What is Global LED Lighting Driver ICs Market?

The Global LED Lighting Driver ICs Market is an intriguing sector that focuses on the components essential for powering LED lights. These integrated circuits (ICs) are designed to provide a constant power supply to LED lighting systems, ensuring optimal performance and longevity. The market encompasses a wide range of driver ICs tailored to meet the diverse needs of LED lighting applications across the globe. With the increasing adoption of LED lighting due to its energy efficiency, long life, and decreasing costs, the demand for reliable and efficient LED lighting driver ICs has surged. This market is a critical component of the broader semiconductor industry, playing a pivotal role in the advancement of energy-efficient lighting solutions. As industries and consumers alike seek more sustainable and cost-effective lighting options, the Global LED Lighting Driver ICs Market is poised for significant growth, reflecting the broader trend towards energy conservation and environmental sustainability.

SMD Type, Through Hole Type in the Global LED Lighting Driver ICs Market:

Diving into the Global LED Lighting Driver ICs Market, we find two primary types of ICs based on their mounting technology: SMD (Surface Mount Device) Type and Through Hole Type. SMD Type ICs are designed for direct mounting on the surface of printed circuit boards (PCBs), offering a compact footprint and enhanced performance in a smaller package. This type is favored for its space-saving design, making it ideal for sleek, modern LED lighting applications where space is at a premium. On the other hand, Through Hole Type ICs are mounted through holes drilled into PCBs. This traditional mounting style is known for its strong mechanical bonds and excellent heat dissipation properties, making it suitable for high-power LED applications where reliability under thermal stress is crucial. Both types play vital roles in the Global LED Lighting Driver ICs Market, catering to a wide array of lighting needs. From indoor and outdoor lighting solutions to automotive and industrial applications, these ICs ensure that LED lights operate efficiently, safely, and reliably. As technology advances, the market continues to evolve, with manufacturers constantly innovating to improve the performance, efficiency, and versatility of their LED driver IC offerings, ensuring they meet the growing demands of the global market.

Automotive Lighting, General Lighting in the Global LED Lighting Driver ICs Market:

In the realm of the Global LED Lighting Driver ICs Market, two areas where these components find critical application are Automotive Lighting and General Lighting. In Automotive Lighting, LED driver ICs are essential for ensuring the reliability and performance of LED lights used in vehicles. These ICs help manage the power supplied to LED headlights, taillights, and interior lights, contributing to safer driving conditions and enhancing the vehicle's aesthetic appeal. The precise control offered by these ICs allows for innovative lighting solutions, such as adaptive lighting systems that adjust based on driving conditions, thereby improving visibility and safety. In the General Lighting sector, LED driver ICs play a pivotal role in residential, commercial, and industrial lighting. They enable the development of energy-efficient, durable, and versatile lighting solutions that can be tailored to the specific needs of various environments. From smart home lighting systems that adjust brightness and color based on user preferences to large-scale industrial lighting setups designed for energy efficiency and longevity, LED driver ICs are at the heart of modern lighting solutions. Their ability to provide stable and efficient power to LED lights makes them indispensable in our quest for more sustainable and adaptable lighting technologies.

Global LED Lighting Driver ICs Market Outlook:

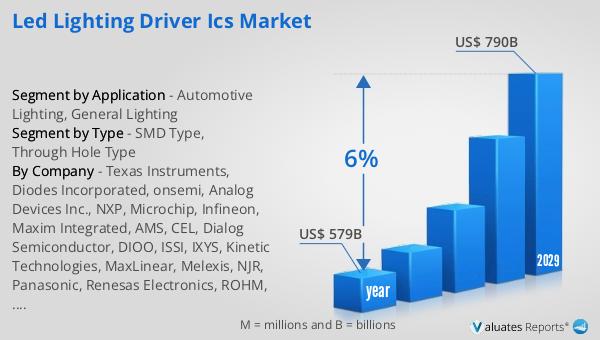

The market outlook for the semiconductor industry, which includes the Global LED Lighting Driver ICs Market, presents a promising future. In 2022, the industry was valued at approximately 579 billion US dollars. This figure is expected to climb to around 790 billion US dollars by the year 2029. This growth trajectory suggests a Compound Annual Growth Rate (CAGR) of about 6% throughout the forecast period. Such an expansion reflects the increasing reliance on semiconductor technology across various sectors, including consumer electronics, automotive, and industrial applications. The surge in demand for energy-efficient lighting solutions, alongside the broader adoption of LED lighting, plays a significant role in this growth. As the world continues to prioritize sustainability and energy conservation, the semiconductor industry, particularly the segment focused on LED lighting driver ICs, is set to experience robust growth. This outlook underscores the industry's critical role in powering the next generation of technological advancements and sustainable solutions.

| Report Metric | Details |

| Report Name | LED Lighting Driver ICs Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Texas Instruments, Diodes Incorporated, onsemi, Analog Devices Inc., NXP, Microchip, Infineon, Maxim Integrated, AMS, CEL, Dialog Semiconductor, DIOO, ISSI, IXYS, Kinetic Technologies, MaxLinear, Melexis, NJR, Panasonic, Renesas Electronics, ROHM, STM, Toshiba, Wurth Elektronik |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |