What is Global PTCA Coronary Balloon Catheter Market?

The Global PTCA Coronary Balloon Catheter Market refers to the worldwide market for devices used in percutaneous transluminal coronary angioplasty (PTCA) procedures. These catheters are specialized medical tools designed to open up blocked or narrowed coronary arteries, which can improve blood flow to the heart muscle and alleviate symptoms of heart disease such as chest pain and shortness of breath. The market encompasses various types of PTCA balloon catheters, each tailored to specific medical needs and procedural requirements. These devices are crucial in the treatment of coronary artery disease, a leading cause of morbidity and mortality globally. The market is driven by factors such as the increasing prevalence of cardiovascular diseases, advancements in medical technology, and the growing demand for minimally invasive surgical procedures.

Quick Exchange Type, Overall Exchange Type, Fixed Guide Wire Type, Perfusion Type in the Global PTCA Coronary Balloon Catheter Market:

In the Global PTCA Coronary Balloon Catheter Market, there are several types of catheters designed to meet different clinical needs and procedural preferences. The Quick Exchange Type catheter is designed for ease of use, allowing for rapid catheter exchanges during procedures. This type is particularly beneficial in complex cases where multiple balloon catheters may be needed. The Overall Exchange Type catheter, on the other hand, is designed for situations where the entire catheter needs to be exchanged. This type is often used in procedures where precise control and positioning of the catheter are critical. The Fixed Guide Wire Type catheter integrates the guide wire into the catheter itself, which can simplify the procedure and reduce the risk of complications. This type is especially useful in challenging anatomical situations where maintaining guide wire position is crucial. The Perfusion Type catheter is designed to allow blood flow to continue through the artery during the procedure, which can be particularly important in patients with compromised coronary circulation. Each of these catheter types has its own set of advantages and is chosen based on the specific needs of the patient and the preferences of the healthcare provider. The diversity of catheter types in the market reflects the complexity of coronary artery disease and the need for tailored treatment approaches.

Hospital, Clinic in the Global PTCA Coronary Balloon Catheter Market:

The usage of PTCA Coronary Balloon Catheters in hospitals and clinics is integral to the management of coronary artery disease. In hospitals, these catheters are used in catheterization labs, where interventional cardiologists perform angioplasty procedures. The hospital setting provides the necessary infrastructure and support for these complex procedures, including advanced imaging technologies, skilled medical personnel, and emergency care capabilities. Hospitals often handle more severe cases of coronary artery disease, including patients with multiple comorbidities or those requiring urgent intervention. The availability of a wide range of PTCA balloon catheters in hospitals ensures that healthcare providers can choose the most appropriate device for each patient, enhancing the likelihood of successful outcomes. In clinics, PTCA Coronary Balloon Catheters are used in less acute settings, often for elective procedures. Clinics may cater to patients with stable coronary artery disease who require intervention to improve their quality of life and prevent future cardiac events. The use of these catheters in clinics allows for a more streamlined and patient-friendly experience, with shorter wait times and a more personalized approach to care. Both hospitals and clinics play a crucial role in the treatment of coronary artery disease, and the availability of PTCA Coronary Balloon Catheters in these settings is essential for providing high-quality, effective care to patients.

Global PTCA Coronary Balloon Catheter Market Outlook:

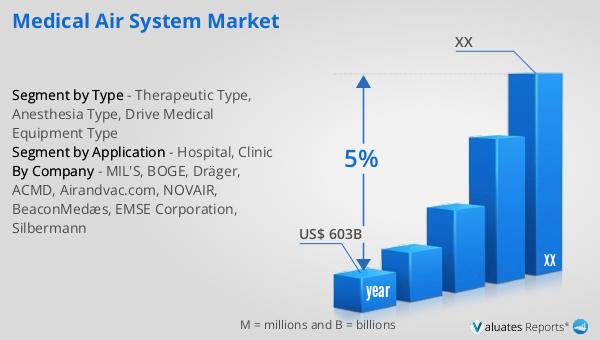

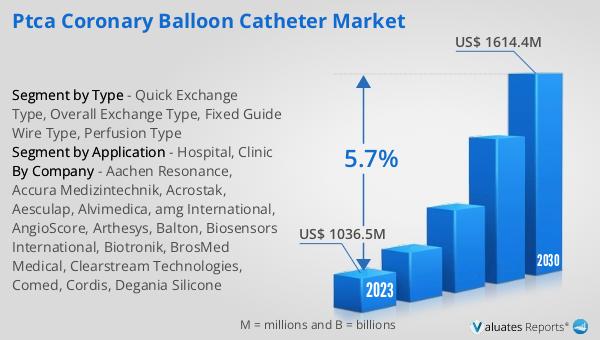

The global PTCA Coronary Balloon Catheter market was valued at US$ 1036.5 million in 2023 and is anticipated to reach US$ 1614.4 million by 2030, witnessing a CAGR of 5.7% during the forecast period 2024-2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% during the next six years. This growth is driven by the increasing prevalence of chronic diseases, advancements in medical technology, and the rising demand for minimally invasive procedures. The PTCA Coronary Balloon Catheter market is a significant segment within the broader medical device market, reflecting the critical role these devices play in the treatment of coronary artery disease. The market's growth is supported by ongoing research and development efforts, as well as the increasing adoption of advanced medical technologies in both developed and emerging markets.

| Report Metric | Details |

| Report Name | PTCA Coronary Balloon Catheter Market |

| Accounted market size in 2023 | US$ 1036.5 million |

| Forecasted market size in 2030 | US$ 1614.4 million |

| CAGR | 5.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Aachen Resonance, Accura Medizintechnik, Acrostak, Aesculap, Alvimedica, amg International, AngioScore, Arthesys, Balton, Biosensors International, Biotronik, BrosMed Medical, Clearstream Technologies, Comed, Cordis, Degania Silicone |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |