What is Global Electric Surgical Pendants Market?

The Global Electric Surgical Pendants Market refers to the worldwide industry focused on the production, distribution, and utilization of electric surgical pendants. These devices are essential in modern medical settings, providing a centralized system for managing various medical equipment and utilities such as gas, electrical outlets, and data communication ports. They are designed to enhance the efficiency and safety of surgical procedures by organizing and streamlining the workspace. Electric surgical pendants are commonly used in operating rooms, intensive care units, and other critical care areas within hospitals and clinics. Their ability to support a wide range of medical devices and facilitate easy access to essential utilities makes them indispensable in healthcare environments. The market for these devices is driven by the increasing demand for advanced healthcare infrastructure, the rising number of surgical procedures, and the growing emphasis on patient safety and operational efficiency. As healthcare facilities continue to modernize and expand, the need for reliable and versatile surgical pendants is expected to grow, making this market a vital component of the global medical device industry.

Single-arm Pendants, Double-arm Pendants in the Global Electric Surgical Pendants Market:

Single-arm pendants and double-arm pendants are two primary types of electric surgical pendants used in the Global Electric Surgical Pendants Market. Single-arm pendants are designed with a single, flexible arm that can be easily maneuvered to position medical equipment and utilities within the surgical workspace. These pendants are ideal for smaller operating rooms or areas where space is limited, as they provide a compact and efficient solution for organizing essential medical devices. Single-arm pendants typically feature multiple outlets for medical gases, electrical power, and data communication, allowing healthcare professionals to access all necessary utilities from a single, centralized location. This design not only enhances the efficiency of surgical procedures but also improves patient safety by reducing clutter and minimizing the risk of equipment-related accidents. On the other hand, double-arm pendants are equipped with two flexible arms, offering greater versatility and reach compared to single-arm pendants. The dual-arm design allows for more extensive coverage of the surgical workspace, making them suitable for larger operating rooms or areas with more complex medical equipment requirements. Double-arm pendants can support a higher number of outlets and devices, providing healthcare professionals with even greater access to essential utilities. This increased capacity and flexibility make double-arm pendants an ideal choice for advanced surgical procedures and specialized medical applications. Additionally, the dual-arm design allows for better weight distribution and stability, ensuring that the pendant remains securely in place during use. Both single-arm and double-arm pendants play a crucial role in enhancing the functionality and efficiency of modern healthcare facilities. By providing a centralized system for managing medical equipment and utilities, these pendants help streamline surgical procedures, reduce clutter, and improve overall patient safety. The choice between single-arm and double-arm pendants depends on the specific needs and requirements of the healthcare facility, with each type offering unique advantages in terms of flexibility, capacity, and coverage. As the demand for advanced healthcare infrastructure continues to grow, the Global Electric Surgical Pendants Market is expected to see increased adoption of both single-arm and double-arm pendants, driven by their ability to enhance the efficiency and safety of surgical procedures.

Hospital, Specialist Clinic, Others in the Global Electric Surgical Pendants Market:

The usage of electric surgical pendants in hospitals, specialist clinics, and other healthcare settings is a testament to their versatility and importance in modern medical practice. In hospitals, electric surgical pendants are primarily used in operating rooms and intensive care units. They provide a centralized system for managing medical equipment and utilities, ensuring that healthcare professionals have easy access to essential tools and resources during surgical procedures. The ability to organize and streamline the workspace helps reduce clutter, minimize the risk of equipment-related accidents, and improve overall patient safety. Additionally, the flexibility and maneuverability of electric surgical pendants allow for better positioning of medical devices, enhancing the efficiency and effectiveness of surgical interventions. In specialist clinics, electric surgical pendants are used to support a wide range of medical procedures, from minor surgeries to complex interventions. These clinics often require specialized equipment and utilities, and electric surgical pendants provide a convenient and efficient solution for managing these resources. The ability to customize the configuration of the pendant to meet the specific needs of the clinic ensures that healthcare professionals have access to the right tools and utilities at the right time. This not only improves the quality of care provided to patients but also enhances the overall operational efficiency of the clinic. The use of electric surgical pendants in specialist clinics is particularly beneficial in areas such as cardiology, neurology, and orthopedics, where precise and reliable access to medical equipment is critical. In other healthcare settings, such as outpatient surgery centers and emergency rooms, electric surgical pendants play a vital role in ensuring that medical equipment and utilities are readily available and easily accessible. These settings often require quick and efficient access to a wide range of medical devices, and electric surgical pendants provide a centralized system for managing these resources. The ability to position and maneuver the pendant as needed allows healthcare professionals to respond quickly to patient needs, improving the overall quality of care. Additionally, the use of electric surgical pendants helps reduce clutter and improve the organization of the workspace, creating a safer and more efficient environment for both patients and healthcare providers. Overall, the usage of electric surgical pendants in hospitals, specialist clinics, and other healthcare settings highlights their importance in modern medical practice. By providing a centralized system for managing medical equipment and utilities, these pendants help enhance the efficiency, safety, and effectiveness of surgical procedures and other medical interventions. As healthcare facilities continue to modernize and expand, the demand for reliable and versatile electric surgical pendants is expected to grow, further driving the development and adoption of these essential medical devices.

Global Electric Surgical Pendants Market Outlook:

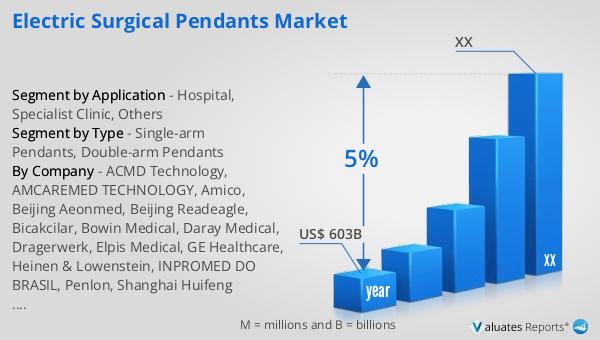

Based on our research, the global market for medical devices is projected to reach approximately $603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This substantial market size underscores the critical role that medical devices, including electric surgical pendants, play in the healthcare industry. The steady growth rate reflects the increasing demand for advanced medical technologies and the continuous efforts to improve patient care and operational efficiency in healthcare facilities worldwide. As the market expands, it presents numerous opportunities for innovation and development in the field of medical devices, driving advancements that can further enhance the quality of healthcare services. The projected growth also highlights the importance of investing in research and development to create more efficient, reliable, and versatile medical devices that can meet the evolving needs of healthcare providers and patients. This positive market outlook serves as a strong indicator of the ongoing and future significance of medical devices in the global healthcare landscape.

| Report Metric | Details |

| Report Name | Electric Surgical Pendants Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | ACMD Technology, AMCAREMED TECHNOLOGY, Amico, Beijing Aeonmed, Beijing Readeagle, Bicakcilar, Bowin Medical, Daray Medical, Dragerwerk, Elpis Medical, GE Healthcare, Heinen & Lowenstein, INPROMED DO BRASIL, Penlon, Shanghai Huifeng Medical Instrument, Shenzhen Mindray Bio-Medical Electronics, Spacelabs Healthcare, St. Francis Medical Equipment, TECHNOMED INDIA, VG MEDICAL |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |