What is Global Semi-automated Haemostasis Analyzers Market?

The Global Semi-automated Haemostasis Analyzers Market is a specialized segment within the broader medical devices industry, focusing on devices that assist in the analysis of blood clotting processes. These analyzers are crucial for diagnosing and monitoring conditions related to haemostasis, which is the body's process of stopping bleeding and maintaining blood in a fluid state within the vascular system. Semi-automated haemostasis analyzers combine manual and automated processes to deliver accurate and timely results, making them indispensable in clinical settings. They are designed to perform a variety of tests, including prothrombin time (PT), activated partial thromboplastin time (aPTT), and fibrinogen levels, among others. These tests are essential for diagnosing bleeding disorders, monitoring anticoagulant therapy, and assessing the risk of thrombosis. The market for these devices is driven by the increasing prevalence of blood-related disorders, advancements in technology, and the growing demand for point-of-care testing. Additionally, the aging global population and the rising incidence of chronic diseases further fuel the need for efficient haemostasis analyzers. As healthcare systems worldwide strive for better diagnostic tools, the demand for semi-automated haemostasis analyzers is expected to continue its upward trajectory.

Single Channel, Multiple Channels in the Global Semi-automated Haemostasis Analyzers Market:

In the Global Semi-automated Haemostasis Analyzers Market, devices can be categorized based on the number of channels they possess, namely single-channel and multiple-channel analyzers. Single-channel haemostasis analyzers are designed to perform one test at a time, making them suitable for smaller laboratories or settings with lower test volumes. These analyzers are typically more affordable and easier to operate, requiring minimal training for healthcare professionals. They are ideal for point-of-care testing and can provide quick results, which is crucial in emergency situations or for patients requiring immediate diagnosis and treatment. On the other hand, multiple-channel haemostasis analyzers are capable of performing several tests simultaneously, making them more suitable for larger laboratories or hospitals with high test volumes. These analyzers are more complex and often come with advanced features such as automated sample handling, data management systems, and connectivity options for integration with laboratory information systems (LIS). Multiple-channel analyzers offer higher throughput, which can significantly reduce turnaround times and improve laboratory efficiency. They are particularly beneficial in settings where a large number of tests need to be processed quickly, such as in hospitals with busy emergency departments or specialized coagulation laboratories. The choice between single-channel and multiple-channel analyzers depends on various factors, including the volume of tests, budget constraints, and the specific needs of the healthcare facility. While single-channel analyzers offer simplicity and cost-effectiveness, multiple-channel analyzers provide higher efficiency and advanced functionalities. Both types of analyzers play a crucial role in the diagnosis and management of haemostasis-related conditions, contributing to better patient outcomes and more efficient healthcare delivery.

Hospitals, Research Institutes, Others in the Global Semi-automated Haemostasis Analyzers Market:

The usage of Global Semi-automated Haemostasis Analyzers Market spans across various healthcare settings, including hospitals, research institutes, and other medical facilities. In hospitals, these analyzers are essential tools in the diagnosis and management of patients with bleeding disorders, thrombotic conditions, and those undergoing anticoagulant therapy. They are used in emergency departments, intensive care units, and surgical wards to provide rapid and accurate haemostasis testing, which is critical for timely clinical decision-making. The ability to quickly assess a patient's coagulation status can significantly impact treatment outcomes, particularly in acute settings where delays can be life-threatening. Research institutes also rely heavily on semi-automated haemostasis analyzers for various studies related to blood coagulation and haemostasis. These devices enable researchers to conduct detailed analyses of blood samples, facilitating the development of new diagnostic methods, therapeutic approaches, and a deeper understanding of haemostatic mechanisms. The precision and reliability of these analyzers are crucial for generating valid and reproducible research data, which can ultimately lead to advancements in medical science and improved patient care. Other medical facilities, such as specialized clinics and diagnostic laboratories, also utilize semi-automated haemostasis analyzers to offer comprehensive coagulation testing services. These facilities often serve as referral centers for complex cases requiring specialized haemostasis assessments. The versatility and efficiency of semi-automated analyzers make them suitable for a wide range of applications, from routine screening to specialized diagnostic testing. Overall, the widespread use of semi-automated haemostasis analyzers across different healthcare settings underscores their importance in modern medical practice. By providing accurate and timely haemostasis testing, these devices play a vital role in improving patient outcomes, advancing medical research, and enhancing the overall efficiency of healthcare delivery.

Global Semi-automated Haemostasis Analyzers Market Outlook:

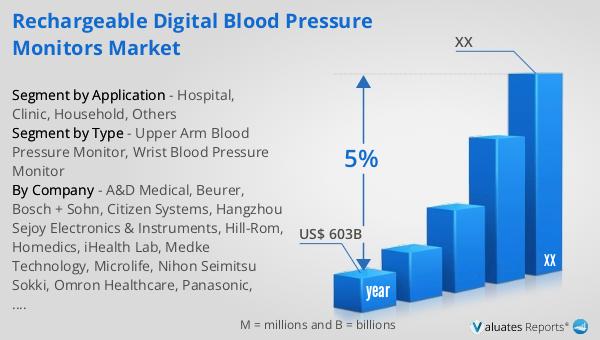

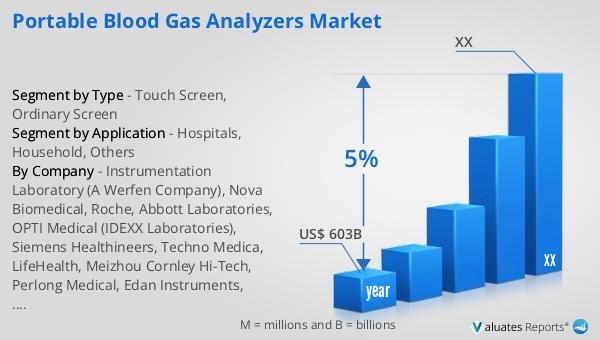

According to our research, the global market for medical devices is projected to reach approximately US$ 603 billion by the year 2023, with an anticipated growth rate of 5% CAGR over the next six years. This substantial market size reflects the increasing demand for advanced medical technologies and devices, driven by factors such as the aging population, rising prevalence of chronic diseases, and ongoing advancements in medical science. The growth trajectory of the medical devices market indicates a robust expansion, with significant opportunities for innovation and development. As healthcare systems worldwide continue to evolve, the need for efficient, reliable, and cutting-edge medical devices becomes more pronounced. This growth is not only limited to developed regions but also extends to emerging markets, where improving healthcare infrastructure and increasing healthcare expenditure are driving the adoption of advanced medical technologies. The projected growth rate of 5% CAGR underscores the dynamic nature of the medical devices industry, highlighting the continuous efforts to enhance patient care, improve diagnostic accuracy, and streamline therapeutic interventions. As the market expands, stakeholders, including manufacturers, healthcare providers, and policymakers, must collaborate to address challenges such as regulatory compliance, cost-effectiveness, and accessibility to ensure that the benefits of advanced medical devices are widely accessible.

| Report Metric | Details |

| Report Name | Semi-automated Haemostasis Analyzers Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Stago Group (HemoSonics), Grifols, Haemonetics, Roche Diagnostics, Abbott (Alere), Sysmex Corporation, Nihon Kohden, Thermo Fisher Scientific, Siemens, Helena Laboratories, Instrumentation Laboratory (Werfen), Medcaptain Medical Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |