What is Global Eptacog Alfa (Recombinant Human Coagulation Factor VIIa) Market?

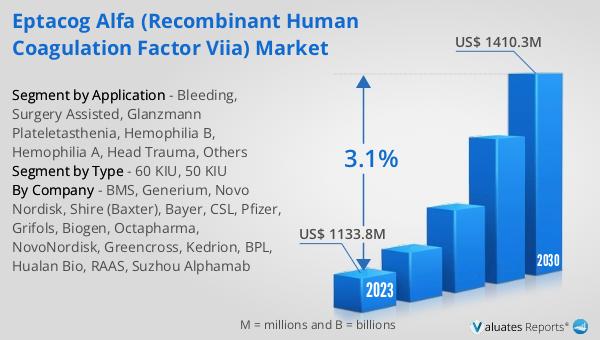

The Global Eptacog Alfa (Recombinant Human Coagulation Factor VIIa) Market is a specialized sector within the pharmaceutical industry that focuses on the production and distribution of Eptacog Alfa, a recombinant form of human coagulation factor VIIa. This product is primarily used in the treatment of bleeding disorders such as hemophilia. The market is characterized by its high value, with a valuation of US$ 1133.8 million in 2022. It is projected to grow at a steady pace, reaching an estimated value of US$ 1410.3 million by 2029. This represents a compound annual growth rate (CAGR) of 3.1% during the forecast period from 2023 to 2029. The market is dominated by Novo Nordisk, a global healthcare company with more than 95 years of innovation and leadership in diabetes care. This heritage has given them experience and capabilities that also enable them to help people defeat other serious chronic conditions: hemophilia, growth disorders, and obesity. With a market share of over 95%, Novo Nordisk is the leading manufacturer in the Global Eptacog Alfa (Recombinant Human Coagulation Factor VIIa) Market. Geographically, North America is the most significant consumer market for recombinant human coagulation VIIa, accounting for approximately 45% of the global market share. This can be attributed to the advanced healthcare infrastructure in the region, the high prevalence of bleeding disorders, and the presence of key market players. However, other regions are also expected to contribute to the market growth during the forecast period, driven by increasing awareness about bleeding disorders and the availability of effective treatment options.

60 KIU, 50 KIU in the Global Eptacog Alfa (Recombinant Human Coagulation Factor VIIa) Market:

The Global Eptacog Alfa (Recombinant Human Coagulation Factor VIIa) Market is segmented based on the dosage of the product, with 60 KIU and 50 KIU being the most common. These dosages are determined based on the severity of the bleeding disorder and the patient's overall health condition. The choice of dosage is critical as it directly impacts the effectiveness of the treatment and the patient's quality of life. The market is also segmented based on the application of the product. Eptacog Alfa is used in various areas such as controlling bleeding during surgeries, treating Glanzmann Plateletasthenia, Hemophilia B, Hemophilia A, and managing head trauma among others. Each of these applications has a different demand pattern and growth potential, contributing to the overall market dynamics. In the surgical setting, Eptacog Alfa is used to control bleeding during and after the procedure. This is particularly important in surgeries involving patients with bleeding disorders, where the risk of excessive bleeding is high. The product is also used in the treatment of Glanzmann Plateletasthenia, a rare bleeding disorder characterized by the lack of a certain type of protein required for blood clotting. In the case of Hemophilia A and B, Eptacog Alfa is used as a replacement therapy to compensate for the lack of clotting factors in the patient's blood. This helps in controlling bleeding episodes and preventing long-term complications associated with these disorders. Eptacog Alfa is also used in the management of head trauma, where it helps in controlling bleeding within the brain and reducing the risk of further damage. Other applications of the product include the treatment of other bleeding disorders and conditions where the normal clotting mechanism is impaired.

Bleeding, Surgery Assisted, Glanzmann Plateletasthenia, Hemophilia B, Hemophilia A, Head Trauma, Others in the Global Eptacog Alfa (Recombinant Human Coagulation Factor VIIa) Market:

In conclusion, the Global Eptacog Alfa (Recombinant Human Coagulation Factor VIIa) Market is a dynamic and growing sector within the pharmaceutical industry. It is characterized by its high value, the dominance of key players like Novo Nordisk, and the wide range of applications of the product. The market is expected to grow at a steady pace during the forecast period, driven by the increasing prevalence of bleeding disorders and the availability of effective treatment options.

| Report Metric | Details |

| Report Name | Eptacog Alfa (Recombinant Human Coagulation Factor VIIa) Market |

| Accounted market size in 2022 | US$ 1133.8 million |

| Forecasted market size in 2029 | US$ 1410.3 million |

| CAGR | 3.1% |

| Base Year | 2022 |

| Forecasted years | 2023 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | BMS, Generium, Novo Nordisk, Shire (Baxter), Bayer, CSL, Pfizer, Grifols, Biogen, Octapharma, NovoNordisk, Greencross, Kedrion, BPL, Hualan Bio, RAAS, Suzhou Alphamab |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |