What is Global Flue Pipe Market?

The Global Flue Pipe Market is a significant segment within the broader heating and ventilation industry, focusing on the components that facilitate the safe and efficient expulsion of exhaust gases from fireplaces, stoves, and industrial applications. Flue pipes are essential for directing combustion gases away from living spaces, ensuring safety and compliance with environmental regulations. The market encompasses a variety of flue pipe types, including twin wall, single wall, and flexible chimney liners, each designed to meet specific installation and performance requirements. The demand for flue pipes is driven by the need for efficient heating solutions, stringent environmental standards, and the growing adoption of renewable energy sources that require specialized venting systems. As urbanization and industrialization continue to rise globally, the flue pipe market is expected to expand, driven by new construction projects and the retrofitting of existing buildings. Additionally, advancements in materials and technology are leading to the development of more durable and efficient flue systems, further propelling market growth. The market is characterized by a mix of established players and new entrants, all striving to innovate and capture a share of this essential industry.

Twin Wall Flue Pipes, Single Wall Flue Pipes, Flexible Chimney Flue Liner, Others in the Global Flue Pipe Market:

Twin wall flue pipes are a popular choice in the Global Flue Pipe Market due to their robust construction and superior insulation properties. These pipes consist of two layers of stainless steel with an insulating layer in between, which helps maintain the temperature of the flue gases and prevents condensation. This design makes them ideal for use in both residential and commercial settings, where maintaining consistent temperatures is crucial for efficiency and safety. Twin wall flue pipes are often used in situations where the flue needs to pass through walls or roofs, as their insulation minimizes heat loss and reduces the risk of fire hazards. On the other hand, single wall flue pipes are typically used in applications where the flue is not exposed to cold temperatures or where the pipe is installed within a chimney. These pipes are more economical and easier to install, making them a popular choice for straightforward installations. However, they lack the insulation properties of twin wall pipes, which can lead to heat loss and condensation issues if not properly managed. Flexible chimney flue liners are another critical component of the flue pipe market, designed to navigate the twists and turns of existing chimneys. These liners are made from stainless steel and are highly adaptable, making them ideal for retrofitting older chimneys that may not be perfectly straight. They provide a cost-effective solution for improving the safety and efficiency of existing chimney systems, ensuring that exhaust gases are safely expelled from the building. Other types of flue pipes in the market include ceramic and clay flue liners, which are often used in traditional masonry chimneys. These liners offer excellent durability and heat resistance, making them a long-lasting option for chimney construction. However, they can be more challenging to install and may require professional expertise to ensure a proper fit. Overall, the Global Flue Pipe Market offers a diverse range of products to meet the varying needs of consumers, from high-performance twin wall systems to flexible liners for older chimneys. As technology advances and environmental regulations become more stringent, the market is likely to see continued innovation and growth, with manufacturers focusing on developing more efficient and sustainable flue solutions.

Standard Fireplaces, Stoves, Industrial Application in the Global Flue Pipe Market:

The Global Flue Pipe Market plays a crucial role in the functionality and safety of standard fireplaces, stoves, and industrial applications. In standard fireplaces, flue pipes are essential for directing smoke and combustion gases out of the home, preventing the buildup of harmful substances like carbon monoxide. Properly installed flue pipes ensure that fireplaces operate efficiently, providing warmth and ambiance without compromising indoor air quality. The choice of flue pipe can significantly impact the performance of a fireplace, with twin wall systems offering superior insulation and safety features for modern installations. In the context of stoves, flue pipes are equally important for ensuring safe and efficient operation. Wood-burning and pellet stoves rely on flue systems to expel exhaust gases and maintain optimal combustion conditions. The type of flue pipe used can affect the stove's efficiency, with insulated twin wall pipes often recommended for installations where the flue passes through unheated spaces. Flexible chimney liners are also commonly used in stove installations, particularly when retrofitting existing chimneys to accommodate new appliances. In industrial applications, flue pipes are critical for managing the exhaust from large-scale combustion processes. Factories and power plants use flue systems to control emissions and comply with environmental regulations, making them an integral part of industrial operations. The materials and design of industrial flue pipes must withstand high temperatures and corrosive gases, often requiring specialized coatings and construction techniques. The Global Flue Pipe Market caters to these diverse applications by offering a range of products designed to meet specific performance and regulatory requirements. As industries continue to prioritize sustainability and efficiency, the demand for advanced flue systems is expected to grow, driving innovation and development within the market.

Global Flue Pipe Market Outlook:

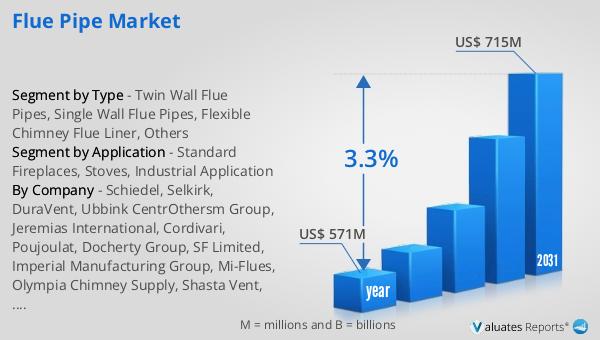

In 2024, the global flue pipe market was valued at approximately $571 million. Looking ahead, projections indicate that by 2031, this market is expected to expand to a revised size of around $715 million. This growth trajectory represents a compound annual growth rate (CAGR) of 3.3% over the forecast period. This steady growth reflects the increasing demand for efficient and environmentally friendly heating solutions across various sectors, including residential, commercial, and industrial applications. The market's expansion is driven by several factors, including the rising adoption of renewable energy sources, which often require specialized venting systems, and the ongoing need for retrofitting and upgrading existing heating systems to meet modern efficiency standards. Additionally, stringent environmental regulations are pushing manufacturers to innovate and develop more sustainable flue pipe solutions, further contributing to market growth. As urbanization and industrialization continue to rise globally, the demand for flue pipes is expected to increase, supported by new construction projects and the retrofitting of existing buildings. The market is characterized by a mix of established players and new entrants, all striving to capture a share of this essential industry through innovation and competitive pricing strategies.

| Report Metric | Details |

| Report Name | Flue Pipe Market |

| Accounted market size in year | US$ 571 million |

| Forecasted market size in 2031 | US$ 715 million |

| CAGR | 3.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Schiedel, Selkirk, DuraVent, Ubbink CentrOthersm Group, Jeremias International, Cordivari, Poujoulat, Docherty Group, SF Limited, Imperial Manufacturing Group, Mi-Flues, Olympia Chimney Supply, Shasta Vent, Security Chimneys International, Ruilun Metal Products |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |