What is Global Air-Supported Radome Market?

The global Air-Supported Radome market is a specialized segment within the broader radome industry, focusing on structures that protect radar and communication equipment from environmental elements while allowing electromagnetic signals to pass through. These radomes are essentially air-inflated structures, which makes them lightweight, portable, and easy to deploy. They are used in various applications, including military, aerospace, and telecommunications, where they provide a protective barrier against harsh weather conditions, debris, and other potential hazards. The market for air-supported radomes is driven by the increasing need for advanced communication systems and the growing demand for reliable and durable protective solutions in extreme environments. The versatility and efficiency of air-supported radomes make them an attractive option for organizations looking to safeguard their critical equipment without compromising on performance. As technology continues to advance, the global Air-Supported Radome market is expected to see further innovations and improvements, enhancing their functionality and expanding their range of applications.

Hemispherical, Tent Shape, Others in the Global Air-Supported Radome Market:

Air-supported radomes come in various shapes and designs, each tailored to meet specific requirements and environmental conditions. The hemispherical radome is one of the most common types, characterized by its dome-like shape that provides excellent aerodynamic properties and structural integrity. This design is particularly effective in minimizing wind resistance and distributing stress evenly across the surface, making it ideal for use in high-wind areas and extreme weather conditions. Hemispherical radomes are often used in military and aerospace applications, where they protect radar and communication systems from harsh environmental factors while maintaining optimal performance. Another popular design is the tent-shaped radome, which features a more angular and elongated structure. This shape is advantageous for applications that require a larger internal volume and greater flexibility in terms of equipment placement. Tent-shaped radomes are commonly used in telecommunications and satellite communication systems, where they provide ample space for antennas and other equipment while ensuring reliable signal transmission. Additionally, the tent shape allows for easy installation and dismantling, making it a practical choice for temporary or mobile setups. Other designs in the air-supported radome market include cylindrical and conical shapes, each offering unique benefits depending on the specific application and environmental conditions. Cylindrical radomes, for example, are often used in maritime and coastal installations, where their streamlined shape helps reduce drag and withstand strong winds and waves. Conical radomes, on the other hand, are typically used in aviation and aerospace applications, where their tapered design enhances aerodynamic performance and reduces the impact of wind loads. The choice of radome shape and design depends on various factors, including the type of equipment being protected, the environmental conditions, and the specific requirements of the application. Each design offers distinct advantages and can be customized to meet the unique needs of different industries and use cases. As the demand for advanced communication and radar systems continues to grow, the market for air-supported radomes is expected to see further diversification and innovation in terms of shapes and designs, providing more options for organizations looking to protect their critical equipment.

Extreme Environment, General Environment in the Global Air-Supported Radome Market:

The usage of air-supported radomes in extreme environments is crucial for ensuring the reliability and longevity of radar and communication systems. In harsh conditions such as arctic regions, deserts, and high-altitude locations, these radomes provide a robust protective barrier against extreme temperatures, strong winds, and other environmental challenges. For instance, in arctic regions, air-supported radomes are designed to withstand freezing temperatures and heavy snow loads, ensuring that radar and communication equipment remain operational even in the most severe weather conditions. Similarly, in desert environments, these radomes protect against high temperatures, sandstorms, and UV radiation, preventing damage to sensitive equipment and maintaining optimal performance. The ability to deploy air-supported radomes quickly and efficiently makes them an ideal solution for temporary or emergency installations in extreme environments. In general environments, air-supported radomes offer a versatile and cost-effective solution for protecting radar and communication systems from everyday weather conditions and environmental hazards. These radomes are commonly used in urban and suburban areas, where they provide a protective barrier against rain, wind, and debris, ensuring the uninterrupted operation of critical equipment. In addition to their protective capabilities, air-supported radomes also offer advantages in terms of ease of installation and maintenance. Their lightweight and portable design allows for quick deployment and relocation, making them a practical choice for various applications, including telecommunications, satellite communication, and military installations. Furthermore, the use of air-supported radomes in general environments helps extend the lifespan of radar and communication systems by reducing the impact of environmental wear and tear. This, in turn, leads to lower maintenance costs and improved overall efficiency. As technology continues to advance, the versatility and effectiveness of air-supported radomes in both extreme and general environments are expected to drive further adoption and innovation in this market.

Global Air-Supported Radome Market Outlook:

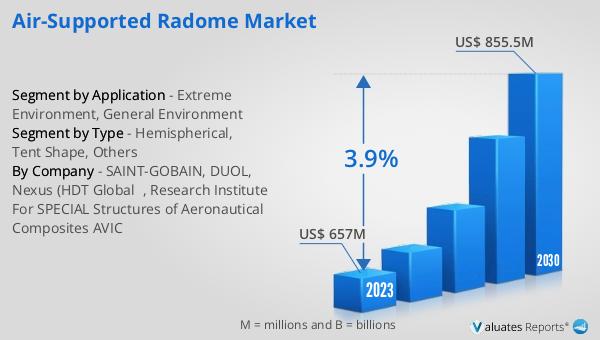

The global Air-Supported Radome market was valued at $657 million in 2023 and is projected to reach $855.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.9% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for advanced protective solutions for radar and communication systems across various industries. The market's expansion can be attributed to the rising need for reliable and durable radomes that can withstand harsh environmental conditions while ensuring optimal performance. The versatility and efficiency of air-supported radomes make them an attractive option for organizations looking to safeguard their critical equipment without compromising on functionality. As technology continues to evolve, the global Air-Supported Radome market is expected to see further innovations and improvements, enhancing their capabilities and expanding their range of applications. This positive market outlook underscores the importance of air-supported radomes in ensuring the reliability and longevity of radar and communication systems in both extreme and general environments.

| Report Metric | Details |

| Report Name | Air-Supported Radome Market |

| Accounted market size in 2023 | US$ 657 million |

| Forecasted market size in 2030 | US$ 855.5 million |

| CAGR | 3.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | SAINT-GOBAIN, DUOL, Nexus (HDT Global), Research Institute For SPECIAL Structures of Aeronautical Composites AVIC |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |