What is Global Passive Safety Needles Market?

The Global Passive Safety Needles Market refers to the worldwide industry focused on the production and distribution of needles designed with built-in safety mechanisms to prevent needlestick injuries. These needles are essential in healthcare settings as they help protect healthcare workers from accidental needle sticks, which can lead to the transmission of bloodborne pathogens such as HIV, hepatitis B, and hepatitis C. The market encompasses various types of passive safety needles, including those used for injections, blood collection, and other medical procedures. The demand for these needles is driven by increasing awareness of occupational hazards, stringent regulations for healthcare worker safety, and the growing prevalence of chronic diseases that require frequent injections. As healthcare systems globally strive to enhance safety protocols, the adoption of passive safety needles is expected to rise, making this market a critical component of the broader medical devices industry.

Automatic Injection, Manual Injection in the Global Passive Safety Needles Market:

Automatic injection and manual injection are two primary methods of administering medications using passive safety needles in the Global Passive Safety Needles Market. Automatic injection systems are designed to deliver a pre-measured dose of medication with minimal user intervention. These systems often feature spring-loaded mechanisms that activate upon pressing a button, ensuring consistent and accurate delivery of the drug. Automatic injection devices are particularly beneficial for patients who require regular self-administration of medications, such as those with diabetes or multiple sclerosis. The ease of use and reduced risk of needlestick injuries make automatic injection systems a popular choice in both home and clinical settings. On the other hand, manual injection involves the traditional method of using a syringe and needle to administer medication. In the context of passive safety needles, manual injection devices are equipped with safety features such as retractable needles or needle shields that activate after the injection is completed. These safety mechanisms are designed to protect healthcare workers from accidental needle sticks during and after the injection process. Manual injection devices are widely used in hospitals, clinics, and other healthcare facilities due to their versatility and cost-effectiveness. Both automatic and manual injection systems play a crucial role in the Global Passive Safety Needles Market, catering to different needs and preferences of healthcare providers and patients. The choice between automatic and manual injection often depends on factors such as the type of medication, the frequency of administration, and the setting in which the injection is given. For instance, automatic injection systems are ideal for patients who need to self-administer medication at home, while manual injection devices are more commonly used in clinical settings where healthcare professionals can oversee the process. Despite the differences in their operation, both types of injection systems share the common goal of enhancing safety and reducing the risk of needlestick injuries. As the Global Passive Safety Needles Market continues to evolve, advancements in technology are likely to further improve the functionality and safety of both automatic and manual injection devices, ultimately benefiting patients and healthcare workers alike.

Hospitals, Clinics, Others in the Global Passive Safety Needles Market:

The usage of passive safety needles in hospitals is extensive and multifaceted. Hospitals are high-risk environments for needlestick injuries due to the high volume of injections and blood draws performed daily. Passive safety needles are employed in various departments, including emergency rooms, operating theaters, and intensive care units, to enhance the safety of both patients and healthcare workers. These needles are particularly crucial in high-stress situations where the risk of accidental needle sticks is elevated. By incorporating passive safety needles into their protocols, hospitals can significantly reduce the incidence of needlestick injuries, thereby improving overall workplace safety and compliance with health regulations. Clinics, which often serve as the first point of contact for patients seeking medical care, also benefit greatly from the use of passive safety needles. In these settings, healthcare providers frequently administer vaccinations, draw blood, and perform minor surgical procedures. The use of passive safety needles in clinics helps minimize the risk of needlestick injuries, ensuring a safer environment for both staff and patients. Additionally, the adoption of these needles can enhance the clinic's reputation for safety and quality care, attracting more patients and fostering trust within the community. Beyond hospitals and clinics, passive safety needles find applications in various other settings, including long-term care facilities, home healthcare, and public health initiatives. In long-term care facilities, where residents often require regular injections and blood tests, the use of passive safety needles can protect both residents and caregivers from potential injuries. Home healthcare providers, who administer treatments in patients' homes, also rely on these needles to ensure safe and effective care. Public health initiatives, such as vaccination campaigns and blood donation drives, benefit from the use of passive safety needles by reducing the risk of needlestick injuries among volunteers and healthcare workers. Overall, the widespread adoption of passive safety needles across different healthcare settings underscores their importance in promoting safety and preventing injuries. As awareness of the risks associated with needlestick injuries continues to grow, the demand for passive safety needles is likely to increase, driving further innovation and improvements in this critical area of healthcare.

Global Passive Safety Needles Market Outlook:

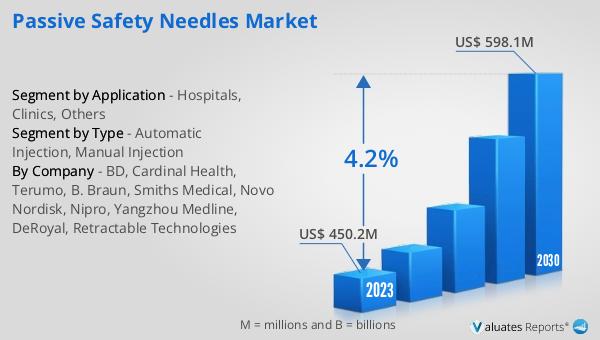

The global Passive Safety Needles market was valued at US$ 450.2 million in 2023 and is anticipated to reach US$ 598.1 million by 2030, witnessing a CAGR of 4.2% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of the passive safety needles market over the next several years. The increasing awareness of the importance of needlestick injury prevention, coupled with stringent regulatory requirements, is expected to drive the demand for passive safety needles. As healthcare providers and institutions prioritize the safety of their staff and patients, the adoption of these needles is likely to rise. The projected growth in market value reflects the ongoing efforts to enhance safety protocols in healthcare settings and the continuous advancements in needle technology. With a steady CAGR of 4.2%, the passive safety needles market is poised for substantial expansion, underscoring its critical role in the global healthcare landscape.

| Report Metric | Details |

| Report Name | Passive Safety Needles Market |

| Accounted market size in 2023 | US$ 450.2 million |

| Forecasted market size in 2030 | US$ 598.1 million |

| CAGR | 4.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | BD, Cardinal Health, Terumo, B. Braun, Smiths Medical, Novo Nordisk, Nipro, Yangzhou Medline, DeRoyal, Retractable Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |