What is Global Anti-Drone Weapon System Market?

The Global Anti-Drone Weapon System Market refers to the industry focused on developing and deploying technologies designed to detect, track, and neutralize unmanned aerial vehicles (UAVs), commonly known as drones. These systems are crucial in addressing the growing threat posed by unauthorized or hostile drones, which can be used for surveillance, smuggling, or even armed attacks. The market encompasses a wide range of solutions, including radar systems, radio frequency detectors, jamming devices, and kinetic weapons, all aimed at ensuring airspace security. As drones become more accessible and their usage proliferates across various sectors, the demand for effective anti-drone measures has surged. This market is driven by the need to protect critical infrastructure, military installations, and public events from potential drone-related threats. Governments, defense organizations, and private enterprises are investing heavily in anti-drone technologies to safeguard their assets and maintain operational security. The market is characterized by rapid technological advancements and a growing number of players offering innovative solutions to counter the evolving drone threat landscape.

Anti-UAV Missile System, Laser Weapon System, Microwave Weapon System, Combat Drone System in the Global Anti-Drone Weapon System Market:

The Anti-UAV Missile System is a specialized technology within the Global Anti-Drone Weapon System Market designed to intercept and destroy hostile drones using guided missiles. These systems are typically deployed in military settings where the threat level is high, and precision is paramount. They use advanced targeting systems to lock onto drones and neutralize them from a distance, ensuring minimal collateral damage. The Laser Weapon System, on the other hand, employs directed energy to disable or destroy drones. This technology is highly effective due to its speed and accuracy, capable of engaging multiple targets in quick succession. Laser systems are particularly useful in scenarios where stealth and precision are required, such as protecting sensitive installations or during covert operations. The Microwave Weapon System uses high-powered microwaves to disrupt the electronic systems of drones, rendering them inoperative. This non-kinetic approach is advantageous in urban environments where traditional kinetic methods might pose risks to civilians and infrastructure. Microwave systems can cover a wide area, making them suitable for protecting large perimeters or critical infrastructure. Lastly, the Combat Drone System represents a more aggressive approach within the anti-drone arsenal. These are drones designed to hunt and neutralize other drones, often equipped with various weapons or jamming devices. Combat drones offer flexibility and can be deployed quickly to respond to emerging threats. They are particularly useful in dynamic combat environments where threats are constantly evolving. Each of these systems plays a crucial role in the broader strategy to counter the growing drone threat, offering unique capabilities that can be tailored to specific operational needs.

Military Defense, Commercial in the Global Anti-Drone Weapon System Market:

The usage of Global Anti-Drone Weapon Systems in Military Defense is paramount for maintaining national security and protecting military assets. These systems are deployed to safeguard military bases, forward operating bases, and other critical infrastructure from potential drone attacks. In combat zones, anti-drone systems provide a crucial layer of defense against enemy reconnaissance and weaponized drones. They help in maintaining air superiority by neutralizing aerial threats before they can cause harm. Additionally, these systems are used in border security operations to prevent smuggling and unauthorized surveillance by hostile entities. In the commercial sector, anti-drone systems are increasingly being adopted to protect sensitive areas such as airports, power plants, and public events. Airports, in particular, face significant risks from drones that can disrupt flight operations and pose safety hazards. Anti-drone technologies help in detecting and mitigating these threats, ensuring the safety of passengers and aircraft. Similarly, power plants and other critical infrastructure use these systems to prevent potential sabotage or espionage. Public events, such as concerts and sports events, also benefit from anti-drone measures to ensure the safety of attendees and prevent disruptions. The commercial adoption of anti-drone systems is driven by the need to protect valuable assets and maintain operational continuity in the face of evolving drone threats. Both military and commercial sectors rely on these advanced technologies to address the unique challenges posed by the proliferation of drones, ensuring security and safety in various operational environments.

Global Anti-Drone Weapon System Market Outlook:

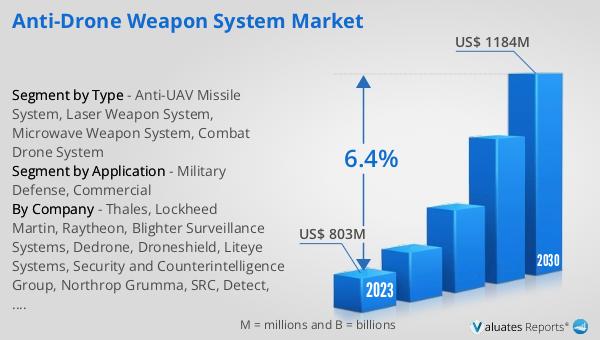

The global Anti-Drone Weapon System market was valued at US$ 803 million in 2023 and is anticipated to reach US$ 1184 million by 2030, witnessing a CAGR of 6.4% during the forecast period 2024-2030. This market growth reflects the increasing demand for advanced technologies to counter the rising threat of unauthorized and hostile drones. As drones become more prevalent and accessible, the need for effective anti-drone measures has become critical for both military and commercial applications. Governments and private enterprises are investing heavily in research and development to enhance the capabilities of anti-drone systems, ensuring they can effectively detect, track, and neutralize a wide range of drone threats. The market is characterized by rapid technological advancements and a growing number of players offering innovative solutions to address the evolving drone threat landscape. This growth trajectory underscores the importance of anti-drone technologies in maintaining security and operational integrity across various sectors.

| Report Metric | Details |

| Report Name | Anti-Drone Weapon System Market |

| Accounted market size in 2023 | US$ 803 million |

| Forecasted market size in 2030 | US$ 1184 million |

| CAGR | 6.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Thales, Lockheed Martin, Raytheon, Blighter Surveillance Systems, Dedrone, Droneshield, Liteye Systems, Security and Counterintelligence Group, Northrop Grumma, SRC, Detect, Theiss Uav Solutions, Battele Memorial Institute |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |