What is Global Anterior Cervical Plating Systems Market?

The Global Anterior Cervical Plating Systems Market is a specialized segment within the medical device industry, focusing on the development, manufacturing, and distribution of anterior cervical plates. These plates are crucial components used in surgeries to fixate and stabilize the cervical spine, which is the upper part of the spine located in the neck. This market has garnered significant attention due to the increasing prevalence of cervical spine disorders and injuries, which are often caused by accidents, degenerative diseases, or congenital conditions. The anterior cervical plating systems are designed to provide mechanical stability and facilitate the fusion of the vertebrae during the healing process. Surgeons utilize these systems in procedures aimed at relieving pain, restoring function, and improving the quality of life for patients suffering from conditions such as herniated discs, spinal stenosis, and fractures. The market's value is underpinned by technological advancements, the growing aging population, and the rising demand for minimally invasive surgical procedures, which collectively drive the development of more efficient, safer, and patient-friendly solutions.

Pure Titanium, Titanium Alloy in the Global Anterior Cervical Plating Systems Market:

In the realm of the Global Anterior Cervical Plating Systems Market, materials like Pure Titanium and Titanium Alloy stand out for their critical roles. These materials are favored for their exceptional strength, biocompatibility, and corrosion resistance, making them ideal for use in medical implants and devices. Pure Titanium is widely appreciated in the medical field for its ability to integrate well with human bone, a property known as osseointegration. This characteristic is particularly important for anterior cervical plating systems, as it ensures the stability of the implant while the spinal vertebrae heal and fuse together. On the other hand, Titanium Alloy, which combines titanium with other metals like aluminum and vanadium, offers enhanced strength and reduced weight compared to pure titanium. This makes titanium alloy plates more suitable for patients requiring more robust support due to the nature of their spinal conditions or their physical activity levels. The choice between pure titanium and titanium alloy in the manufacturing of anterior cervical plating systems is influenced by factors such as the specific clinical requirements of the surgery, the patient's condition, and the surgeon's preference. Manufacturers in the Global Anterior Cervical Plating Systems Market invest heavily in research and development to innovate and improve the properties of these materials, aiming to enhance the performance and outcomes of spinal surgeries. The ongoing advancements in material science and surgical techniques continue to expand the possibilities for treating complex cervical spine issues, thereby contributing to the growth and evolution of this market.

Hospital, Specialty Clinic, Others in the Global Anterior Cervical Plating Systems Market:

The usage of Global Anterior Cervical Plating Systems in various healthcare settings, including Hospitals, Specialty Clinics, and Others, is a testament to their versatility and critical role in spinal surgery. In hospitals, these systems are commonly used in the orthopedic or neurosurgery departments, where surgeries involving the cervical spine are performed. The availability of advanced surgical facilities and multidisciplinary teams in hospitals ensures that patients undergoing cervical spine surgery receive comprehensive care, from pre-operative assessment to post-operative rehabilitation. Specialty clinics, on the other hand, offer a more focused setting for the treatment of spinal conditions. These clinics often have surgeons who specialize in spinal surgeries, including those involving anterior cervical plating systems. The specialized nature of these clinics allows for a high degree of expertise and personalized care, which can be particularly beneficial for patients with complex or uncommon spinal issues. Other healthcare settings, such as outpatient surgical centers, may also utilize anterior cervical plating systems for less invasive procedures. These centers can offer the advantage of reduced costs and shorter recovery times, making them an attractive option for patients and healthcare providers alike. The use of anterior cervical plating systems across these diverse healthcare settings underscores their importance in the treatment of cervical spine conditions and highlights the need for ongoing innovation and education in their application to ensure optimal patient outcomes.

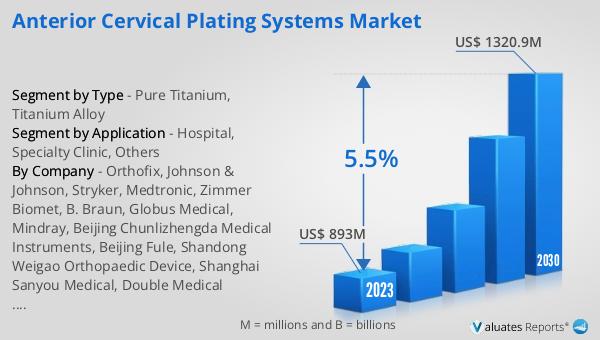

Global Anterior Cervical Plating Systems Market Outlook:

The market outlook for the Global Anterior Cervical Plating Systems presents a promising future, with its valuation at US$ 893 million in 2023, and an expected growth to reach US$ 1320.9 million by 2030. This growth trajectory, marked by a Compound Annual Growth Rate (CAGR) of 5.5% during the forecast period from 2024 to 2030, underscores the increasing demand and reliance on these systems in the medical field. This anticipated expansion is reflective of the broader trends in healthcare, including technological advancements in medical devices, an aging global population that is more prone to cervical spine issues, and a growing preference for minimally invasive surgical procedures. The market's growth is also indicative of the increasing awareness and improvements in the diagnosis and treatment of spinal conditions, which in turn drives the demand for anterior cervical plating systems. As these systems evolve to become more effective and patient-friendly, their adoption in surgical practices worldwide is expected to rise, further propelling the market's growth. This outlook not only highlights the market's current state but also its potential to significantly impact the healthcare industry by providing essential solutions for patients requiring cervical spine surgeries.

| Report Metric | Details |

| Report Name | Anterior Cervical Plating Systems Market |

| Accounted market size in 2023 | US$ 893 million |

| Forecasted market size in 2030 | US$ 1320.9 million |

| CAGR | 5.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Orthofix, Johnson & Johnson, Stryker, Medtronic, Zimmer Biomet, B. Braun, Globus Medical, Mindray, Beijing Chunlizhengda Medical Instruments, Beijing Fule, Shandong Weigao Orthopaedic Device, Shanghai Sanyou Medical, Double Medical Technology, Genesys Spine, Nvision Biomedical Technologies, Zhejiang Canwell Medical, BRICON, Changzhou Waston Medical Appliance, Suzhou AND Science&Technology, Jiangsu Hope Medical Instrument, Shandong Shinva United |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |