What is Global Industrial PDAs Market?

The global Industrial PDAs market is a dynamic and evolving sector that focuses on the production and distribution of Personal Digital Assistants (PDAs) specifically designed for industrial applications. These devices are rugged, durable, and equipped with advanced features to withstand harsh environments and demanding tasks. Industrial PDAs are used across various sectors such as manufacturing, logistics, transportation, government, and retail to streamline operations, enhance productivity, and improve data accuracy. They come with functionalities like barcode scanning, RFID, GPS, and wireless connectivity, making them indispensable tools for real-time data collection and management. The market for these devices is driven by the increasing need for automation, the rise in e-commerce activities, and the growing emphasis on operational efficiency. As industries continue to adopt digital solutions, the demand for industrial PDAs is expected to grow, offering significant opportunities for manufacturers and technology providers.

Android, Windows in the Global Industrial PDAs Market:

When it comes to the operating systems used in global industrial PDAs, Android and Windows are the two most prevalent platforms. Android-based industrial PDAs are popular due to their user-friendly interface, extensive app ecosystem, and flexibility. They offer a wide range of applications that can be customized to meet specific industrial needs. Android PDAs are often preferred in environments where ease of use and quick deployment are crucial. They support various industrial applications such as inventory management, field service, and asset tracking. On the other hand, Windows-based industrial PDAs are known for their robust security features, compatibility with enterprise systems, and reliability. They are widely used in sectors where data security and integration with existing IT infrastructure are paramount. Windows PDAs are particularly favored in industries like government and large-scale manufacturing, where stringent security protocols and seamless integration with enterprise resource planning (ERP) systems are essential. Both Android and Windows platforms offer unique advantages, and the choice between them often depends on the specific requirements of the industry and the nature of the tasks to be performed. The versatility of Android allows for a more flexible and adaptable approach, while the stability and security of Windows make it a preferred choice for more controlled and regulated environments. As technology continues to advance, both operating systems are expected to evolve, offering even more sophisticated features and capabilities to meet the growing demands of the industrial sector.

Industrial or Manufacturing, Logistics or Transport, Government, Retail, Other in the Global Industrial PDAs Market:

The usage of global industrial PDAs spans across various sectors, each benefiting from the unique features and capabilities of these devices. In the industrial or manufacturing sector, PDAs are used to streamline production processes, manage inventory, and ensure quality control. They enable real-time data collection and analysis, helping manufacturers to optimize their operations and reduce downtime. In logistics and transport, industrial PDAs play a crucial role in tracking shipments, managing fleet operations, and ensuring timely deliveries. They provide accurate and up-to-date information, enhancing the efficiency of supply chain management. Government agencies use industrial PDAs for tasks such as asset management, field inspections, and public safety operations. These devices help in maintaining accurate records, improving response times, and ensuring compliance with regulations. In the retail sector, industrial PDAs are used for inventory management, point-of-sale transactions, and customer service. They enable retailers to manage their stock levels efficiently, process transactions quickly, and provide better service to their customers. Other sectors, such as healthcare, utilities, and field services, also benefit from the use of industrial PDAs. These devices help in managing patient records, monitoring utility infrastructure, and conducting field inspections. The versatility and durability of industrial PDAs make them an invaluable tool across various industries, enhancing productivity, accuracy, and efficiency.

Global Industrial PDAs Market Outlook:

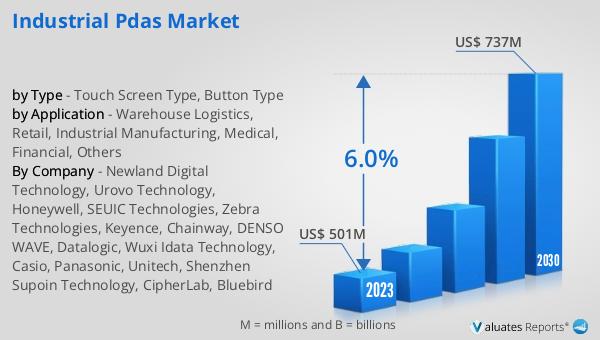

The global Industrial PDAs market was valued at US$ 1789 million in 2023 and is projected to grow significantly in the coming years. By 2030, the market is expected to reach US$ 2571 million, reflecting a compound annual growth rate (CAGR) of 4.6% during the forecast period from 2024 to 2030. This growth can be attributed to the increasing adoption of digital solutions across various industries, the need for real-time data collection and management, and the rising emphasis on operational efficiency. Industrial PDAs are becoming essential tools for businesses looking to streamline their operations, enhance productivity, and improve data accuracy. The market's expansion is also driven by technological advancements, such as the integration of advanced features like barcode scanning, RFID, GPS, and wireless connectivity. As industries continue to embrace digital transformation, the demand for industrial PDAs is expected to rise, offering significant opportunities for manufacturers and technology providers. The projected growth of the global Industrial PDAs market underscores the importance of these devices in modern industrial operations and highlights the potential for further innovation and development in this sector.

| Report Metric | Details |

| Report Name | Industrial PDAs Market |

| Accounted market size in 2023 | US$ 1789 million |

| Forecasted market size in 2030 | US$ 2571 million |

| CAGR | 4.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | ARBOR Technology, Zebra Technologies, Datalogic, CASIO, IEI Integration, Intermec, AXEM Technology, Custom Group, Emdoor Information, Mactron Group, MediaTek, Advantech, Beijing GFUVE Electronics, Shenzhen Swell Technology, Shandong Xintong Electronic, Guangzhou Jiebao Technology, Weiqiang Industry Computer |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |