What is Global Marine Exhaust Gas Desulfurization System Market?

The Global Marine Exhaust Gas Desulfurization System Market is a specialized segment within the broader maritime industry, focusing on technologies designed to reduce sulfur emissions from ship exhaust gases. These systems are crucial due to international regulations aimed at minimizing air pollution from ships, particularly sulfur oxides (SOx), which are harmful to both human health and the environment. The market encompasses various types of desulfurization systems, including open loop, closed loop, and hybrid systems, each offering different methods of removing sulfur from exhaust gases. The demand for these systems is driven by stringent environmental regulations, such as those imposed by the International Maritime Organization (IMO), which mandate a significant reduction in sulfur content in marine fuels. As a result, ship owners and operators are increasingly investing in these systems to comply with regulations and avoid penalties. The market is characterized by technological advancements and innovations aimed at improving the efficiency and cost-effectiveness of desulfurization systems. Additionally, the market is witnessing a growing interest in sustainable and eco-friendly solutions, further propelling the development and adoption of advanced marine exhaust gas desulfurization systems.

Open Loop System, Closed Loop System, Others in the Global Marine Exhaust Gas Desulfurization System Market:

The Global Marine Exhaust Gas Desulfurization System Market is segmented into various types, including open loop systems, closed loop systems, and others, each offering distinct advantages and operational mechanisms. Open loop systems are the most commonly used type and operate by utilizing seawater to wash the exhaust gases, effectively removing sulfur oxides. The process involves drawing in seawater, which is then sprayed into the exhaust gas stream. The sulfur oxides react with the water, forming sulfuric acid, which is then neutralized by the natural alkalinity of the seawater. The treated water is then discharged back into the sea, adhering to environmental regulations. Open loop systems are favored for their simplicity and cost-effectiveness, especially in areas where seawater is abundant and regulations permit their use. However, they are less effective in areas with low alkalinity water or strict discharge regulations. Closed loop systems, on the other hand, use a recirculating process where freshwater mixed with an alkaline substance, such as sodium hydroxide, is used to scrub the exhaust gases. The sulfur oxides are absorbed by the alkaline solution, forming a neutral salt solution. This system is advantageous in areas where open loop systems are not feasible due to environmental restrictions or low alkalinity seawater. Closed loop systems offer greater control over emissions and discharge, making them suitable for use in sensitive marine environments. However, they are generally more complex and costly to install and maintain compared to open loop systems. In addition to open and closed loop systems, there are hybrid systems that combine the features of both. Hybrid systems offer the flexibility to switch between open and closed loop modes depending on the environmental conditions and regulatory requirements. This adaptability makes them an attractive option for vessels operating in diverse regions with varying regulations. Hybrid systems provide the benefits of both systems, ensuring compliance with stringent emission standards while optimizing operational efficiency. Despite their higher initial cost, the long-term benefits of hybrid systems, such as reduced fuel consumption and lower operational costs, make them a viable investment for ship owners and operators. Other types of systems in the market include dry scrubbers and advanced technologies that utilize alternative methods for sulfur removal. Dry scrubbers, for instance, use a dry sorbent material to capture sulfur oxides from the exhaust gases. These systems are less common but offer advantages in terms of reduced water usage and waste generation. As the market continues to evolve, there is a growing focus on developing innovative solutions that enhance the efficiency and sustainability of marine exhaust gas desulfurization systems. This includes the integration of digital technologies and automation to optimize system performance and reduce operational costs. Overall, the Global Marine Exhaust Gas Desulfurization System Market is characterized by a diverse range of technologies, each catering to specific operational and regulatory needs, driving the adoption of cleaner and more efficient solutions in the maritime industry.

Commercial Vessels, Passenger Vessels, Military Vessels in the Global Marine Exhaust Gas Desulfurization System Market:

The usage of Global Marine Exhaust Gas Desulfurization Systems is prevalent across various types of vessels, including commercial vessels, passenger vessels, and military vessels, each with unique operational requirements and regulatory considerations. Commercial vessels, such as cargo ships and tankers, are the primary users of these systems due to their significant contribution to global shipping emissions. These vessels operate on heavy fuel oil, which contains high levels of sulfur, making them a major source of sulfur oxides. By installing desulfurization systems, commercial vessel operators can significantly reduce their sulfur emissions, ensuring compliance with international regulations and avoiding potential fines. The adoption of these systems also enhances the environmental sustainability of commercial shipping operations, aligning with the growing demand for greener shipping practices. Passenger vessels, including cruise ships and ferries, also utilize marine exhaust gas desulfurization systems to meet stringent emission standards. These vessels often operate in environmentally sensitive areas, such as coastal regions and tourist destinations, where air quality regulations are more stringent. By implementing desulfurization systems, passenger vessel operators can minimize their environmental impact, ensuring a cleaner and healthier environment for passengers and local communities. Additionally, the use of these systems can enhance the reputation of passenger vessel operators, as travelers increasingly prioritize environmentally responsible travel options. The integration of advanced desulfurization technologies in passenger vessels also contributes to improved air quality onboard, enhancing the overall passenger experience. Military vessels, such as naval ships and submarines, also benefit from the use of marine exhaust gas desulfurization systems. These vessels operate in diverse environments and are subject to strict emission regulations, particularly when operating in international waters or near coastal areas. By adopting desulfurization systems, military vessel operators can ensure compliance with environmental standards while maintaining operational readiness. The use of these systems also aligns with the broader sustainability goals of military organizations, contributing to reduced environmental impact and enhanced energy efficiency. Furthermore, the integration of advanced desulfurization technologies in military vessels can enhance their operational capabilities, enabling them to operate more efficiently and effectively in various maritime environments. Overall, the usage of Global Marine Exhaust Gas Desulfurization Systems across commercial, passenger, and military vessels underscores the importance of these technologies in promoting environmental sustainability and regulatory compliance in the maritime industry. As the demand for cleaner and more efficient shipping solutions continues to grow, the adoption of advanced desulfurization systems is expected to increase, driving further innovation and development in the market. The integration of these systems not only helps vessel operators meet regulatory requirements but also enhances their operational efficiency and environmental performance, contributing to a more sustainable and responsible maritime industry.

Global Marine Exhaust Gas Desulfurization System Market Outlook:

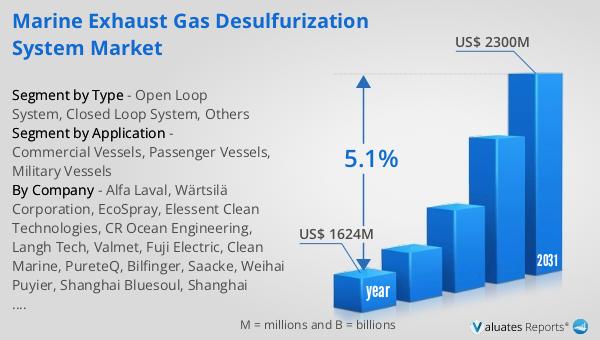

The global market for Marine Exhaust Gas Desulfurization Systems was valued at $1,624 million in 2024 and is anticipated to expand to a revised size of $2,300 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.1% during the forecast period. This growth trajectory underscores the increasing demand for effective solutions to reduce sulfur emissions from marine vessels, driven by stringent international regulations and a growing emphasis on environmental sustainability. The market's expansion is fueled by the need for ship operators to comply with the International Maritime Organization's (IMO) regulations, which mandate a significant reduction in sulfur content in marine fuels. As a result, there is a heightened focus on adopting advanced desulfurization technologies that not only meet regulatory requirements but also enhance operational efficiency and reduce environmental impact. The projected growth of the market also highlights the ongoing technological advancements and innovations in the field of marine exhaust gas desulfurization. Companies are investing in research and development to create more efficient, cost-effective, and environmentally friendly solutions that cater to the diverse needs of the maritime industry. This includes the development of hybrid systems that offer greater flexibility and adaptability, as well as the integration of digital technologies to optimize system performance and reduce operational costs. As the market continues to evolve, there is a growing emphasis on sustainability and eco-friendly solutions, driving the adoption of cleaner and more efficient desulfurization systems. In conclusion, the global market for Marine Exhaust Gas Desulfurization Systems is poised for significant growth, driven by regulatory pressures and the increasing demand for sustainable shipping solutions. The market's expansion reflects the industry's commitment to reducing its environmental footprint and enhancing the sustainability of maritime operations. As ship operators continue to invest in advanced desulfurization technologies, the market is expected to witness further innovation and development, contributing to a cleaner and more sustainable future for the maritime industry.

| Report Metric | Details |

| Report Name | Marine Exhaust Gas Desulfurization System Market |

| Accounted market size in year | US$ 1624 million |

| Forecasted market size in 2031 | US$ 2300 million |

| CAGR | 5.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Alfa Laval, Wärtsilä Corporation, EcoSpray, Elessent Clean Technologies, CR Ocean Engineering, Langh Tech, Valmet, Fuji Electric, Clean Marine, PureteQ, Bilfinger, Saacke, Weihai Puyier, Shanghai Bluesoul, Shanghai ContiOcean Group, Zhejiang Energy Marine Environmental Technology, CPGC, Qingdao Headway Technology Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |