What is Global High Voltage Testing Market?

The Global High Voltage Testing Market is a specialized sector focused on evaluating the performance and safety of electrical equipment that operates at high voltages. High voltage testing is crucial for ensuring the reliability and longevity of electrical systems, which are integral to various industries such as power generation, transmission, and distribution. This market encompasses a range of testing methods and equipment designed to assess the insulation and overall integrity of high voltage apparatus. These tests help in identifying potential faults, preventing failures, and ensuring compliance with international standards. The market is driven by the increasing demand for electricity, the expansion of power grids, and the need for regular maintenance and upgrading of existing infrastructure. High voltage testing is essential for both new installations and the maintenance of existing systems, making it a critical component of the electrical industry. The market includes various players, from equipment manufacturers to service providers, all working together to ensure the safe and efficient operation of high voltage electrical systems.

Sustained Low Frequency Test, Constant DC Test, High Frequency Test, Surge or Impulse Test in the Global High Voltage Testing Market:

In the Global High Voltage Testing Market, several testing methods are employed to ensure the reliability and safety of electrical systems. The Sustained Low Frequency Test is one such method, where a low-frequency voltage is applied to the equipment for an extended period. This test helps in identifying insulation weaknesses and potential breakdowns under normal operating conditions. The Constant DC Test involves applying a direct current voltage to the equipment to check for insulation integrity. This test is particularly useful for detecting moisture and other contaminants that may affect the performance of the insulation. The High Frequency Test, on the other hand, uses high-frequency alternating current to evaluate the dielectric properties of the insulation. This test is essential for identifying defects that may not be apparent under normal operating conditions. The Surge or Impulse Test is another critical method used in high voltage testing. This test involves applying a high-voltage surge or impulse to the equipment to simulate lightning strikes or switching surges. It helps in assessing the equipment's ability to withstand transient overvoltages and ensures that it can operate safely under extreme conditions. Each of these testing methods plays a vital role in the overall assessment of high voltage equipment, ensuring that it meets the required safety and performance standards. The Global High Voltage Testing Market relies on these methods to provide accurate and reliable results, helping to prevent failures and extend the lifespan of electrical systems.

Submarine Cable, Offshore Cable in the Global High Voltage Testing Market:

The Global High Voltage Testing Market finds significant applications in the areas of submarine and offshore cables. Submarine cables, which are used to transmit electricity across bodies of water, require rigorous testing to ensure their reliability and safety. High voltage testing is essential for these cables as they are subjected to harsh underwater conditions, including high pressure, temperature variations, and potential physical damage. The testing process involves evaluating the insulation and overall integrity of the cables to prevent failures that could lead to costly repairs and downtime. Offshore cables, which are used in offshore wind farms and oil and gas platforms, also require high voltage testing to ensure their performance and safety. These cables are exposed to extreme environmental conditions, including saltwater corrosion, mechanical stress, and temperature fluctuations. High voltage testing helps in identifying potential weaknesses in the insulation and other components, ensuring that the cables can withstand the demanding conditions of offshore environments. The testing process for both submarine and offshore cables involves a combination of methods, including sustained low frequency tests, constant DC tests, high frequency tests, and surge or impulse tests. These tests help in assessing the cables' ability to operate safely and efficiently under various conditions, ensuring the reliability and longevity of the electrical systems they support. The Global High Voltage Testing Market plays a crucial role in the maintenance and upgrading of submarine and offshore cables, helping to prevent failures and ensure the continuous supply of electricity in these critical applications.

Global High Voltage Testing Market Outlook:

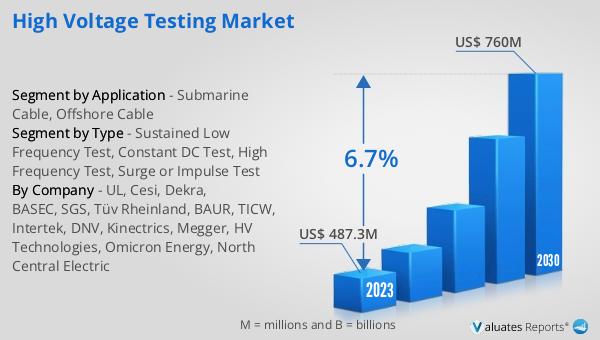

The global High Voltage Testing market was valued at US$ 487.3 million in 2023 and is anticipated to reach US$ 760 million by 2030, witnessing a CAGR of 6.7% during the forecast period 2024-2030. This growth is driven by the increasing demand for electricity, the expansion of power grids, and the need for regular maintenance and upgrading of existing infrastructure. High voltage testing is essential for ensuring the reliability and safety of electrical systems, making it a critical component of the electrical industry. The market includes various players, from equipment manufacturers to service providers, all working together to ensure the safe and efficient operation of high voltage electrical systems. The sustained growth of the market highlights the importance of high voltage testing in maintaining the integrity and performance of electrical systems, ensuring that they meet the required safety and performance standards. The Global High Voltage Testing Market is expected to continue its growth trajectory, driven by the ongoing demand for reliable and efficient electrical systems.

| Report Metric | Details |

| Report Name | High Voltage Testing Market |

| Accounted market size in 2023 | US$ 487.3 million |

| Forecasted market size in 2030 | US$ 760 million |

| CAGR | 6.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | UL, Cesi, Dekra, BASEC, SGS, Tüv Rheinland, BAUR, TICW, Intertek, DNV, Kinectrics, Megger, HV Technologies, Omicron Energy, North Central Electric |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |