What is Global Dry Clutch Friction Plate Market?

The Global Dry Clutch Friction Plate Market refers to the worldwide industry involved in the production, distribution, and sale of dry clutch friction plates. These components are crucial in the automotive sector, particularly in the transmission systems of vehicles. Unlike wet clutches, which are lubricated with oil, dry clutches operate without lubrication, making them more efficient in certain applications. They are designed to engage and disengage the engine from the transmission, allowing for smooth gear shifts and efficient power transfer. The market encompasses various types of vehicles, including passenger cars and commercial vehicles, and caters to both original equipment manufacturers (OEMs) and the aftermarket. The demand for dry clutch friction plates is driven by factors such as the increasing production of vehicles, advancements in transmission technologies, and the need for improved fuel efficiency and performance. Additionally, the market is influenced by regional automotive production trends, regulatory standards, and consumer preferences. As the automotive industry continues to evolve, the Global Dry Clutch Friction Plate Market is expected to grow, driven by innovations in materials and manufacturing processes that enhance the durability and performance of these critical components.

MT, AMT, DSG in the Global Dry Clutch Friction Plate Market:

Manual Transmission (MT), Automated Manual Transmission (AMT), and Direct Shift Gearbox (DSG) are three types of transmission systems that utilize dry clutch friction plates in the Global Dry Clutch Friction Plate Market. Manual Transmission (MT) is the traditional type of transmission where the driver manually shifts gears using a clutch pedal and gear stick. In this system, dry clutch friction plates play a crucial role in engaging and disengaging the engine from the transmission, allowing for smooth gear changes. MTs are known for their simplicity, reliability, and cost-effectiveness, making them popular in various regions, especially in markets where driving enthusiasts prefer the control and engagement of manual shifting. Automated Manual Transmission (AMT) combines the features of manual and automatic transmissions. It uses a computer-controlled system to automate the clutch and gear shift operations, eliminating the need for a clutch pedal. Dry clutch friction plates in AMTs are essential for ensuring precise and efficient gear changes, contributing to improved fuel efficiency and driving comfort. AMTs are particularly favored in commercial vehicles and entry-level passenger cars due to their cost-effectiveness and ease of use. Direct Shift Gearbox (DSG), also known as dual-clutch transmission, is a more advanced system that uses two separate clutches for odd and even gear sets. This design allows for seamless and rapid gear shifts, enhancing the driving experience and performance. Dry clutch friction plates in DSG systems are critical for managing the high torque and power transfer between the engine and transmission. DSGs are commonly found in high-performance and luxury vehicles, where the emphasis is on delivering a sporty and responsive driving experience. Each of these transmission types has its unique advantages and applications, and the choice of transmission often depends on factors such as vehicle type, performance requirements, and consumer preferences. The Global Dry Clutch Friction Plate Market caters to the diverse needs of these transmission systems, providing high-quality components that ensure optimal performance and durability.

Passenger Vehicle, Commercial Vehicle in the Global Dry Clutch Friction Plate Market:

The usage of dry clutch friction plates in passenger vehicles and commercial vehicles highlights the versatility and importance of these components in the automotive industry. In passenger vehicles, dry clutch friction plates are integral to the transmission systems, whether it be in manual transmissions (MT), automated manual transmissions (AMT), or direct shift gearboxes (DSG). For manual transmissions, these plates facilitate smooth gear changes, enhancing the driving experience and providing better control over the vehicle. In automated manual transmissions, they contribute to the automation of gear shifts, offering a balance between the efficiency of manual transmissions and the convenience of automatic transmissions. In direct shift gearboxes, dry clutch friction plates enable rapid and seamless gear changes, which is particularly valued in high-performance and luxury vehicles. The emphasis in passenger vehicles is often on driving comfort, fuel efficiency, and performance, and dry clutch friction plates play a crucial role in achieving these objectives. In commercial vehicles, the requirements for dry clutch friction plates are slightly different due to the nature of their usage. Commercial vehicles, such as trucks and buses, often operate under more demanding conditions, including heavy loads, frequent stop-and-go traffic, and long-distance travel. In these scenarios, the durability and reliability of dry clutch friction plates are paramount. They must withstand higher levels of stress and wear while ensuring efficient power transfer and minimal downtime. Automated manual transmissions are particularly popular in commercial vehicles due to their ability to handle heavy loads and improve fuel efficiency. The use of dry clutch friction plates in these transmissions helps in reducing maintenance costs and enhancing the overall lifespan of the vehicle. Additionally, the growing emphasis on reducing emissions and improving fuel economy in commercial vehicles further drives the demand for advanced dry clutch friction plates that can meet these stringent requirements. Overall, the usage of dry clutch friction plates in both passenger and commercial vehicles underscores their critical role in the automotive industry. These components not only contribute to the performance and efficiency of the vehicles but also play a significant part in meeting regulatory standards and consumer expectations.

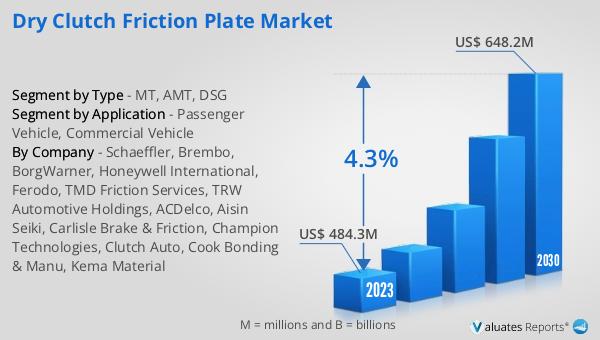

Global Dry Clutch Friction Plate Market Outlook:

The global Dry Clutch Friction Plate market, valued at US$ 484.3 million in 2023, is projected to grow to US$ 648.2 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.3% during the forecast period from 2024 to 2030. This growth trajectory indicates a steady increase in demand for dry clutch friction plates, driven by various factors such as advancements in automotive transmission technologies, increasing vehicle production, and the need for improved fuel efficiency and performance. The market's expansion is also influenced by regional automotive production trends, regulatory standards, and consumer preferences. As the automotive industry continues to evolve, innovations in materials and manufacturing processes are expected to enhance the durability and performance of dry clutch friction plates, further driving market growth. The projected growth underscores the importance of these components in the automotive sector and highlights the ongoing efforts to meet the evolving needs of the industry.

| Report Metric | Details |

| Report Name | Dry Clutch Friction Plate Market |

| Accounted market size in 2023 | US$ 484.3 million |

| Forecasted market size in 2030 | US$ 648.2 million |

| CAGR | 4.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Schaeffler, Brembo, BorgWarner, Honeywell International, Ferodo, TMD Friction Services, TRW Automotive Holdings, ACDelco, Aisin Seiki, Carlisle Brake & Friction, Champion Technologies, Clutch Auto, Cook Bonding & Manu, Kema Material |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |