What is Global Cow Whole Milk Powder Market?

The Global Cow Whole Milk Powder Market refers to the worldwide industry involved in the production, distribution, and sale of powdered milk derived from cow's milk. Whole milk powder is created by evaporating the water content from liquid milk, resulting in a dry, shelf-stable product that retains most of the nutritional benefits of fresh milk. This market encompasses various stages, including dairy farming, milk processing, packaging, and distribution. The demand for cow whole milk powder is driven by its versatility and long shelf life, making it a popular choice in regions with limited access to fresh milk. It is used in a wide range of applications, from infant formula to bakery products, and is a staple in many households and food industries around the world. The market is influenced by factors such as consumer preferences, economic conditions, and advancements in dairy processing technologies.

Formula Milk Powder, Modified Milk Powder in the Global Cow Whole Milk Powder Market:

Formula milk powder and modified milk powder are significant segments within the Global Cow Whole Milk Powder Market. Formula milk powder is specifically designed to meet the nutritional needs of infants and young children who are not breastfed. It is fortified with essential vitamins, minerals, and other nutrients to support healthy growth and development. This type of milk powder is often used as a substitute for breast milk and is available in various formulations to cater to different age groups and dietary requirements. Modified milk powder, on the other hand, refers to milk powder that has been altered to suit specific dietary needs or preferences. This can include lactose-free milk powder for individuals with lactose intolerance, low-fat or skim milk powder for those looking to reduce their fat intake, and fortified milk powder with added nutrients such as calcium or vitamin D. Both formula and modified milk powders are produced through advanced processing techniques that ensure the retention of essential nutrients while removing unwanted components. These products are widely used in households, healthcare settings, and the food industry, providing a convenient and nutritious alternative to fresh milk. The demand for these specialized milk powders is driven by factors such as changing dietary habits, increasing health awareness, and the need for convenient and long-lasting dairy products.

Infant, Child, Aldult, Elderly in the Global Cow Whole Milk Powder Market:

The usage of Global Cow Whole Milk Powder spans across various age groups, including infants, children, adults, and the elderly. For infants, whole milk powder is often used as a base ingredient in infant formula, providing essential nutrients that support growth and development during the early stages of life. It is a crucial alternative for mothers who are unable to breastfeed, ensuring that their babies receive the necessary nutrition. For children, whole milk powder serves as a convenient and nutritious option for daily consumption. It can be easily mixed with water to create a milk beverage that is rich in calcium, protein, and other vital nutrients, supporting healthy bone development and overall growth. Adults also benefit from the consumption of whole milk powder, as it provides a source of high-quality protein and essential vitamins and minerals. It can be used in various culinary applications, such as baking, cooking, and making beverages, offering a versatile and long-lasting dairy option. For the elderly, whole milk powder is particularly valuable as it can help meet their nutritional needs, especially when fresh milk is not readily available. It is easy to store and prepare, making it a practical choice for older individuals who may have limited mobility or access to fresh groceries. Additionally, whole milk powder can be fortified with additional nutrients to address specific health concerns common in older adults, such as osteoporosis or weakened immune systems. Overall, the versatility and nutritional benefits of cow whole milk powder make it a valuable product for individuals of all ages.

Global Cow Whole Milk Powder Market Outlook:

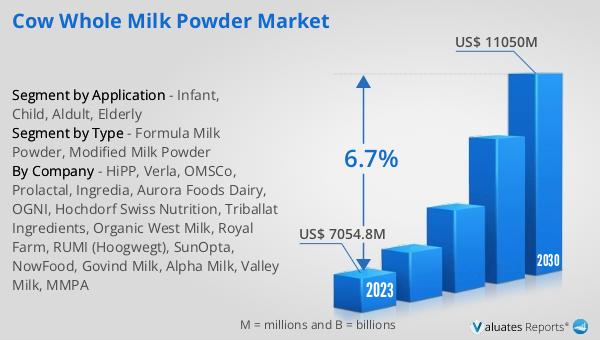

The global Cow Whole Milk Powder market was valued at US$ 7054.8 million in 2023 and is anticipated to reach US$ 11050 million by 2030, witnessing a CAGR of 6.7% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of the cow whole milk powder industry over the coming years. The increasing demand for convenient and long-lasting dairy products, coupled with the rising awareness of the nutritional benefits of whole milk powder, is expected to drive market expansion. The projected growth rate indicates a robust market trajectory, with substantial opportunities for manufacturers, distributors, and other stakeholders in the dairy industry. As consumer preferences continue to evolve and new markets emerge, the cow whole milk powder market is poised for sustained growth and development. This positive outlook underscores the importance of innovation and adaptation in meeting the diverse needs of consumers worldwide.

| Report Metric | Details |

| Report Name | Cow Whole Milk Powder Market |

| Accounted market size in 2023 | US$ 7054.8 million |

| Forecasted market size in 2030 | US$ 11050 million |

| CAGR | 6.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | HiPP, Verla, OMSCo, Prolactal, Ingredia, Aurora Foods Dairy, OGNI, Hochdorf Swiss Nutrition, Triballat Ingredients, Organic West Milk, Royal Farm, RUMI (Hoogwegt), SunOpta, NowFood, Govind Milk, Alpha Milk, Valley Milk, MMPA |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |