What is Global Functional Coil Coatings Market?

The Global Functional Coil Coatings Market is a specialized sector within the coatings industry, focusing on the production and application of coatings used on metal coils. These coatings are applied in a continuous process before the metal is cut and shaped, enhancing the durability, aesthetics, and functionality of the end product. This market caters to a wide range of applications, from construction materials, automotive components, to home appliances, offering solutions that are resistant to corrosion, weather, and wear. The functional aspect of these coatings is paramount, providing not just aesthetic value but also protective qualities that extend the life of metal products. As industries worldwide continue to demand higher quality and more environmentally friendly options, the Global Functional Coil Coatings Market is poised to meet these needs with innovative and sustainable coating solutions. This market's significance is underscored by its contribution to enhancing product value and performance across various sectors, making it a critical component of the global manufacturing landscape.

Primer, Back Paint, Topcoat in the Global Functional Coil Coatings Market:

Diving into the specifics of the Global Functional Coil Coatings Market, we find that it is intricately segmented into Primer, Back Paint, and Topcoat categories, each serving a unique purpose in the coating process. Primers are the foundational layer, designed to adhere to the metal surface and provide a base for subsequent layers, ensuring long-term durability and corrosion resistance. Back Paint, on the other hand, is applied to the reverse side of the coil, offering additional protection against environmental elements and enhancing the overall aesthetic of the metal product. Topcoats are the final layer, applied for their aesthetic qualities and to provide a surface that is resistant to chipping, scratching, and UV damage. These three components work in tandem to ensure that the metal coil is well-protected, both functionally and visually. The Global Functional Coil Coatings Market thrives on innovation, constantly developing new formulations and technologies to improve the performance and environmental footprint of these coatings. As industries evolve and demand more from their materials, the market responds with solutions that are more durable, more aesthetically pleasing, and easier to apply. This relentless pursuit of excellence is what drives the market forward, ensuring that it remains at the forefront of the coatings industry.

Resident Building, Industrial Building in the Global Functional Coil Coatings Market:

In the realm of construction and industrial applications, the Global Functional Coil Coatings Market plays a pivotal role, particularly in the sectors of residential and industrial buildings. These coatings are applied to metal components used in construction, such as roofing, wall panels, and structural supports, providing them with enhanced durability, weather resistance, and aesthetic appeal. In residential buildings, the demand for functional coil coatings is driven by the desire for homes that are not only visually appealing but also capable of withstanding the rigors of weather and time. Similarly, in industrial buildings, where durability and maintenance are key concerns, these coatings offer solutions that protect against corrosion, chemical exposure, and mechanical wear. The versatility of functional coil coatings makes them suitable for a wide range of architectural styles and industrial applications, ensuring that buildings not only look good but are also built to last. As the construction industry continues to evolve, with a growing emphasis on sustainability and efficiency, the Global Functional Coil Coatings Market is expected to play an increasingly important role, offering coatings that meet the industry's changing needs while adhering to stringent environmental standards.

Global Functional Coil Coatings Market Outlook:

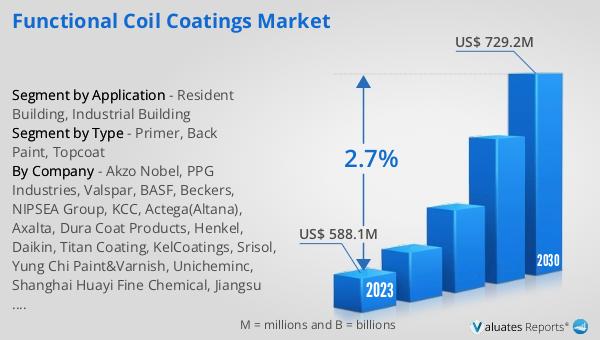

The market outlook for the Global Functional Coil Coatings Market presents a promising future, with its value estimated at US$ 588.1 million in 2023, and projections suggesting it will ascend to US$ 729.2 million by 2030. This growth trajectory, marked by a Compound Annual Growth Rate (CAGR) of 2.7% during the forecast period from 2024 to 2030, underscores the market's robust potential. This anticipated expansion is reflective of the increasing demand for coil coatings across various industries, driven by the need for materials that offer enhanced protection and longevity for metal products. The market's growth is also indicative of the ongoing innovations within the sector, aimed at producing more environmentally friendly and efficient coating solutions. As the market continues to evolve, it is expected to offer new opportunities for businesses and investors alike, who are looking to capitalize on the growing demand for high-quality, durable, and sustainable coating options. This optimistic outlook is a testament to the market's resilience and its critical role in meeting the contemporary needs of the global manufacturing landscape.

| Report Metric | Details |

| Report Name | Functional Coil Coatings Market |

| Accounted market size in 2023 | US$ 588.1 million |

| Forecasted market size in 2030 | US$ 729.2 million |

| CAGR | 2.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Akzo Nobel, PPG Industries, Valspar, BASF, Beckers, NIPSEA Group, KCC, Actega(Altana), Axalta, Dura Coat Products, Henkel, Daikin, Titan Coating, KelCoatings, Srisol, Yung Chi Paint&Varnish, Unicheminc, Shanghai Huayi Fine Chemical, Jiangsu Lanling Group, Shaanxi Baotashan Paint, Pingyuan Wente, Tangshan Wick Painting Chemical, CNOOC Changzhou EP Coating, Ningbo Zhengliang Coatings, Zhejiang Tiannv Group, Changzhou Baoxin Anticorrosive Material |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |