What is Global Vaccine Vial Rubber Stopper Market?

The Global Vaccine Vial Rubber Stopper Market is a specialized segment within the broader pharmaceutical and medical supplies industry. These rubber stoppers are essential components used to seal vaccine vials, ensuring the sterility and integrity of the vaccine contents. They are designed to withstand various conditions, including temperature fluctuations and chemical interactions, to maintain the efficacy of the vaccines. The market for these rubber stoppers is driven by the increasing demand for vaccines worldwide, especially in light of recent global health challenges. Manufacturers are focusing on producing high-quality, durable, and safe rubber stoppers to meet stringent regulatory standards and the growing needs of the healthcare sector. The market encompasses various types of rubber stoppers, including those made from butyl rubber, which is known for its excellent barrier properties against gases and moisture. The global reach of this market is significant, with major players operating in North America, Europe, Asia-Pacific, and other regions, catering to both large pharmaceutical companies and smaller biotech firms. The continuous advancements in vaccine development and the expansion of immunization programs globally are expected to sustain the demand for vaccine vial rubber stoppers in the coming years.

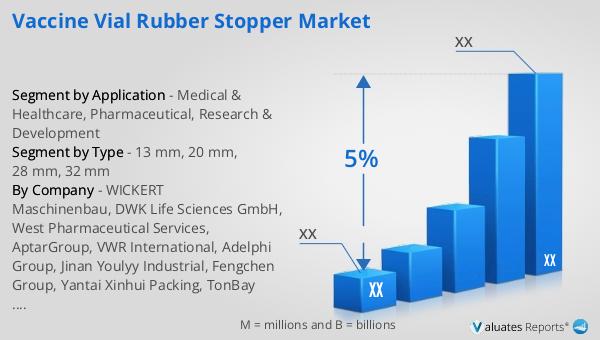

13 mm, 20 mm, 28 mm, 32 mm in the Global Vaccine Vial Rubber Stopper Market:

In the Global Vaccine Vial Rubber Stopper Market, the sizes of the stoppers play a crucial role in their application and compatibility with different vial types. The 13 mm, 20 mm, 28 mm, and 32 mm rubber stoppers are among the most commonly used sizes. The 13 mm stoppers are typically used for smaller vials, often containing single-dose vaccines. These stoppers are designed to provide a secure seal while allowing easy access for syringes. The 20 mm stoppers are more versatile and are used for both single-dose and multi-dose vials. They offer a balance between ease of use and security, making them a popular choice in the pharmaceutical industry. The 28 mm and 32 mm stoppers are generally used for larger vials, which may contain multiple doses or bulk quantities of vaccines. These larger stoppers need to provide a robust seal to prevent contamination and ensure the stability of the vaccine over time. Each size of rubber stopper must meet specific regulatory requirements and undergo rigorous testing to ensure they do not interact negatively with the vaccine contents. The material composition of these stoppers is also critical, with butyl rubber being a preferred choice due to its low permeability to gases and moisture, which helps in maintaining the sterility and potency of the vaccines. The manufacturing process of these stoppers involves precision molding and stringent quality control measures to ensure consistency and reliability. The demand for different sizes of rubber stoppers is influenced by the types of vaccines being produced and the packaging preferences of pharmaceutical companies. For instance, during the COVID-19 pandemic, there was a significant increase in the production of vaccines, leading to a surge in demand for various sizes of rubber stoppers to accommodate different vial types. The global distribution of these stoppers requires a well-coordinated supply chain to ensure timely delivery to vaccine manufacturers across different regions. The market for these rubber stoppers is highly competitive, with several key players investing in research and development to innovate and improve the performance of their products. The focus is on enhancing the safety, compatibility, and ease of use of these stoppers to meet the evolving needs of the pharmaceutical industry. As vaccine development continues to advance, the demand for high-quality rubber stoppers in various sizes is expected to remain strong, driven by the need for effective and safe vaccine delivery systems.

Medical & Healthcare, Pharmaceutical, Research & Development in the Global Vaccine Vial Rubber Stopper Market:

The usage of Global Vaccine Vial Rubber Stopper Market spans across several critical areas, including Medical & Healthcare, Pharmaceutical, and Research & Development. In the Medical & Healthcare sector, these rubber stoppers are vital for ensuring the safe storage and administration of vaccines. They help maintain the sterility of the vaccine vials, preventing contamination and ensuring that the vaccines remain effective until they are administered to patients. Healthcare providers rely on these stoppers to deliver vaccines safely and efficiently, which is crucial for immunization programs and disease prevention efforts. In the Pharmaceutical industry, rubber stoppers are an integral part of the vaccine production and packaging process. Pharmaceutical companies use these stoppers to seal vaccine vials during the manufacturing process, ensuring that the vaccines are protected from external contaminants and environmental factors. The stoppers also play a role in maintaining the stability and potency of the vaccines during storage and transportation. This is particularly important for vaccines that require specific storage conditions, such as refrigeration or freezing. In the Research & Development sector, rubber stoppers are used in the development and testing of new vaccines. Researchers use these stoppers to seal vials containing experimental vaccines, ensuring that the samples remain uncontaminated and stable throughout the testing process. The stoppers also allow for easy access to the vaccine contents for testing and analysis. This is crucial for the development of new vaccines, as it ensures that the samples remain viable and accurate results can be obtained. Overall, the usage of rubber stoppers in these areas is essential for the safe and effective delivery of vaccines, from development and production to storage and administration.

Global Vaccine Vial Rubber Stopper Market Outlook:

The global pharmaceutical market was valued at approximately 1475 billion USD in 2022, with an expected compound annual growth rate (CAGR) of 5% over the next six years. In comparison, the chemical drug market saw an increase from 1005 billion USD in 2018 to an estimated 1094 billion USD in 2022. This growth reflects the expanding demand for pharmaceutical products and the continuous advancements in drug development and healthcare solutions. The pharmaceutical market encompasses a wide range of products, including prescription medications, over-the-counter drugs, and vaccines, all of which contribute to the overall market value. The increase in the chemical drug market highlights the ongoing innovation and investment in the development of new chemical-based therapies and treatments. This growth is driven by factors such as the rising prevalence of chronic diseases, an aging population, and the increasing focus on personalized medicine. The pharmaceutical industry plays a crucial role in improving global health outcomes, and the continued growth of this market is essential for meeting the healthcare needs of populations worldwide. The data underscores the importance of the pharmaceutical sector in driving economic growth and advancing medical science.

| Report Metric | Details |

| Report Name | Vaccine Vial Rubber Stopper Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | WICKERT Maschinenbau, DWK Life Sciences GmbH, West Pharmaceutical Services, AptarGroup, VWR International, Adelphi Group, Jinan Youlyy Industrial, Fengchen Group, Yantai Xinhui Packing, TonBay Industry, Shandong Province Medicinal Glass |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |