What is Global Smart Building Solutions Market?

The Global Smart Building Solutions Market encompasses a wide array of technologies aimed at making buildings more intelligent, efficient, and user-friendly. At its core, this market focuses on integrating various systems and processes to manage buildings effectively, ensuring comfort, safety, and energy efficiency. Smart building solutions leverage advanced technologies such as IoT (Internet of Things), AI (Artificial Intelligence), and big data analytics to monitor and control different aspects of a building's operation. From energy consumption to security systems, these solutions provide a centralized platform for managing all the building's functionalities. This approach not only enhances the occupants' experience by creating a more comfortable and safe environment but also contributes significantly to energy conservation and operational cost reduction. As the global emphasis on sustainability and smart cities intensifies, the demand for smart building solutions is expected to surge, making it a key player in the future of urban development.

Building Management System (BMS), HVAC, Lighting Control, Security and Access Control, Emergency Alarm and Evacuation System, Audio and Visual Effects, Escalator, Elevator, Others in the Global Smart Building Solutions Market:

The Global Smart Building Solutions Market is a comprehensive ecosystem encompassing various subsystems like Building Management Systems (BMS), HVAC (Heating, Ventilation, and Air Conditioning), Lighting Control, Security and Access Control, Emergency Alarm and Evacuation Systems, Audio and Visual Effects, and vertical transportation solutions including Escalators and Elevators. BMS forms the backbone of smart buildings, providing a unified platform for monitoring and controlling the building's mechanical and electrical equipment. HVAC systems, optimized through smart solutions, ensure energy efficiency and occupant comfort by dynamically adjusting to the internal and external environmental conditions. Lighting control systems further enhance energy savings and comfort by automatically adjusting the lighting based on occupancy and natural light levels. Security and access control systems leverage advanced technologies like biometrics and mobile access to ensure building security, while emergency alarm and evacuation systems are designed to efficiently manage crises, ensuring occupant safety. Audio and visual systems enhance the functionality of meeting spaces and communal areas, adding to the building's smart features. Lastly, smart solutions for escalators and elevators improve safety, efficiency, and maintenance processes, contributing to the overall performance of smart buildings. These components work in synergy to create an intelligent ecosystem that optimizes building operations, enhances occupant comfort, and minimizes environmental impact.

Commercial Building, Government Building, Hotel, Residential Houses, Others in the Global Smart Building Solutions Market:

In the realm of the Global Smart Building Solutions Market, these technologies find extensive application across various types of buildings, including Commercial Buildings, Government Buildings, Hotels, Residential Houses, and others. In commercial buildings, smart solutions streamline operations, enhance security, and improve energy efficiency, leading to cost savings and a better working environment. Government buildings leverage these technologies to ensure public safety, reduce energy consumption, and enhance service delivery to citizens. Hotels use smart building solutions to provide guests with a personalized experience, optimizing comfort and convenience while ensuring efficient management of resources. In residential houses, these solutions offer homeowners control over their environment, security, and energy usage, contributing to a comfortable, safe, and efficient living space. Other applications include educational institutions, healthcare facilities, and retail spaces, where the benefits of smart building solutions—ranging from enhanced security to improved energy efficiency and operational effectiveness—demonstrate their versatility and impact across different sectors. This widespread usage underscores the transformative potential of smart building technologies in shaping the future of built environments.

Global Smart Building Solutions Market Outlook:

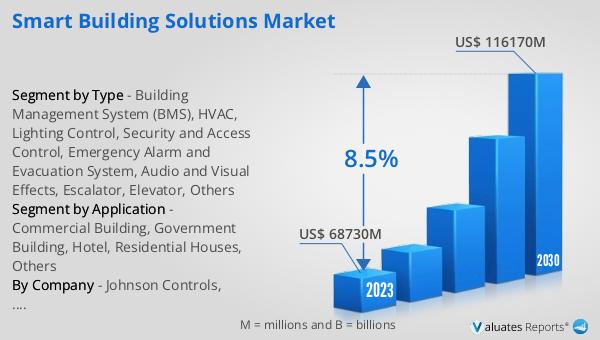

The market outlook for the Global Smart Building Solutions Market reveals a promising trajectory, with the market's value estimated at US$ 68,730 million in 2023, and projections suggesting it will ascend to US$ 116,170 million by 2030. This growth reflects a Compound Annual Growth Rate (CAGR) of 8.5% throughout the forecast period spanning from 2024 to 2030. Such an optimistic forecast underscores the increasing recognition of the value that smart building solutions bring to the table in terms of operational efficiency, energy savings, and enhanced occupant experience. As urbanization continues to rise and the focus on sustainability becomes sharper, the demand for intelligent, efficient, and safer buildings is expected to drive significant growth in this market. This outlook not only highlights the economic potential of the smart building solutions market but also points to the broader implications for urban development, environmental sustainability, and quality of life improvements in the years to come.

| Report Metric | Details |

| Report Name | Smart Building Solutions Market |

| Accounted market size in 2023 | US$ 68730 million |

| Forecasted market size in 2030 | US$ 116170 million |

| CAGR | 8.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Johnson Controls, Honeywell, Schneider, UTC, Siemens, Ingersoll Rand (Trane), Azbil, ABB, Emerson, Eaton, Control4, Bosch, Panasonic, Delta Controls, Legrand, Cisco, IBM, Advantech, Current (GE), Carrier, Otis, Hitachi |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |