What is Global Aspheric IOL Market?

The Global Aspheric Intraocular Lens (IOL) Market is a specialized segment within the broader ophthalmic devices industry. Aspheric IOLs are advanced lenses implanted in the eye to replace the natural lens during cataract surgery. Unlike traditional spherical IOLs, aspheric IOLs are designed to reduce spherical aberrations, providing clearer and sharper vision. These lenses are particularly beneficial for patients with higher visual demands, such as those who drive at night or read extensively. The market for aspheric IOLs is driven by the increasing prevalence of cataracts, advancements in lens technology, and a growing aging population. Additionally, the rising awareness about the benefits of aspheric IOLs over traditional lenses is contributing to market growth. The market is characterized by the presence of several key players who are continuously innovating to improve lens performance and patient outcomes. The adoption of aspheric IOLs is also supported by favorable reimbursement policies in many regions, making these advanced lenses more accessible to a broader patient base. Overall, the Global Aspheric IOL Market is poised for significant growth as more patients and healthcare providers recognize the advantages of these lenses in improving visual quality and overall quality of life.

Non-foldable Lenses, Foldable Intraocular Lenses in the Global Aspheric IOL Market:

Non-foldable lenses and foldable intraocular lenses (IOLs) are two primary types of lenses used in the Global Aspheric IOL Market. Non-foldable lenses are typically made from rigid materials such as polymethyl methacrylate (PMMA). These lenses require a larger incision during cataract surgery, which can lead to longer recovery times and a higher risk of complications. Despite these drawbacks, non-foldable lenses are still used in certain situations, particularly in regions where advanced surgical equipment may not be readily available. On the other hand, foldable intraocular lenses are made from flexible materials like silicone or acrylic, allowing them to be folded and inserted through a smaller incision. This minimally invasive approach reduces recovery time and lowers the risk of surgical complications. Foldable IOLs are further categorized into monofocal, multifocal, and toric lenses. Monofocal lenses provide clear vision at one distance, usually far, while multifocal lenses offer multiple focal points, allowing for better near, intermediate, and distance vision. Toric lenses are specifically designed to correct astigmatism, providing sharper vision for patients with this condition. The choice between non-foldable and foldable lenses depends on various factors, including the patient's specific needs, the surgeon's expertise, and the available surgical infrastructure. In the Global Aspheric IOL Market, foldable lenses are increasingly preferred due to their numerous advantages, including improved patient comfort and quicker recovery times. However, non-foldable lenses still hold a niche market, particularly in developing regions where cost and accessibility are significant considerations. Both types of lenses play a crucial role in addressing the diverse needs of cataract patients worldwide, contributing to the overall growth and development of the Global Aspheric IOL Market.

Public Hospital, Private Hospital in the Global Aspheric IOL Market:

The usage of Global Aspheric IOLs in public and private hospitals varies significantly, reflecting differences in resources, patient demographics, and healthcare policies. In public hospitals, which are often government-funded, the focus is typically on providing essential healthcare services to a broad population base. These hospitals may have limited budgets and resources, which can impact the availability and adoption of advanced medical technologies like aspheric IOLs. However, public hospitals play a crucial role in offering cataract surgeries to underserved populations, including the elderly and low-income patients. In many regions, public hospitals are the primary providers of cataract surgery, and efforts are being made to incorporate aspheric IOLs into their offerings to improve patient outcomes. Government initiatives and subsidies can also facilitate the adoption of these advanced lenses in public healthcare settings. On the other hand, private hospitals, which are often funded through private investments and patient fees, generally have more resources and flexibility in adopting new technologies. These hospitals cater to patients who can afford higher out-of-pocket expenses and are often more willing to invest in advanced treatments like aspheric IOLs. Private hospitals are known for their state-of-the-art facilities, experienced surgeons, and personalized patient care, making them attractive options for patients seeking premium healthcare services. The adoption of aspheric IOLs in private hospitals is driven by the demand for high-quality vision correction and the desire to offer the latest advancements in ophthalmic care. Additionally, private hospitals often engage in marketing and educational campaigns to raise awareness about the benefits of aspheric IOLs, further driving their adoption. Overall, both public and private hospitals play vital roles in the Global Aspheric IOL Market, each contributing to the market's growth in unique ways. While public hospitals focus on accessibility and affordability, private hospitals emphasize advanced technology and premium patient care, together ensuring that a wide range of patients can benefit from the advantages of aspheric IOLs.

Global Aspheric IOL Market Outlook:

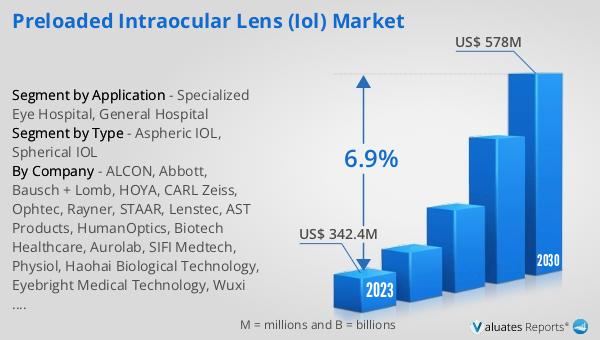

The global Aspheric IOL market was valued at US$ 542.7 million in 2023 and is anticipated to reach US$ 842 million by 2030, witnessing a CAGR of 6.6% during the forecast period 2024-2030. This market outlook indicates a robust growth trajectory driven by several key factors. The increasing prevalence of cataracts, particularly among the aging population, is a significant driver of market growth. As the global population continues to age, the demand for cataract surgeries and advanced intraocular lenses like aspheric IOLs is expected to rise. Additionally, advancements in lens technology and surgical techniques are making aspheric IOLs more accessible and effective, further boosting their adoption. The market is also benefiting from growing awareness about the superior visual outcomes provided by aspheric IOLs compared to traditional spherical lenses. Healthcare providers and patients alike are recognizing the value of these advanced lenses in improving quality of life, leading to increased demand. Furthermore, favorable reimbursement policies in many regions are making aspheric IOLs more affordable for a broader patient base. The presence of key market players who are continuously innovating and improving lens performance is also contributing to the market's growth. Overall, the Global Aspheric IOL Market is poised for significant expansion, driven by a combination of demographic trends, technological advancements, and increasing awareness about the benefits of aspheric IOLs.

| Report Metric | Details |

| Report Name | Aspheric IOL Market |

| Accounted market size in 2023 | US$ 542.7 million |

| Forecasted market size in 2030 | US$ 842 million |

| CAGR | 6.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | ALCON, AMO(Abbott), Bausch + Lomb, HOYA, CARL Zeiss, Ophtec, Rayner, STAAR, Lenstec, HumanOptics, Biotech Visioncare, Omni Lens Pvt Ltd, Aurolab, SAV-IOL, Eagle Optics, SIFI Medtech, Physiol, Haohai Biological Technology, Eyebright Medical Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |