What is Global Oil-water Separation Purifier Market?

The Global Oil-water Separation Purifier Market refers to the industry focused on the development, production, and distribution of devices designed to separate oil from water. These purifiers are essential in various industries where oil contamination in water can pose significant environmental and operational challenges. The primary function of these purifiers is to ensure that water discharged from industrial processes is free from oil pollutants, thereby protecting water bodies and complying with environmental regulations. The market encompasses a wide range of technologies and products, from simple mechanical separators to advanced filtration systems that use coalescing filters, gravity separation, and other sophisticated methods. The demand for oil-water separation purifiers is driven by stringent environmental laws, the need for sustainable industrial practices, and the increasing awareness of the importance of water conservation. Industries such as oil and gas, chemical manufacturing, food processing, and automotive heavily rely on these purifiers to maintain operational efficiency and environmental compliance. The market is characterized by continuous innovation, with companies investing in research and development to enhance the efficiency, reliability, and cost-effectiveness of their products.

Hydraulic Type, Sealed Type in the Global Oil-water Separation Purifier Market:

In the Global Oil-water Separation Purifier Market, two prominent types of purifiers are the Hydraulic Type and the Sealed Type. The Hydraulic Type oil-water separation purifiers operate based on the principle of gravity separation. These systems use the difference in density between oil and water to separate the two substances. The oil, being less dense, floats on top of the water and can be skimmed off or collected in a separate chamber. Hydraulic Type purifiers are widely used in industries where large volumes of water need to be treated, such as in oil refineries, petrochemical plants, and large-scale manufacturing facilities. These systems are known for their robustness and ability to handle high flow rates, making them suitable for heavy-duty applications. On the other hand, Sealed Type oil-water separation purifiers are designed to operate in a closed system, preventing the escape of volatile organic compounds (VOCs) and other hazardous substances into the atmosphere. These purifiers are particularly useful in industries where the handling of toxic or flammable liquids is common, such as in chemical manufacturing and pharmaceuticals. The sealed design ensures that the separation process is contained, reducing the risk of environmental contamination and improving safety. Sealed Type purifiers often incorporate advanced filtration technologies, such as coalescing filters and membrane filtration, to achieve high levels of separation efficiency. These systems are typically more compact and can be integrated into existing industrial processes with minimal disruption. Both Hydraulic and Sealed Type purifiers play a crucial role in maintaining environmental compliance and operational efficiency across various industries. The choice between the two types depends on the specific requirements of the application, including the volume of water to be treated, the nature of the contaminants, and the regulatory standards that need to be met. As industries continue to prioritize sustainability and environmental protection, the demand for efficient and reliable oil-water separation purifiers is expected to grow, driving further innovation and development in this market.

Chemical Industry, Food Industry, Automobile Industry in the Global Oil-water Separation Purifier Market:

The Global Oil-water Separation Purifier Market finds extensive usage across several key industries, including the Chemical Industry, Food Industry, and Automobile Industry. In the Chemical Industry, oil-water separation purifiers are essential for managing wastewater generated during the production of chemicals, pharmaceuticals, and other related products. Chemical manufacturing processes often involve the use of various oils and solvents, which can contaminate water streams. Effective separation of these contaminants is crucial to prevent environmental pollution and to comply with stringent wastewater discharge regulations. Oil-water separation purifiers help chemical plants to treat their wastewater efficiently, ensuring that harmful substances are removed before the water is released into the environment or reused within the facility. In the Food Industry, oil-water separation purifiers play a vital role in maintaining hygiene and safety standards. Food processing operations, such as frying, cooking, and cleaning, generate wastewater that contains oils and fats. If not properly treated, this wastewater can lead to blockages in drainage systems and pose a risk to the environment. Oil-water separation purifiers help food processing plants to effectively remove oils and fats from their wastewater, ensuring that it meets regulatory standards for discharge or reuse. This not only helps in maintaining a clean and safe working environment but also supports the industry's sustainability goals by reducing water consumption and minimizing waste. In the Automobile Industry, oil-water separation purifiers are used in various applications, including vehicle washing, maintenance, and manufacturing processes. Automotive facilities generate wastewater that contains oils, greases, and other contaminants from vehicle engines, parts, and cleaning operations. Proper treatment of this wastewater is essential to prevent environmental pollution and to comply with environmental regulations. Oil-water separation purifiers help automotive facilities to efficiently remove oil and grease from their wastewater, ensuring that it can be safely discharged or reused. This not only helps in protecting the environment but also supports the industry's efforts to reduce water consumption and improve operational efficiency. Overall, the usage of oil-water separation purifiers in these industries highlights their importance in promoting environmental sustainability, regulatory compliance, and operational efficiency.

Global Oil-water Separation Purifier Market Outlook:

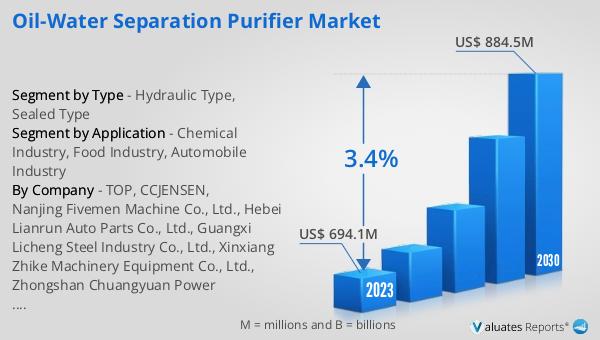

The global Oil-water Separation Purifier market, valued at US$ 694.1 million in 2023, is projected to grow to US$ 884.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.4% during the forecast period from 2024 to 2030. This growth indicates a steady increase in demand for oil-water separation purifiers across various industries. The rising awareness about environmental protection, coupled with stringent regulations on wastewater discharge, is driving the adoption of these purifiers. Industries such as oil and gas, chemical manufacturing, food processing, and automotive are increasingly investing in advanced oil-water separation technologies to ensure compliance with environmental standards and to promote sustainable practices. The market's growth is also fueled by continuous innovation and technological advancements, which are enhancing the efficiency and reliability of oil-water separation purifiers. Companies are focusing on developing cost-effective solutions that can handle large volumes of wastewater and effectively remove oil contaminants. As a result, the market is witnessing the introduction of new products and technologies that cater to the evolving needs of various industries. The projected growth of the global Oil-water Separation Purifier market underscores the importance of these devices in promoting environmental sustainability and operational efficiency.

| Report Metric | Details |

| Report Name | Oil-water Separation Purifier Market |

| Accounted market size in 2023 | US$ 694.1 million |

| Forecasted market size in 2030 | US$ 884.5 million |

| CAGR | 3.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TOP, CCJENSEN, Nanjing Fivemen Machine Co., Ltd., Hebei Lianrun Auto Parts Co., Ltd., Guangxi Licheng Steel Industry Co., Ltd., Xinxiang Zhike Machinery Equipment Co., Ltd., Zhongshan Chuangyuan Power Equipment Co., Ltd., Highland Tank, PureBilge, PEWE LLC, Huilide Electric, RWO, Conder Environmental Solutions, PS International, Compass Water |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |