What is Global Wafer Handling Electrostatic Chuck Market?

The Global Wafer Handling Electrostatic Chuck Market is an intricate segment of the semiconductor equipment industry, focusing on devices essential for the secure handling of silicon wafers during the manufacturing process. These electrostatic chucks (ESCs) utilize electrical charges to hold wafers in place, ensuring precision and stability without physical contact that could damage the delicate surfaces. As the semiconductor industry pushes for smaller, more efficient chips, the demand for sophisticated wafer handling solutions has surged. The market for these electrostatic chucks is driven by the need for higher throughput and reduced contamination in chip fabrication facilities. With advancements in technology, these chucks have become critical in the production of integrated circuits, contributing significantly to the overall efficiency and yield of semiconductor manufacturing operations. As of 2023, the market has seen substantial growth, reflecting the ongoing expansion and technological evolution within the global semiconductor industry.

Coulomb Type Electrostatic Chuck, Johnsen-Rahbek (JR) Type Electrostatic Chuck in the Global Wafer Handling Electrostatic Chuck Market:

Diving into the specifics, the Global Wafer Handling Electrostatic Chuck Market is segmented into two primary types: Coulomb Type Electrostatic Chuck and Johnsen-Rahbek (JR) Type Electrostatic Chuck. The Coulomb Type relies on the principle of electrostatic force for wafer clamping, offering a straightforward mechanism that ensures minimal wafer deformation, making it suitable for thin wafer handling. This type is favored for its simplicity and effectiveness in various semiconductor processes. On the other hand, the Johnsen-Rahbek (JR) Type Electrostatic Chuck operates on a different principle, leveraging the electrostatic force and real area of contact to enhance its holding power. This type is particularly valued for its strong clamping force, which is crucial for high-precision applications. Both types play pivotal roles in the semiconductor manufacturing process, catering to different requirements based on the nature of the semiconductor wafers and the specific processes involved. Manufacturers and researchers continuously explore improvements in these technologies to address the evolving needs of the semiconductor industry, aiming for higher efficiency, reduced contamination, and better overall performance in wafer handling.

300 mm Wafer, 200 mm Wafer, Others in the Global Wafer Handling Electrostatic Chuck Market:

The application of the Global Wafer Handling Electrostatic Chuck Market spans across various wafer sizes, notably including 300 mm wafers, 200 mm wafers, and others. The 300 mm wafer segment represents a significant portion of the market, driven by its widespread adoption in advanced semiconductor manufacturing due to its efficiency and higher output compared to smaller diameters. Electrostatic chucks designed for 300 mm wafers are engineered to meet the stringent requirements of modern chip fabrication, including high precision and minimal contamination. Similarly, the 200 mm wafer segment remains relevant, particularly for specialized or legacy semiconductor processes where upgrading to larger wafers is not feasible or cost-effective. Electrostatic chucks for 200 mm wafers continue to see demand, reflecting the ongoing need for equipment that can support a wide range of semiconductor manufacturing technologies. The "others" category encompasses electrostatic chucks for wafers of different sizes, catering to niche applications or emerging technologies within the semiconductor industry. This diversity in application underscores the versatility and critical nature of electrostatic chucks in enabling the production of a broad spectrum of semiconductor devices.

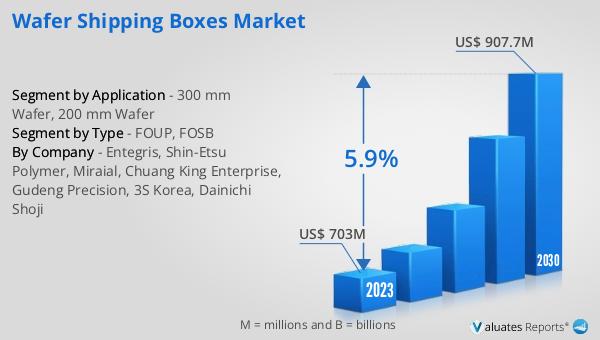

Global Wafer Handling Electrostatic Chuck Market Outlook:

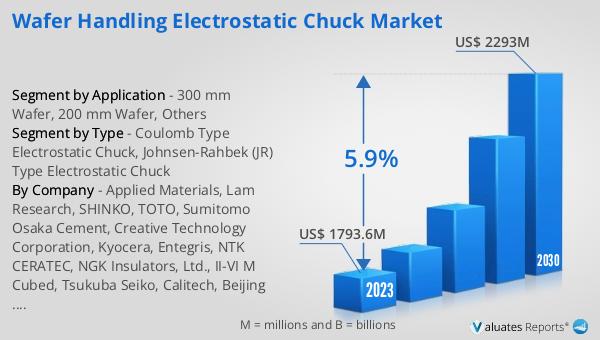

In 2023, the Global Wafer Handling Electrostatic Chuck Market was valued at approximately $1793.6 million, showcasing a robust foundation within the semiconductor equipment sector. This market is on a trajectory to expand to around $2293 million by the year 2030, marking a compound annual growth rate (CAGR) of 5.9% throughout the forecast period spanning from 2024 to 2030. Leading the market in terms of revenue share, Applied Materials has established a dominant presence with 43.84%, followed closely by Lam Research and SHINKO, holding 31.58% and 10.21% of the market share, respectively. This financial outlook highlights the competitive landscape of the Global Wafer Handling Electrostatic Chuck Market, reflecting the strategic positioning and innovative advancements made by key players. The anticipated growth underscores the increasing demand for semiconductor devices and the critical role of efficient wafer handling technologies in meeting this demand.

| Report Metric | Details |

| Report Name | Wafer Handling Electrostatic Chuck Market |

| Accounted market size in 2023 | US$ 1793.6 million |

| Forecasted market size in 2030 | US$ 2293 million |

| CAGR | 5.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Applied Materials, Lam Research, SHINKO, TOTO, Sumitomo Osaka Cement, Creative Technology Corporation, Kyocera, Entegris, NTK CERATEC, NGK Insulators, Ltd., II-VI M Cubed, Tsukuba Seiko, Calitech, Beijing U-PRECISION TECH CO., LTD. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |