What is Global Immunochemistry Diagnostic Device Market?

The Global Immunochemistry Diagnostic Device Market encompasses a wide range of devices and technologies used to detect and measure specific proteins, hormones, and other substances in the body. These devices are crucial in diagnosing various diseases and conditions by analyzing blood, urine, and other bodily fluids. Immunochemistry diagnostic devices use antibodies as a key component to identify and quantify substances, making them highly specific and sensitive. The market includes various types of analyzers and systems, each designed for different applications and levels of complexity. These devices are used in hospitals, diagnostic laboratories, research institutions, and other healthcare settings. The growing prevalence of chronic diseases, advancements in technology, and increasing awareness about early disease detection are driving the demand for these diagnostic devices globally. As healthcare systems worldwide strive to improve diagnostic accuracy and patient outcomes, the Global Immunochemistry Diagnostic Device Market is expected to continue its growth trajectory.

Chemiluminescence Immunoassay (CLIA) Analyzers, Immuno Fluorescence (IFA) Analyzers, Enzyme Immunoassay (EIA) Analyzers, Radioimmunoassay (RIA) Analyzers, Enzyme Linked Fluorescent Assay (ELFA) Systems, Multiplexed Assay Systems in the Global Immunochemistry Diagnostic Device Market:

Chemiluminescence Immunoassay (CLIA) Analyzers are a type of immunochemistry diagnostic device that uses chemiluminescent labels to detect the presence of specific substances in a sample. These analyzers are known for their high sensitivity and specificity, making them ideal for detecting low-abundance analytes. Immuno Fluorescence (IFA) Analyzers, on the other hand, use fluorescent labels to identify and quantify substances. They are widely used in autoimmune disease testing and infectious disease diagnostics due to their ability to provide rapid and accurate results. Enzyme Immunoassay (EIA) Analyzers utilize enzymes as labels to detect antigens or antibodies in a sample. These analyzers are commonly used in various diagnostic applications, including hormone level testing and infectious disease screening. Radioimmunoassay (RIA) Analyzers employ radioactive isotopes as labels, offering high sensitivity and precision. Despite their effectiveness, the use of radioactive materials requires stringent regulatory compliance and safety measures. Enzyme Linked Fluorescent Assay (ELFA) Systems combine the principles of enzyme immunoassay and fluorescence detection, providing a robust and versatile platform for various diagnostic tests. Multiplexed Assay Systems are designed to simultaneously detect multiple analytes in a single sample, increasing efficiency and throughput. These systems are particularly useful in research and clinical settings where comprehensive profiling of biomarkers is required. Each of these analyzers and systems plays a crucial role in the Global Immunochemistry Diagnostic Device Market, catering to different diagnostic needs and enhancing the overall capability of healthcare providers to diagnose and monitor diseases accurately.

Endocrinology, Oncology, Cardiology, Therapeutic Drug Development and Monitoring, Infectious Disease Testing, Drugs Of Abuse Testing, Others in the Global Immunochemistry Diagnostic Device Market:

The usage of Global Immunochemistry Diagnostic Device Market spans several critical areas of healthcare, including endocrinology, oncology, cardiology, therapeutic drug development and monitoring, infectious disease testing, and drugs of abuse testing. In endocrinology, these devices are used to measure hormone levels, aiding in the diagnosis and management of conditions such as diabetes, thyroid disorders, and adrenal gland dysfunctions. In oncology, immunochemistry diagnostic devices help in detecting tumor markers, which are substances produced by cancer cells or by the body in response to cancer. This aids in early cancer detection, monitoring treatment efficacy, and assessing the risk of recurrence. In cardiology, these devices are used to measure cardiac biomarkers, which are crucial in diagnosing heart attacks, heart failure, and other cardiovascular diseases. Therapeutic drug development and monitoring benefit from these devices by enabling precise measurement of drug levels in the body, ensuring optimal dosing and minimizing adverse effects. Infectious disease testing is another significant application, where these devices detect specific antigens or antibodies related to pathogens such as bacteria, viruses, and fungi. This is essential for timely diagnosis and treatment of infections. Drugs of abuse testing utilizes immunochemistry diagnostic devices to detect the presence of illicit drugs and their metabolites in biological samples, playing a vital role in substance abuse programs and workplace drug testing. Other applications include allergy testing, autoimmune disease diagnostics, and reproductive health assessments. The versatility and accuracy of immunochemistry diagnostic devices make them indispensable tools in modern healthcare, contributing to improved patient outcomes and more efficient disease management.

Global Immunochemistry Diagnostic Device Market Outlook:

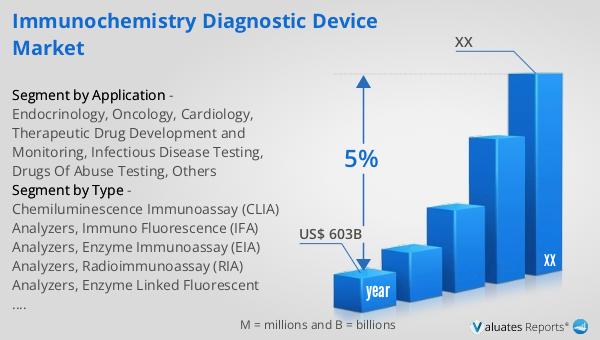

Based on our research, the global market for medical devices is projected to reach approximately US$ 603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including technological advancements, increasing prevalence of chronic diseases, and rising healthcare expenditure worldwide. The demand for innovative and efficient diagnostic devices is on the rise as healthcare providers seek to improve diagnostic accuracy and patient care. Immunochemistry diagnostic devices, in particular, are gaining traction due to their ability to provide precise and rapid results, which are crucial for early disease detection and effective treatment planning. The market's expansion is also supported by the growing adoption of point-of-care testing and personalized medicine, which rely heavily on advanced diagnostic technologies. As healthcare systems continue to evolve and prioritize patient-centric approaches, the role of immunochemistry diagnostic devices is expected to become even more significant. The ongoing research and development efforts in this field are likely to yield new and improved diagnostic solutions, further propelling market growth. Overall, the Global Immunochemistry Diagnostic Device Market is poised for substantial growth, driven by the increasing need for accurate and timely diagnostics in various medical disciplines.

| Report Metric | Details |

| Report Name | Immunochemistry Diagnostic Device Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Abbott, Roche Diagnostics, Siemens Healthcare Diagnostics, Diamond Diagnostics, Dynex Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |