What is Global Hot Melt Adhesive Film for Underwear Market?

The Global Hot Melt Adhesive Film for Underwear Market refers to the industry that produces and supplies adhesive films specifically designed for use in underwear manufacturing. These films are used to bond fabrics and other materials together without the need for sewing, providing a seamless and comfortable finish. Hot melt adhesive films are activated by heat, which melts the adhesive and allows it to bond with the fabric. Once cooled, the adhesive solidifies, creating a strong and durable bond. This technology is particularly useful in the underwear market as it enhances the comfort and appearance of the garments by eliminating bulky seams and stitches. The market for these adhesive films is driven by the increasing demand for high-quality, comfortable, and aesthetically pleasing underwear. Manufacturers are continuously innovating to develop films that offer better adhesion, flexibility, and durability to meet the evolving needs of consumers.

TPU Hot Melt Adhesive Film, EVA Hot Melt Adhesive Film, PA Hot Melt Adhesive Film, PES Hot Melt Adhesive Film in the Global Hot Melt Adhesive Film for Underwear Market:

TPU (Thermoplastic Polyurethane) Hot Melt Adhesive Film is known for its excellent elasticity, abrasion resistance, and transparency. It is widely used in the underwear market due to its ability to provide a soft and comfortable feel while maintaining strong adhesion. TPU films are also highly resistant to oils and chemicals, making them ideal for intimate apparel that requires frequent washing. EVA (Ethylene Vinyl Acetate) Hot Melt Adhesive Film, on the other hand, is valued for its flexibility, low-temperature bonding, and cost-effectiveness. EVA films are often used in applications where a softer bond is required, such as in delicate fabrics and lace used in underwear. PA (Polyamide) Hot Melt Adhesive Film is known for its high melting point and excellent adhesion to a variety of fabrics. It is particularly useful in applications that require strong and durable bonds, such as in sports and performance underwear. PA films also offer good resistance to washing and dry cleaning, ensuring the longevity of the garments. PES (Polyester) Hot Melt Adhesive Film is characterized by its high strength and durability. It is commonly used in underwear that requires a strong bond and resistance to high temperatures. PES films are also known for their excellent adhesion to synthetic fabrics, making them ideal for use in modern, high-performance underwear. Each type of hot melt adhesive film offers unique properties that cater to different needs in the underwear market, allowing manufacturers to choose the best material for their specific applications.

Online Sales, Offline Sales in the Global Hot Melt Adhesive Film for Underwear Market:

The usage of Global Hot Melt Adhesive Film for Underwear Market in online sales has seen significant growth in recent years. Online platforms provide a convenient and accessible way for consumers to purchase underwear, and the use of hot melt adhesive films enhances the quality and comfort of these products. E-commerce websites often highlight the benefits of seamless and comfortable underwear, which is made possible by the use of these adhesive films. The ability to showcase detailed product descriptions, customer reviews, and high-quality images helps consumers make informed purchasing decisions. Additionally, online sales channels allow manufacturers to reach a global audience, expanding their market reach and increasing sales. On the other hand, offline sales, which include physical retail stores and specialty shops, continue to play a crucial role in the underwear market. Consumers often prefer to physically inspect and try on underwear before making a purchase, and the use of hot melt adhesive films ensures that the products meet their expectations in terms of comfort and quality. Retail stores can provide personalized customer service, allowing shoppers to receive recommendations and assistance in finding the right fit and style. The tactile experience of feeling the softness and flexibility of the adhesive films in the garments can significantly influence purchasing decisions. Both online and offline sales channels complement each other, providing consumers with multiple options to purchase high-quality underwear made with hot melt adhesive films.

Global Hot Melt Adhesive Film for Underwear Market Outlook:

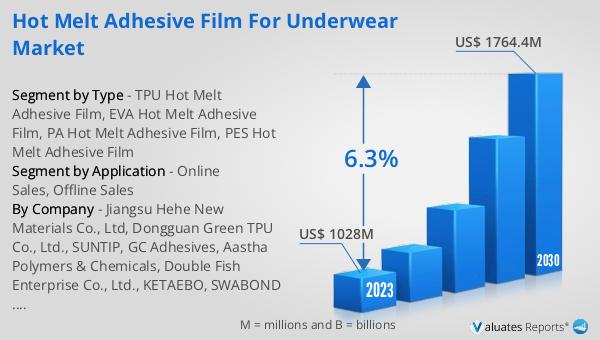

The global Hot Melt Adhesive Film for Underwear market was valued at US$ 1028 million in 2023 and is anticipated to reach US$ 1764.4 million by 2030, witnessing a CAGR of 6.3% during the forecast period 2024-2030. This market outlook indicates a robust growth trajectory driven by the increasing demand for comfortable and high-quality underwear. The use of hot melt adhesive films in underwear manufacturing has revolutionized the industry by providing seamless and durable bonds that enhance the overall comfort and appearance of the garments. As consumers become more aware of the benefits of these adhesive films, the demand for underwear made with this technology is expected to rise. Manufacturers are continuously innovating to develop advanced adhesive films that offer better performance and meet the evolving needs of consumers. The projected growth in the market reflects the increasing adoption of hot melt adhesive films in the underwear industry and the expanding market reach through both online and offline sales channels.

| Report Metric | Details |

| Report Name | Hot Melt Adhesive Film for Underwear Market |

| Accounted market size in 2023 | US$ 1028 million |

| Forecasted market size in 2030 | US$ 1764.4 million |

| CAGR | 6.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Jiangsu Hehe New Materials Co., Ltd, Dongguan Green TPU Co., Ltd., SUNTIP, GC Adhesives, Aastha Polymers & Chemicals, Double Fish Enterprise Co., Ltd., KETAEBO, SWABOND THK, FuRong, Nan Pao, SIBUR, Impex Global, LLC, MANUCOR SPA, Gettel Group, FlexFilm |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |