What is Global Handheld Hemoglobin Monitor Market?

The Global Handheld Hemoglobin Monitor Market refers to the worldwide industry focused on the production, distribution, and utilization of portable devices designed to measure hemoglobin levels in the blood. Hemoglobin is a crucial protein in red blood cells that carries oxygen from the lungs to the rest of the body. These handheld monitors are essential tools in medical settings, providing quick and accurate hemoglobin readings, which are vital for diagnosing and managing conditions like anemia, polycythemia, and other blood disorders. The market encompasses a variety of devices that cater to different needs, including those used in hospitals, specialty clinics, and ambulatory surgical centers. The demand for these monitors is driven by the increasing prevalence of blood-related health issues, advancements in medical technology, and the need for efficient and portable diagnostic tools. As healthcare systems worldwide continue to evolve, the Global Handheld Hemoglobin Monitor Market is expected to grow, offering innovative solutions to improve patient care and outcomes.

Intrusive, Non-invasive in the Global Handheld Hemoglobin Monitor Market:

In the Global Handheld Hemoglobin Monitor Market, devices are categorized based on their method of measuring hemoglobin levels: intrusive and non-invasive. Intrusive hemoglobin monitors require a blood sample, typically obtained through a finger prick or venipuncture. These devices are known for their accuracy and reliability, making them a standard choice in many medical settings. The process involves drawing a small amount of blood, which is then analyzed by the device to determine the hemoglobin concentration. Despite their accuracy, intrusive methods can cause discomfort to patients and carry a risk of infection if not performed under sterile conditions. On the other hand, non-invasive hemoglobin monitors offer a more patient-friendly alternative. These devices use advanced technologies such as optical sensors and spectroscopy to measure hemoglobin levels without the need for a blood sample. Non-invasive monitors work by emitting light through the skin and analyzing the light absorption patterns to estimate hemoglobin concentration. This method is painless, reduces the risk of infection, and allows for continuous monitoring, making it particularly useful in critical care settings and for patients who require frequent hemoglobin checks. However, non-invasive devices may sometimes be less accurate than their intrusive counterparts, especially in cases of severe anemia or other conditions that affect blood composition. The choice between intrusive and non-invasive monitors depends on various factors, including the clinical setting, patient condition, and the need for accuracy versus convenience. Both types of devices play a crucial role in the Global Handheld Hemoglobin Monitor Market, catering to different needs and preferences in the healthcare industry. As technology continues to advance, the gap between the accuracy of intrusive and non-invasive monitors is expected to narrow, further enhancing the utility and adoption of non-invasive devices.

Hospital, Specialty Clinic, Ambulatory Surgical Center in the Global Handheld Hemoglobin Monitor Market:

The usage of handheld hemoglobin monitors in hospitals is extensive and multifaceted. In hospital settings, these devices are crucial for the rapid assessment of patients' hemoglobin levels, which is essential for diagnosing and managing various medical conditions. For instance, in emergency departments, handheld hemoglobin monitors enable quick screening for anemia or blood loss in trauma patients, facilitating timely interventions. In surgical wards, these devices help monitor patients' hemoglobin levels before, during, and after surgery to ensure they remain within safe limits, thereby reducing the risk of complications. Additionally, in intensive care units (ICUs), continuous monitoring of hemoglobin levels using non-invasive devices can be vital for critically ill patients who require constant observation. Specialty clinics also benefit significantly from handheld hemoglobin monitors. These clinics, which focus on specific medical fields such as hematology, oncology, or nephrology, often deal with patients who have chronic conditions that affect blood health. Handheld hemoglobin monitors provide a convenient and efficient way to regularly check hemoglobin levels, enabling healthcare providers to adjust treatments promptly and improve patient outcomes. For example, in hematology clinics, these devices are used to monitor patients with anemia or polycythemia, ensuring that their hemoglobin levels are managed effectively. In oncology clinics, they help track the impact of chemotherapy on patients' blood health, allowing for timely interventions to address any adverse effects. Ambulatory surgical centers (ASCs) also rely on handheld hemoglobin monitors to enhance patient care. ASCs perform a wide range of surgical procedures that do not require overnight hospital stays. In these settings, handheld hemoglobin monitors are used to assess patients' hemoglobin levels before surgery to ensure they are fit for the procedure. Post-operatively, these devices help monitor patients' recovery, ensuring that any significant changes in hemoglobin levels are promptly addressed. The portability and ease of use of handheld hemoglobin monitors make them particularly valuable in ASCs, where quick and accurate assessments are essential for efficient patient turnover and high-quality care. Overall, the usage of handheld hemoglobin monitors in hospitals, specialty clinics, and ambulatory surgical centers underscores their importance in modern healthcare. These devices enhance diagnostic accuracy, improve patient monitoring, and facilitate timely interventions, ultimately contributing to better patient outcomes and more efficient healthcare delivery.

Global Handheld Hemoglobin Monitor Market Outlook:

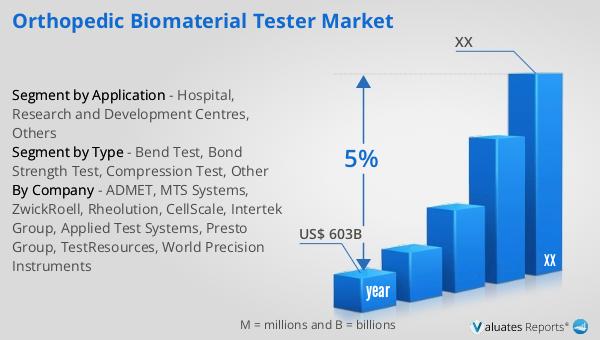

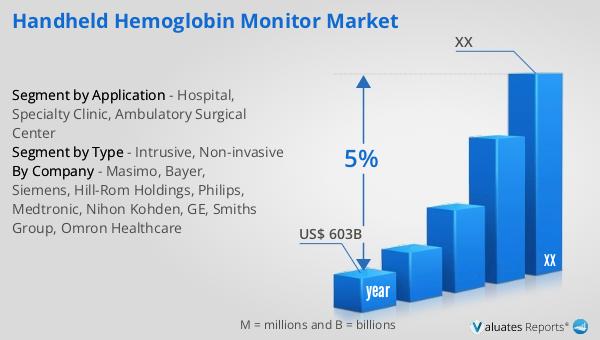

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This robust growth trajectory underscores the increasing demand for innovative medical technologies and devices, including handheld hemoglobin monitors. The expanding market reflects the rising prevalence of chronic diseases, an aging global population, and the continuous advancements in medical technology that drive the need for more efficient and effective diagnostic tools. Handheld hemoglobin monitors, as part of this broader market, are expected to benefit from these trends, offering healthcare providers portable and reliable solutions for monitoring hemoglobin levels. The growth in the medical device market also highlights the importance of ongoing research and development efforts to introduce new and improved devices that meet the evolving needs of healthcare systems worldwide. As the market continues to expand, it will likely see increased competition and innovation, leading to better products and services that enhance patient care and outcomes.

| Report Metric | Details |

| Report Name | Handheld Hemoglobin Monitor Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Masimo, Bayer, Siemens, Hill-Rom Holdings, Philips, Medtronic, Nihon Kohden, GE, Smiths Group, Omron Healthcare |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |