What is Global Nuclear Safety Valve Market?

The Global Nuclear Safety Valve Market is a specialized segment within the broader industrial valve market, focusing on the safety and regulatory needs of nuclear power plants. These valves are critical components designed to ensure the safe operation of nuclear reactors by controlling the flow of fluids and gases, thereby preventing accidents and maintaining operational stability. The market is driven by the increasing demand for nuclear energy as a clean and efficient power source, coupled with stringent safety regulations imposed by governments worldwide. As nuclear power plants age, the need for maintenance and replacement of safety valves also contributes to market growth. Technological advancements in valve design and materials have further enhanced the reliability and efficiency of these safety valves, making them indispensable in modern nuclear facilities. The market is characterized by a mix of established players and new entrants, all striving to innovate and meet the evolving safety standards. With the global push towards reducing carbon emissions, the nuclear safety valve market is poised for steady growth as countries invest in nuclear energy infrastructure. The market's expansion is also supported by the increasing number of nuclear reactors being constructed, particularly in emerging economies.

Spring-Loaded Safety Valve, Pilot-Operated Safety Valve, Bellows-Type Safety Valve, Others in the Global Nuclear Safety Valve Market:

The Global Nuclear Safety Valve Market encompasses various types of valves, each serving a unique function in ensuring the safety and efficiency of nuclear power plants. Among these, the Spring-Loaded Safety Valve is one of the most commonly used types. It operates on a simple mechanism where a spring holds the valve closed under normal conditions. When the pressure exceeds a predetermined limit, the spring compresses, allowing the valve to open and release excess pressure. This type of valve is favored for its reliability and simplicity, making it a staple in many nuclear facilities. The Pilot-Operated Safety Valve, on the other hand, offers more precision and control. It uses a pilot valve to control the main valve, allowing for more accurate pressure management. This type of valve is particularly useful in applications where precise pressure control is critical, such as in high-pressure steam systems. The Bellows-Type Safety Valve is designed to handle back pressure and is often used in systems where back pressure can affect valve performance. The bellows isolate the valve's internal components from the process fluid, enhancing durability and reliability. This type of valve is essential in environments where corrosive or high-temperature fluids are present. Other types of safety valves in the market include the balanced safety valve, which is designed to minimize the effects of back pressure, and the pressure relief valve, which is used to release excess pressure in a controlled manner. Each type of valve plays a crucial role in maintaining the safety and efficiency of nuclear power plants, and their selection depends on the specific requirements of the application. The diversity of valve types in the Global Nuclear Safety Valve Market reflects the complexity and varied needs of nuclear power plants, highlighting the importance of choosing the right valve for each application to ensure optimal performance and safety.

Reactor Coolant System (RCP), Steam Generator System, Residual Heat Removal System (RHR), Emergency Core Cooling System (ECCS), Spent Fuel Storage and Reprocessing Facility, Others in the Global Nuclear Safety Valve Market:

The Global Nuclear Safety Valve Market plays a vital role in various critical areas of nuclear power plants, ensuring the safe and efficient operation of these facilities. In the Reactor Coolant System (RCP), safety valves are essential for maintaining the pressure and temperature of the coolant, preventing overheating and potential reactor damage. These valves help regulate the flow of coolant, ensuring that the reactor core remains at a stable temperature. In the Steam Generator System, safety valves are used to control the pressure of steam produced by the reactor. They prevent over-pressurization, which could lead to equipment failure or even catastrophic accidents. The Residual Heat Removal System (RHR) relies on safety valves to manage the removal of residual heat from the reactor core after shutdown. These valves ensure that the heat is dissipated safely, preventing damage to the reactor and surrounding equipment. The Emergency Core Cooling System (ECCS) is another critical area where safety valves are indispensable. In the event of a loss of coolant accident, these valves help maintain the flow of coolant to the reactor core, preventing overheating and potential meltdown. In Spent Fuel Storage and Reprocessing Facilities, safety valves are used to manage the pressure and temperature of stored spent fuel, ensuring safe storage and handling. Other areas where safety valves are crucial include containment systems, where they help maintain the integrity of the containment structure by regulating pressure and preventing leaks. Overall, the Global Nuclear Safety Valve Market is integral to the safe and efficient operation of nuclear power plants, providing essential components that ensure the stability and safety of various critical systems.

Global Nuclear Safety Valve Market Outlook:

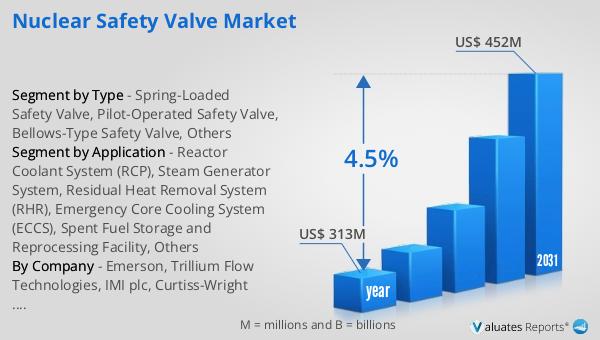

In 2024, the global market for Nuclear Safety Valves was valued at approximately $313 million. This market is projected to grow significantly, reaching an estimated size of $452 million by 2031. This growth represents a compound annual growth rate (CAGR) of 4.5% over the forecast period. The increasing demand for nuclear energy, driven by the need for clean and efficient power sources, is a key factor contributing to this market expansion. As countries worldwide strive to reduce carbon emissions and transition to more sustainable energy solutions, the role of nuclear power becomes increasingly important. This, in turn, drives the demand for safety valves, which are critical components in ensuring the safe and efficient operation of nuclear power plants. Additionally, the aging infrastructure of existing nuclear facilities necessitates the replacement and upgrading of safety valves, further fueling market growth. Technological advancements in valve design and materials also contribute to the market's expansion, as they enhance the reliability and efficiency of these critical components. The market's growth is supported by the construction of new nuclear reactors, particularly in emerging economies, where the demand for energy is rapidly increasing. Overall, the Global Nuclear Safety Valve Market is poised for steady growth, driven by the increasing demand for nuclear energy and the need for reliable and efficient safety solutions.

| Report Metric | Details |

| Report Name | Nuclear Safety Valve Market |

| Accounted market size in year | US$ 313 million |

| Forecasted market size in 2031 | US$ 452 million |

| CAGR | 4.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Emerson, Trillium Flow Technologies, IMI plc, Curtiss-Wright Nuclear, Baker Hughes, Jacomex, Weir Group, Shanghai Valve Factory, WELDON VALVES, Vexve, Crane Nuclear, TVE Co., Ltd, Contro Valve, OKANO, Neway |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |