What is Global Point Of Care Blood Testing Devices Market?

The Global Point Of Care (POC) Blood Testing Devices Market refers to the industry focused on the development, production, and distribution of medical devices that allow for immediate blood testing at the patient's location, rather than in a centralized laboratory. These devices are designed to provide rapid results, which can be crucial for timely diagnosis and treatment. The market encompasses a variety of devices, including those used for glucose monitoring, coagulation testing, blood gas and electrolyte analysis, and hematology. The convenience and speed of POC blood testing devices make them invaluable in various healthcare settings, from hospitals and clinics to homecare environments. The growing demand for quick and accurate diagnostic tools, coupled with advancements in technology, is driving the expansion of this market globally.

Diabete POC Analyzer, Coaglulation POC Analyzer, POC Blood Analyzer, Hematology POC Reader in the Global Point Of Care Blood Testing Devices Market:

Diabetes POC Analyzers are specialized devices used to monitor blood glucose levels in patients with diabetes. These analyzers provide immediate results, allowing for timely adjustments in medication and lifestyle to manage blood sugar levels effectively. They are essential for both Type 1 and Type 2 diabetes management, offering convenience and accuracy. Coagulation POC Analyzers, on the other hand, are used to assess blood clotting functions. These devices are crucial for patients on anticoagulant therapy, such as those with atrial fibrillation or deep vein thrombosis, as they help monitor and adjust medication dosages to prevent complications like stroke or excessive bleeding. POC Blood Analyzers are versatile devices that can measure various blood parameters, including glucose, hemoglobin, and electrolytes. These analyzers are widely used in emergency settings, intensive care units, and during surgeries to provide real-time data that can influence immediate medical decisions. Hematology POC Readers are designed to analyze blood samples for complete blood counts (CBC), which include red and white blood cell counts, hemoglobin levels, and platelet counts. These readers are essential for diagnosing and monitoring conditions like anemia, infections, and blood disorders. The integration of these devices into the Global Point Of Care Blood Testing Devices Market highlights the importance of rapid diagnostics in improving patient outcomes and streamlining healthcare processes. The ability to obtain quick and accurate results at the point of care reduces the need for multiple visits and extensive laboratory work, ultimately enhancing the efficiency of healthcare delivery.

Hospitals, Clinics, Health Centers, Homecare Settings in the Global Point Of Care Blood Testing Devices Market:

The usage of Global Point Of Care Blood Testing Devices Market in hospitals is pivotal for providing immediate diagnostic results, which can significantly impact patient care. In emergency departments, these devices enable rapid assessment of critical conditions, such as heart attacks or severe infections, allowing for swift intervention. In intensive care units, POC blood testing devices are used to monitor patients' vital parameters continuously, ensuring timely adjustments in treatment plans. Clinics also benefit from these devices, as they allow for quick diagnostics during routine check-ups or follow-up visits. This immediacy helps in making informed decisions on the spot, reducing the need for patients to return for additional tests. Health centers, especially those in remote or underserved areas, rely on POC blood testing devices to provide essential diagnostic services that might otherwise be unavailable. These devices help bridge the gap in healthcare access, ensuring that patients receive timely and accurate diagnoses. In homecare settings, POC blood testing devices empower patients to manage chronic conditions like diabetes or coagulation disorders independently. The convenience of self-monitoring not only improves patient compliance but also reduces the burden on healthcare facilities. Overall, the integration of POC blood testing devices across various healthcare settings enhances the quality of care, improves patient outcomes, and optimizes resource utilization.

Global Point Of Care Blood Testing Devices Market Outlook:

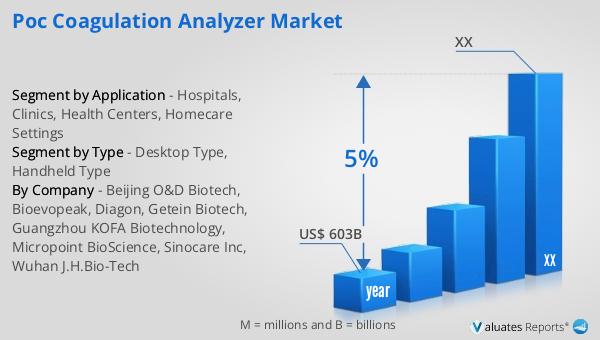

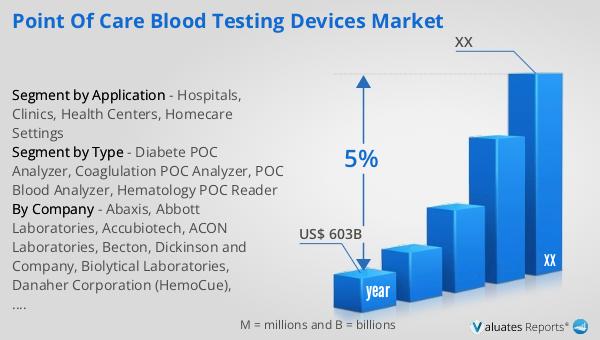

Based on our research, the global market for medical devices is projected to reach approximately US$ 603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by advancements in medical technology, increasing prevalence of chronic diseases, and a rising demand for efficient and accurate diagnostic tools. The expansion of the Global Point Of Care Blood Testing Devices Market is a significant contributor to this overall market growth. The ability to provide rapid and reliable diagnostic results at the point of care is transforming healthcare delivery, making it more responsive and patient-centered. As healthcare systems worldwide continue to evolve, the demand for innovative medical devices, including POC blood testing devices, is expected to rise, further propelling market growth.

| Report Metric | Details |

| Report Name | Point Of Care Blood Testing Devices Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Abaxis, Abbott Laboratories, Accubiotech, ACON Laboratories, Becton, Dickinson and Company, Biolytical Laboratories, Danaher Corporation (HemoCue), Siemens Healthineers, Meridian Bioscience |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |