What is Global Pharmaceutical Grade Cation Exchange Resins Market?

The Global Pharmaceutical Grade Cation Exchange Resins Market is a specialized segment within the broader pharmaceutical industry, focusing on the production and application of cation exchange resins of a quality suitable for pharmaceutical use. These resins are polymers that can exchange cations (positively charged ions) with other ions in a solution passing through them. This ability makes them invaluable in various pharmaceutical applications, including drug formulation and purification processes. The market for these high-grade resins is driven by the increasing demand for more sophisticated drug delivery mechanisms and the ongoing quest for purity and efficiency in drug production. As pharmaceutical companies continue to seek out more effective and safer drug delivery systems, the importance of these resins, known for their high specificity and selectivity, grows. This market segment is characterized by its focus on quality, regulatory compliance, and innovation in response to the evolving needs of the pharmaceutical industry.

Strong Acidc, Weakly Acidic in the Global Pharmaceutical Grade Cation Exchange Resins Market:

Diving into the Global Pharmaceutical Grade Cation Exchange Resins Market, it's essential to understand the distinctions between Strong Acidic and Weakly Acidic cation exchange resins and their significance. Strong Acidic cation exchange resins, typically sulfonated polystyrene divinylbenzene, are known for their robustness and high capacity for ion exchange, making them ideal for applications requiring efficient ion removal or exchange. These resins are particularly effective in environments with low pH levels, where their strong acidic nature allows them to perform optimally. On the other hand, Weakly Acidic cation exchange resins, often made from acrylic or methacrylic acid, offer a more gentle ion exchange capacity. These resins are better suited for scenarios where a softer approach is needed, such as in the removal of divalent cations (like calcium and magnesium) from solutions without drastically altering the pH. The choice between strong and weakly acidic resins depends on the specific requirements of the pharmaceutical application, including the desired outcome, the nature of the substances being treated, and the environmental conditions. The Global Pharmaceutical Grade Cation Exchange Resins Market caters to this diverse need by providing a range of products tailored to various applications, from drug purification to the preparation of pharmaceutical ingredients. The market's depth and breadth ensure that pharmaceutical manufacturers can find the precise resin type to meet their stringent quality and performance standards.

Controlled Drug Release, Odor Masking, Others in the Global Pharmaceutical Grade Cation Exchange Resins Market:

In the realm of the Global Pharmaceutical Grade Cation Exchange Resins Market, these resins find their application in several critical areas, notably in Controlled Drug Release, Odor Masking, and other diverse pharmaceutical processes. Controlled Drug Release is a pivotal application where these resins are employed to modulate the release rate of drugs into the body, ensuring a steady therapeutic effect over an extended period. This is particularly beneficial for medications that require consistent blood concentration levels to be effective, reducing the frequency of dosage and improving patient compliance. Odor Masking is another significant application, where the unique properties of cation exchange resins are utilized to bind or neutralize odorous compounds in pharmaceutical products, making them more palatable and acceptable to patients. Beyond these, the resins are also used in a variety of other applications, including but not limited to, the purification of active pharmaceutical ingredients (APIs), removal of impurities that can affect drug safety and efficacy, and the stabilization of pharmaceutical formulations. These applications underscore the versatility and indispensability of pharmaceutical grade cation exchange resins in the development and manufacturing of modern pharmaceuticals, highlighting their role in enhancing drug performance and patient experience.

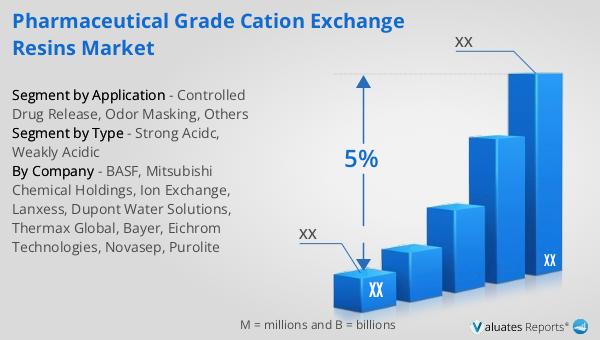

Global Pharmaceutical Grade Cation Exchange Resins Market Outlook:

The outlook for the Global Pharmaceutical Grade Cation Exchange Resins Market is set against the backdrop of the broader pharmaceutical industry, which is projected to reach a valuation of 1475 billion USD by 2022, growing at a compound annual growth rate (CAGR) of 5% over the next six years. This growth trajectory is reflective of the increasing demand for pharmaceutical products and the continuous innovation within the industry. In parallel, the chemical drug market, a subset of the larger pharmaceutical market, is anticipated to expand from 1005 billion USD in 2018 to 1094 billion USD by 2022. This growth is indicative of the ongoing developments in drug formulation and manufacturing processes, including the utilization of advanced materials like pharmaceutical grade cation exchange resins. These resins play a crucial role in enhancing drug purity, efficacy, and safety, thereby supporting the growth and evolution of the pharmaceutical industry. As the market for pharmaceuticals continues to expand, the demand for high-quality cation exchange resins is expected to rise, reflecting their critical role in the production of effective and reliable pharmaceutical products.

| Report Metric | Details |

| Report Name | Pharmaceutical Grade Cation Exchange Resins Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | BASF, Mitsubishi Chemical Holdings, Ion Exchange, Lanxess, Dupont Water Solutions, Thermax Global, Bayer, Eichrom Technologies, Novasep, Purolite |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |