What is Global Smart Noise-Canceling Glass Facades Market?

The Global Smart Noise-Canceling Glass Facades Market represents a cutting-edge segment within the architectural and construction industries, focusing on the development and implementation of advanced glass facades that significantly reduce noise pollution. These innovative glass facades are designed to enhance the acoustic comfort of buildings by minimizing the intrusion of external noise, such as traffic, construction, and urban activities. This market is driven by the increasing demand for quieter and more serene indoor environments, particularly in urban areas where noise pollution is a growing concern. The technology behind these facades involves the integration of soundproofing materials and advanced engineering techniques to create glass panels that can effectively block or absorb sound waves. As urbanization continues to rise globally, the need for smart noise-canceling solutions in both residential and commercial buildings is becoming more pronounced. This market is poised for significant growth as more architects and builders recognize the value of incorporating noise-canceling features into their designs, thereby improving the quality of life for occupants and enhancing the overall appeal of modern structures. The Global Smart Noise-Canceling Glass Facades Market is not only about reducing noise but also about creating sustainable and energy-efficient building solutions that align with contemporary architectural trends.

Active Noise-Canceling Glass Facades, Passive Noise-Canceling Glass Facades in the Global Smart Noise-Canceling Glass Facades Market:

Active Noise-Canceling Glass Facades and Passive Noise-Canceling Glass Facades are two primary categories within the Global Smart Noise-Canceling Glass Facades Market, each offering unique benefits and applications. Active noise-canceling glass facades utilize advanced technology to counteract sound waves. This is achieved through the use of microphones and speakers embedded within the glass panels. The microphones detect incoming noise, and the system generates sound waves that are the exact opposite, effectively canceling out the noise. This technology is particularly effective in environments with fluctuating noise levels, such as near airports or busy highways. Active noise-canceling systems are highly adaptable and can be fine-tuned to address specific noise frequencies, making them ideal for high-end commercial buildings and luxury residential projects where noise reduction is a priority. On the other hand, Passive Noise-Canceling Glass Facades rely on the physical properties of materials to block or absorb sound. These facades are constructed using multiple layers of glass and specialized acoustic interlayers that dampen sound vibrations. The design of passive systems is focused on maximizing the mass and thickness of the glass, as well as incorporating air gaps that act as sound barriers. While passive systems may not offer the same level of precision as active systems, they are highly effective in reducing low-frequency noise and are often more cost-effective. Passive noise-canceling facades are commonly used in standard residential and commercial buildings where budget constraints are a consideration. Both active and passive noise-canceling glass facades contribute to creating quieter indoor environments, but the choice between them depends on specific project requirements, budget, and the level of noise pollution in the surrounding area. As technology advances, the integration of smart features, such as automated adjustments based on real-time noise levels, is becoming more prevalent in both active and passive systems. This evolution is driving the market forward, offering architects and builders a range of options to enhance the acoustic performance of their projects. The Global Smart Noise-Canceling Glass Facades Market is witnessing a growing trend towards hybrid systems that combine both active and passive elements, providing a comprehensive solution to noise pollution challenges. These hybrid systems offer the best of both worlds, delivering superior noise reduction capabilities while maintaining energy efficiency and aesthetic appeal. As urban environments become increasingly noisy, the demand for innovative noise-canceling solutions is expected to rise, making smart glass facades an integral part of modern architectural design.

Commercial Buildings, Residential Buildings, Public Infrastructure, Others in the Global Smart Noise-Canceling Glass Facades Market:

The usage of Global Smart Noise-Canceling Glass Facades Market extends across various sectors, including commercial buildings, residential buildings, public infrastructure, and other areas, each benefiting from the unique advantages these facades offer. In commercial buildings, smart noise-canceling glass facades are increasingly being adopted to create more conducive working environments. Office spaces located in bustling urban centers often face challenges related to noise pollution, which can affect employee productivity and well-being. By incorporating noise-canceling glass facades, businesses can provide a quieter and more comfortable workspace, enhancing focus and reducing stress levels among employees. Additionally, these facades contribute to the aesthetic appeal of commercial buildings, offering sleek and modern designs that align with contemporary architectural trends. In residential buildings, the demand for noise-canceling solutions is driven by the desire for peaceful living spaces, particularly in densely populated urban areas. Homeowners and developers are increasingly recognizing the value of smart glass facades in enhancing the quality of life for residents by minimizing the intrusion of external noise. This is especially important in high-rise apartments and condominiums where proximity to busy streets and transportation hubs can result in significant noise disturbances. By investing in noise-canceling glass facades, residential buildings can offer a tranquil living environment, attracting potential buyers and tenants seeking refuge from the hustle and bustle of city life. Public infrastructure projects, such as airports, train stations, and hospitals, also benefit from the implementation of smart noise-canceling glass facades. In these settings, managing noise levels is crucial to ensuring the comfort and safety of occupants. For instance, airports can utilize noise-canceling facades to reduce the impact of aircraft noise on passengers and staff, while hospitals can create quieter environments conducive to patient recovery and well-being. The versatility of smart glass facades makes them an ideal choice for public infrastructure projects where noise reduction is a priority. Beyond these primary sectors, the Global Smart Noise-Canceling Glass Facades Market is also finding applications in other areas, such as educational institutions, hotels, and entertainment venues. Schools and universities can benefit from quieter classrooms and lecture halls, enhancing the learning experience for students. Hotels can offer guests a peaceful retreat, free from the disturbances of urban noise, while entertainment venues can improve acoustics and sound quality for performances and events. The adaptability and effectiveness of smart noise-canceling glass facades make them a valuable addition to a wide range of building projects, contributing to the creation of more comfortable and enjoyable spaces for occupants. As awareness of the benefits of noise-canceling solutions continues to grow, the market is expected to expand, with more industries recognizing the potential of smart glass facades to transform the built environment.

Global Smart Noise-Canceling Glass Facades Market Outlook:

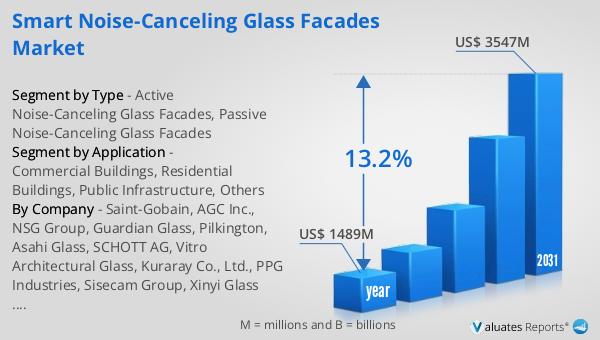

The outlook for the Global Smart Noise-Canceling Glass Facades Market is promising, with significant growth anticipated in the coming years. In 2024, the market was valued at approximately US$ 1489 million, reflecting the increasing demand for innovative noise-canceling solutions in the construction and architectural sectors. By 2031, the market is projected to reach a revised size of US$ 3547 million, indicating a robust compound annual growth rate (CAGR) of 13.2% during the forecast period. This growth is driven by several factors, including the rising awareness of the negative impacts of noise pollution on health and well-being, as well as the growing trend towards sustainable and energy-efficient building practices. As urbanization continues to accelerate globally, the need for smart noise-canceling glass facades is becoming more pronounced, particularly in densely populated cities where noise pollution is a significant concern. The market's expansion is also supported by advancements in technology, which are enabling the development of more effective and versatile noise-canceling solutions. As a result, architects, builders, and developers are increasingly incorporating smart glass facades into their projects, recognizing the value they bring in terms of enhancing acoustic comfort and improving the overall quality of life for building occupants. The Global Smart Noise-Canceling Glass Facades Market is poised for substantial growth, offering exciting opportunities for innovation and development in the years ahead.

| Report Metric | Details |

| Report Name | Smart Noise-Canceling Glass Facades Market |

| Accounted market size in year | US$ 1489 million |

| Forecasted market size in 2031 | US$ 3547 million |

| CAGR | 13.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Saint-Gobain, AGC Inc., NSG Group, Guardian Glass, Pilkington, Asahi Glass, SCHOTT AG, Vitro Architectural Glass, Kuraray Co., Ltd., PPG Industries, Sisecam Group, Xinyi Glass Holdings, CPG Europe, SageGlass, View Inc., Halio Inc., Smartglass International, Gentex Corporation, Magna International, Fuyao Glass Industry Group, Nippon Sheet Glass, Glas Trösch Group, Saint-Gobain Sekurit, AGP Group, Cardinal Glass Industries, Glasfabrik Lamberts, Sedak GmbH & Co. KG, Electrochromic Glass LLC, Innovative Glass Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |