hygiene and prevent cross-contamination. They are worn by food handlers and chefs to ensure that food is prepared in a clean and safe environment. The gloves' flexibility and tactile sensitivity allow for precise handling of food items, making them an essential tool in kitchens and food processing plants. Other sectors that use reusable latex gloves include healthcare, where they are used by medical professionals to prevent the spread of infections, and the beauty industry, where they are used by hairdressers and beauticians to protect their hands from chemicals and dyes. The versatility and durability of reusable latex gloves make them a valuable tool in various applications, ensuring safety and hygiene across different industries.

Global Reusable Latex Gloves Market Outlook:

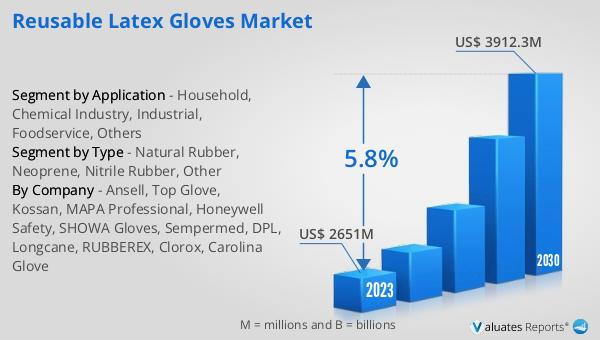

The global Reusable Latex Gloves market was valued at US$ 2651 million in 2023 and is anticipated to reach US$ 3912.3 million by 2030, witnessing a CAGR of 5.8% during the forecast period 2024-2030. This significant growth can be attributed to several factors, including the increasing awareness about hygiene and safety, the rising demand from various end-use industries, and the continuous innovation in glove manufacturing. The market's expansion is also driven by the need for cost-effective protective solutions that can be used multiple times, reducing the overall cost of hand protection. As industries such as healthcare, foodservice, and chemical continue to grow, the demand for high-quality reusable latex gloves is expected to rise. Manufacturers are focusing on developing gloves that offer better comfort, durability, and protection to meet the evolving needs of consumers. The market's growth is also supported by the increasing adoption of stringent safety regulations across various industries, which mandate the use of protective gloves to ensure worker safety. Overall, the Global Reusable Latex Gloves Market is poised for significant growth in the coming years, driven by the increasing demand for reliable and cost-effective hand protection solutions.

| Report Metric | Details |

| Report Name | Reusable Latex Gloves Market |

| Accounted market size in 2023 | US$ 2651 million |

| Forecasted market size in 2030 | US$ 3912.3 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Ansell, Top Glove, Kossan, MAPA Professional, Honeywell Safety, SHOWA Gloves, Sempermed, DPL, Longcane, RUBBEREX, Clorox, Carolina Glove |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |