What is Global Patient Engagement Software and Solutions Market?

Global Patient Engagement Software and Solutions Market refers to a comprehensive range of digital tools and platforms designed to enhance patient involvement in their own healthcare. These solutions aim to improve communication between patients and healthcare providers, streamline administrative processes, and ultimately lead to better health outcomes. The market encompasses various types of software, including mobile apps, web-based platforms, and cloud-based solutions, which facilitate activities such as appointment scheduling, medication management, and access to medical records. By empowering patients with information and tools to manage their health, these solutions contribute to more efficient and effective healthcare delivery. The growing emphasis on patient-centered care and the increasing adoption of digital health technologies are key drivers of this market.

Web-Based, Cloud-Based, On-Premise in the Global Patient Engagement Software and Solutions Market:

Web-Based, Cloud-Based, and On-Premise solutions are the three primary deployment models in the Global Patient Engagement Software and Solutions Market. Web-Based solutions are accessible through internet browsers and do not require any software installation on the user's device. These solutions offer the advantage of being easily accessible from any location with an internet connection, making them highly convenient for both patients and healthcare providers. They typically feature user-friendly interfaces and can be integrated with other healthcare systems to provide a seamless experience. Cloud-Based solutions, on the other hand, are hosted on remote servers and accessed via the internet. These solutions offer scalability, flexibility, and cost-effectiveness, as they eliminate the need for healthcare organizations to invest in and maintain their own IT infrastructure. Cloud-Based solutions also facilitate real-time data sharing and collaboration among healthcare providers, which can lead to improved patient care. On-Premise solutions are installed and run on the healthcare organization's own servers and infrastructure. While these solutions offer greater control over data security and customization, they require significant upfront investment and ongoing maintenance. On-Premise solutions may be preferred by larger healthcare organizations with the resources to manage their own IT systems. Each of these deployment models has its own set of advantages and challenges, and the choice of model depends on factors such as the size of the healthcare organization, budget, and specific needs of the patients and providers.

Health Management, Social and Behavioral Management, Home Health Management in the Global Patient Engagement Software and Solutions Market:

The usage of Global Patient Engagement Software and Solutions Market spans across various areas, including Health Management, Social and Behavioral Management, and Home Health Management. In Health Management, these solutions enable patients to actively participate in their own care by providing tools for tracking vital signs, managing medications, and accessing health records. This empowers patients to make informed decisions about their health and fosters better communication with healthcare providers. In Social and Behavioral Management, patient engagement solutions offer features such as mental health support, lifestyle coaching, and social networking platforms that connect patients with similar health conditions. These tools help patients manage stress, adopt healthier behaviors, and build supportive communities, which can lead to improved mental and emotional well-being. In Home Health Management, patient engagement solutions facilitate remote monitoring of chronic conditions, enabling patients to receive care in the comfort of their own homes. These solutions often include telehealth capabilities, allowing patients to consult with healthcare providers via video calls, and remote monitoring devices that transmit health data to providers in real-time. This not only enhances patient convenience but also reduces the need for frequent hospital visits, leading to cost savings for both patients and healthcare systems. Overall, the usage of patient engagement solutions in these areas contributes to more personalized, efficient, and effective healthcare delivery.

Global Patient Engagement Software and Solutions Market Outlook:

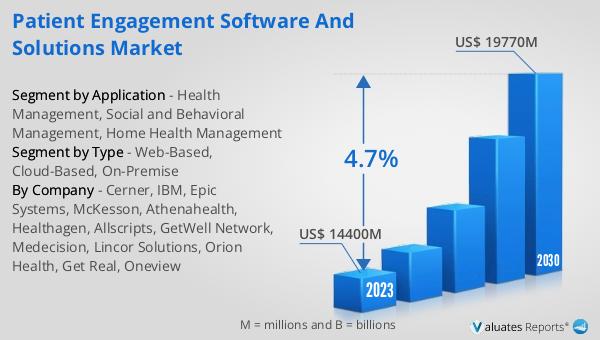

The global Patient Engagement Software and Solutions market was valued at US$ 14,400 million in 2023 and is projected to reach US$ 19,770 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.7% during the forecast period from 2024 to 2030. This market outlook indicates a steady growth trajectory driven by the increasing adoption of digital health technologies and the growing emphasis on patient-centered care. The rising demand for efficient healthcare delivery systems and the need to improve patient outcomes are key factors contributing to this market expansion. As healthcare providers continue to recognize the benefits of patient engagement solutions in enhancing communication, streamlining administrative processes, and empowering patients, the market is expected to witness sustained growth. The projected increase in market value underscores the importance of these solutions in the evolving healthcare landscape.

| Report Metric | Details |

| Report Name | Patient Engagement Software and Solutions Market |

| Accounted market size in 2023 | US$ 14400 million |

| Forecasted market size in 2030 | US$ 19770 million |

| CAGR | 4.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Cerner, IBM, Epic Systems, McKesson, Athenahealth, Healthagen, Allscripts, GetWell Network, Medecision, Lincor Solutions, Orion Health, Get Real, Oneview |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |