What is Global High Temperature Sealing Glass Market?

The Global High Temperature Sealing Glass Market refers to a specialized segment within the materials industry that focuses on the production and application of glass materials capable of withstanding extremely high temperatures. These glasses are designed to maintain their structural integrity and sealing properties even when exposed to temperatures that can exceed 1000°C. This makes them essential in various high-temperature applications where traditional materials would fail. The market encompasses a range of products, including glass powders, pastes, and preforms, which are used in industries such as electronics, automotive, aerospace, and energy. The demand for high temperature sealing glass is driven by the need for reliable and durable sealing solutions in environments where thermal stability is critical. This market is characterized by continuous innovation and development to meet the evolving requirements of advanced technologies and industrial processes.

800℃, 850℃, 950℃, 1000℃, Other in the Global High Temperature Sealing Glass Market:

In the Global High Temperature Sealing Glass Market, products are often categorized based on the temperature ranges they can withstand, such as 800°C, 850°C, 950°C, 1000°C, and other specific temperature thresholds. Each category serves different industrial needs and applications. For instance, sealing glasses that can withstand up to 800°C are typically used in applications where moderate high temperatures are encountered, such as certain types of sensors and low-temperature fuel cells. These glasses provide a balance between thermal resistance and cost-effectiveness. Moving up the scale, 850°C sealing glasses are often employed in more demanding environments, such as in some automotive components and higher temperature sensors. These glasses offer enhanced thermal stability and are designed to maintain their sealing properties under more strenuous conditions. At 950°C, the sealing glasses are used in even more critical applications, such as in aerospace components and advanced electronics, where the materials must endure extreme thermal cycles without degradation. These glasses are engineered to provide superior performance in terms of thermal expansion compatibility and mechanical strength. The 1000°C category represents the pinnacle of high temperature sealing glass technology, used in the most demanding applications, including certain types of high-performance batteries, industrial furnaces, and specialized aerospace components. These glasses are formulated to withstand the highest temperatures while maintaining their sealing integrity and mechanical properties. Beyond these specific categories, there are also other specialized high temperature sealing glasses designed for niche applications that may require unique properties such as chemical resistance, specific thermal expansion coefficients, or particular mechanical strengths. These specialized glasses are often developed in collaboration with end-users to meet the precise requirements of their applications. The continuous development and refinement of high temperature sealing glass products are driven by the need to address the challenges posed by increasingly advanced and demanding industrial processes.

Battery, Electronics and Semiconductors, Home Appliances, Others in the Global High Temperature Sealing Glass Market:

The Global High Temperature Sealing Glass Market finds extensive usage across various sectors, including batteries, electronics and semiconductors, home appliances, and other specialized applications. In the battery industry, high temperature sealing glass is crucial for the production of solid oxide fuel cells and other high-performance batteries that operate at elevated temperatures. These glasses provide a reliable seal that prevents the leakage of gases and ensures the longevity and efficiency of the battery. In the electronics and semiconductor industry, high temperature sealing glass is used in the manufacturing of components that must withstand high thermal loads, such as sensors, capacitors, and certain types of integrated circuits. These glasses ensure the stability and reliability of electronic components by providing a robust seal that can endure the thermal stresses encountered during operation. In the realm of home appliances, high temperature sealing glass is used in products such as ovens, stoves, and other heating devices where components are exposed to high temperatures. These glasses help to maintain the efficiency and safety of the appliances by providing durable seals that can withstand repeated thermal cycling. Beyond these primary applications, high temperature sealing glass is also used in a variety of other specialized areas. For example, in the aerospace industry, these glasses are used in the production of components that must endure extreme thermal conditions, such as turbine engines and heat shields. In the automotive industry, high temperature sealing glass is used in the production of sensors and other components that are exposed to high temperatures. Additionally, high temperature sealing glass is used in the energy sector, particularly in the production of solar panels and other renewable energy technologies that require materials capable of withstanding high thermal loads. The versatility and reliability of high temperature sealing glass make it an essential material in a wide range of industrial applications, driving its demand and continuous development.

Global High Temperature Sealing Glass Market Outlook:

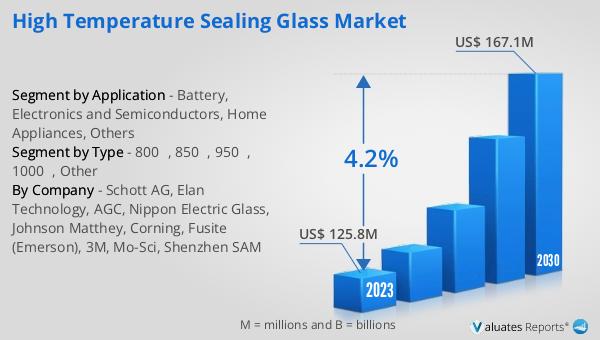

The global High Temperature Sealing Glass market was valued at US$ 125.8 million in 2023 and is anticipated to reach US$ 167.1 million by 2030, witnessing a CAGR of 4.2% during the forecast period 2024-2030. This market outlook highlights the steady growth and increasing demand for high temperature sealing glass products across various industries. The projected growth is driven by the need for materials that can withstand extreme temperatures and provide reliable sealing solutions in critical applications. As industries continue to advance and develop more sophisticated technologies, the demand for high temperature sealing glass is expected to rise, supporting the market's growth trajectory. The market's expansion is also fueled by ongoing research and development efforts aimed at enhancing the performance and capabilities of high temperature sealing glass products. These efforts are focused on addressing the specific requirements of different applications, ensuring that the materials can meet the stringent demands of modern industrial processes. The steady growth rate of 4.2% reflects the increasing recognition of the importance of high temperature sealing glass in maintaining the efficiency, safety, and reliability of various high-temperature applications.

| Report Metric | Details |

| Report Name | High Temperature Sealing Glass Market |

| Accounted market size in 2023 | US$ 125.8 million |

| Forecasted market size in 2030 | US$ 167.1 million |

| CAGR | 4.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Schott AG, Elan Technology, AGC, Nippon Electric Glass, Johnson Matthey, Corning, Fusite (Emerson), 3M, Mo-Sci, Shenzhen SAM |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |