What is Global Precision Components for Semiconductors Market?

The Global Precision Components for Semiconductors Market is a critical segment within the broader semiconductor industry, focusing on the production and supply of highly accurate and reliable components essential for semiconductor manufacturing. These precision components are integral to the fabrication of semiconductor devices, which are the building blocks of modern electronics. The market encompasses a wide range of products, including ceramic and metal components, each designed to meet the stringent requirements of semiconductor manufacturing processes. As the demand for advanced electronic devices continues to grow, driven by innovations in technology and increasing consumer electronics usage, the need for precision components has also surged. This market is characterized by rapid technological advancements, with manufacturers constantly innovating to enhance the performance and efficiency of their components. The global reach of this market is significant, with key players operating across various regions to cater to the diverse needs of semiconductor manufacturers. The precision components market is poised for growth, driven by the increasing complexity of semiconductor devices and the need for high-quality components that can support advanced manufacturing techniques. As such, it plays a pivotal role in the overall semiconductor supply chain, ensuring the production of reliable and efficient electronic devices.

Semiconductor Ceramic Components, Semiconductor Metal Components in the Global Precision Components for Semiconductors Market:

Semiconductor ceramic components and semiconductor metal components are two fundamental categories within the Global Precision Components for Semiconductors Market. Ceramic components are known for their excellent thermal and electrical insulation properties, making them ideal for use in high-temperature and high-voltage applications. These components are often used in environments where stability and reliability are paramount, such as in the production of power semiconductors and high-frequency devices. The inherent properties of ceramics, such as their resistance to wear and corrosion, make them suitable for use in harsh manufacturing environments. Additionally, ceramic components are often used in applications where precision and accuracy are critical, as they can be manufactured to very tight tolerances. On the other hand, semiconductor metal components are essential for their conductive properties, which are crucial for the efficient transmission of electrical signals within semiconductor devices. Metals such as copper, aluminum, and gold are commonly used in the production of these components due to their excellent conductivity and ability to form reliable electrical connections. Metal components are often used in the fabrication of interconnects, which are the pathways that connect different parts of a semiconductor device. The choice between ceramic and metal components often depends on the specific requirements of the semiconductor manufacturing process, with each offering unique advantages. For instance, while ceramic components are preferred for their insulating properties, metal components are chosen for their conductivity and strength. The integration of both ceramic and metal components is often necessary to achieve the desired performance and reliability in semiconductor devices. As the semiconductor industry continues to evolve, the demand for both ceramic and metal components is expected to grow, driven by the need for more advanced and efficient semiconductor devices. Manufacturers in this market are continually innovating to develop new materials and manufacturing techniques that can enhance the performance of their components. This includes the development of advanced ceramics with improved thermal and electrical properties, as well as the use of novel metal alloys that offer superior conductivity and strength. The ongoing advancements in semiconductor technology, such as the transition to smaller and more complex device architectures, are also driving the demand for precision components that can support these innovations. As a result, the Global Precision Components for Semiconductors Market is a dynamic and rapidly evolving sector, with significant opportunities for growth and development.

Etch Equipment, Lithography Machines, Track, Deposition, Cleaning Equipment, CMP, Heat Treatment Equipment, Ion Implant, Metrology and Inspection, Others in the Global Precision Components for Semiconductors Market:

The usage of Global Precision Components for Semiconductors Market spans across various critical areas of semiconductor manufacturing, each requiring specific components to ensure optimal performance and efficiency. In etch equipment, precision components are essential for maintaining the accuracy and consistency of the etching process, which is crucial for defining the intricate patterns on semiconductor wafers. Lithography machines, which are used to transfer circuit patterns onto wafers, rely heavily on precision components to achieve the high levels of accuracy required for modern semiconductor devices. Track equipment, which is used in conjunction with lithography machines, also depends on precision components to ensure the precise application of photoresist materials. In deposition processes, precision components are used to control the uniformity and thickness of the material layers deposited onto wafers, which is critical for the performance of the final semiconductor devices. Cleaning equipment, which is used to remove contaminants from wafers, requires precision components to ensure thorough and efficient cleaning without damaging the delicate structures on the wafers. Chemical Mechanical Planarization (CMP) equipment, which is used to smooth and flatten wafer surfaces, relies on precision components to achieve the desired surface finish and uniformity. Heat treatment equipment, which is used to alter the properties of semiconductor materials through controlled heating and cooling, requires precision components to maintain the precise temperature and timing needed for each process. Ion implant equipment, which is used to introduce dopants into semiconductor materials, depends on precision components to control the dose and energy of the ions being implanted. Metrology and inspection equipment, which are used to measure and evaluate the quality of semiconductor wafers, rely on precision components to achieve the high levels of accuracy and resolution needed for these tasks. Other areas of semiconductor manufacturing, such as packaging and testing, also require precision components to ensure the reliability and performance of the final semiconductor products. The integration of precision components in these various areas is essential for the overall efficiency and effectiveness of semiconductor manufacturing processes. As the demand for more advanced and complex semiconductor devices continues to grow, the need for high-quality precision components in these areas is expected to increase. Manufacturers in the Global Precision Components for Semiconductors Market are continually developing new and improved components to meet the evolving needs of the semiconductor industry. This includes the development of components with enhanced performance characteristics, such as improved thermal and electrical properties, as well as the use of advanced manufacturing techniques to achieve higher levels of precision and accuracy. The ongoing advancements in semiconductor technology, such as the transition to smaller and more complex device architectures, are also driving the demand for precision components that can support these innovations. As a result, the Global Precision Components for Semiconductors Market is a dynamic and rapidly evolving sector, with significant opportunities for growth and development.

Global Precision Components for Semiconductors Market Outlook:

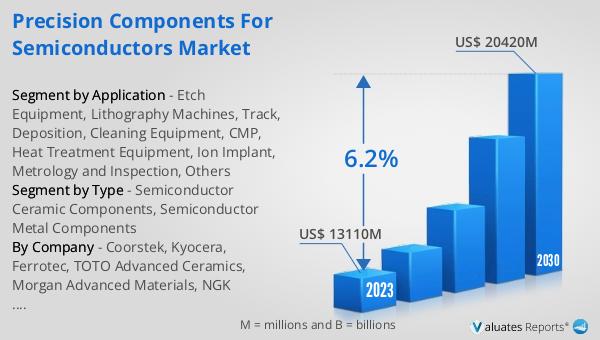

In 2024, the global market for Precision Components for Semiconductors was valued at approximately $15,010 million. It is anticipated to expand to a revised size of around $22,770 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.2% over the forecast period. According to SEMI, worldwide sales of semiconductor manufacturing equipment saw a 5% increase, rising from $102.6 billion in 2021 to a record-breaking $107.6 billion in 2022. For the third consecutive year, China maintained its position as the largest semiconductor equipment market in 2022, despite experiencing a 5% slowdown in investment growth year-over-year. The region accounted for $28.3 billion in billings. This data underscores the robust demand for semiconductor manufacturing equipment and the critical role of precision components in supporting this growth. The market's expansion is driven by the increasing complexity of semiconductor devices and the need for high-quality components that can support advanced manufacturing techniques. As the semiconductor industry continues to evolve, the demand for precision components is expected to grow, driven by the need for more advanced and efficient semiconductor devices. Manufacturers in this market are continually innovating to develop new materials and manufacturing techniques that can enhance the performance of their components. This includes the development of advanced ceramics with improved thermal and electrical properties, as well as the use of novel metal alloys that offer superior conductivity and strength. The ongoing advancements in semiconductor technology, such as the transition to smaller and more complex device architectures, are also driving the demand for precision components that can support these innovations. As a result, the Global Precision Components for Semiconductors Market is a dynamic and rapidly evolving sector, with significant opportunities for growth and development.

| Report Metric | Details |

| Report Name | Precision Components for Semiconductors Market |

| Accounted market size in year | US$ 15010 million |

| Forecasted market size in 2031 | US$ 22770 million |

| CAGR | 6.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Coorstek, Kyocera, Ferrotec, TOTO Advanced Ceramics, Morgan Advanced Materials, NGK Insulators, MiCo Ceramics Co., Ltd., ASUZAC Fine Ceramics, NGK Spark Plug (NTK Ceratec), Shinko Electric Industries, BOBOO Hitech, BACH Resistor Ceramics, Watlow (CRC), Durex Industries, Sumitomo Electric, Momentive Technologies, Shin-Etsu MicroSi, Boboo Hi-Tech, Entegris, Technetics Semi, Fiti Group, Tokai Carbon, VERSA CONN CORP (VCC), KFMI, Shenyang Fortune Precision Equipment Co., Ltd, Sprint Precision Technologies Co., Ltd, Thinkon Semiconductor, Tolerance, Beijing U-PRECISION TECH CO., LTD., SoValue Semiconductor, Lintech Corporation, FEMVIX CORP, TTS Co., Ltd., Nanotech Co. Ltd., KSM Component, AK Tech Co.,Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |