What is Global RFID Etching Antenna Market?

The Global RFID Etching Antenna Market is a rapidly evolving sector that plays a crucial role in the broader field of radio-frequency identification (RFID) technology. RFID technology is used to automatically identify and track tags attached to objects, and the etching antenna is a vital component of this system. These antennas are crafted using advanced etching techniques on materials like copper and aluminum, which are then integrated into RFID tags. The global market for these antennas is driven by the increasing demand for efficient tracking systems across various industries, including retail, logistics, and healthcare. The antennas are designed to be highly sensitive and efficient, ensuring accurate data transmission over varying distances. As businesses continue to seek ways to enhance operational efficiency and security, the demand for RFID etching antennas is expected to grow. This market is characterized by continuous innovation, with companies investing in research and development to produce antennas that are smaller, more efficient, and cost-effective. The global reach of this market is expanding, with significant growth opportunities in emerging economies where industries are rapidly adopting RFID technology to streamline operations and improve supply chain management.

RFID Copper Etched Antenna, RFID AL Etched Antenna in the Global RFID Etching Antenna Market:

RFID Copper Etched Antennas and RFID Aluminum (AL) Etched Antennas are two primary types of antennas used in the Global RFID Etching Antenna Market. Copper etched antennas are known for their excellent conductivity and durability, making them a popular choice for applications requiring high performance and reliability. These antennas are typically used in environments where signal strength and clarity are paramount, such as in logistics and supply chain management. The etching process involves creating intricate patterns on copper sheets, which are then integrated into RFID tags. This process ensures that the antennas can transmit and receive signals effectively, even in challenging conditions. On the other hand, RFID AL etched antennas are made from aluminum, which is a more cost-effective material compared to copper. While aluminum does not conduct electricity as efficiently as copper, it offers a good balance between performance and cost, making it suitable for applications where budget constraints are a consideration. These antennas are often used in retail and anti-counterfeiting labels, where the primary requirement is to ensure product authenticity and prevent fraud. The choice between copper and aluminum etched antennas depends largely on the specific needs of the application, including factors such as environmental conditions, required range, and budget. Both types of antennas are integral to the functioning of RFID systems, providing the necessary link between the RFID tag and the reader. As the demand for RFID technology continues to grow, manufacturers are focusing on improving the performance and reducing the cost of these antennas. Innovations in materials and etching techniques are enabling the production of antennas that are not only more efficient but also more environmentally friendly. For instance, some companies are exploring the use of biodegradable materials for antenna substrates, which could significantly reduce the environmental impact of RFID systems. Additionally, advancements in nanotechnology are opening up new possibilities for the design and manufacture of RFID antennas, allowing for even smaller and more efficient components. The global market for RFID etched antennas is highly competitive, with numerous players vying for market share. Companies are investing heavily in research and development to stay ahead of the competition and meet the evolving needs of their customers. This has led to a steady stream of new products and innovations, which are helping to drive the growth of the market. As industries continue to embrace RFID technology, the demand for high-quality, cost-effective antennas is expected to remain strong. The future of the Global RFID Etching Antenna Market looks promising, with significant opportunities for growth and innovation.

NFC Business Cards/Tickets, Retail/Anti-counterfeiting Labels, Logistics, Other in the Global RFID Etching Antenna Market:

The Global RFID Etching Antenna Market finds its applications in various areas, including NFC business cards and tickets, retail and anti-counterfeiting labels, logistics, and other sectors. In the realm of NFC business cards and tickets, RFID etching antennas play a pivotal role in enabling seamless communication between devices. These antennas are embedded in NFC-enabled cards and tickets, allowing users to exchange information with a simple tap. This technology is particularly useful in events and transportation, where quick and secure data exchange is essential. The antennas ensure that the communication is fast and reliable, enhancing the user experience and streamlining operations. In the retail sector, RFID etching antennas are used extensively in anti-counterfeiting labels. These antennas are integrated into product labels to verify authenticity and prevent fraud. By using RFID technology, retailers can track products throughout the supply chain, ensuring that only genuine products reach the consumers. This not only helps in protecting brand reputation but also enhances customer trust. The antennas used in these labels are designed to be discreet yet effective, providing a robust solution to the problem of counterfeiting. In logistics, RFID etching antennas are indispensable for efficient inventory management and tracking. These antennas are used in RFID tags attached to goods, enabling real-time tracking of products as they move through the supply chain. This technology allows companies to monitor inventory levels, reduce losses, and improve overall operational efficiency. The antennas are designed to withstand harsh environmental conditions, ensuring reliable performance even in challenging settings. Other areas where RFID etching antennas are used include healthcare, where they are employed in patient tracking and equipment management, and in the automotive industry, where they are used for vehicle identification and tracking. The versatility of RFID etching antennas makes them suitable for a wide range of applications, and their importance is only expected to grow as industries continue to adopt RFID technology. The Global RFID Etching Antenna Market is poised for significant growth, driven by the increasing demand for efficient and reliable tracking solutions across various sectors.

Global RFID Etching Antenna Market Outlook:

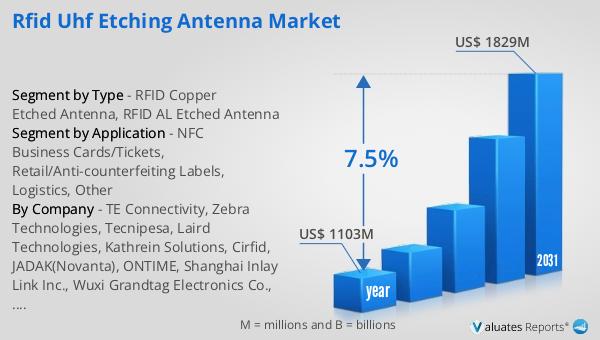

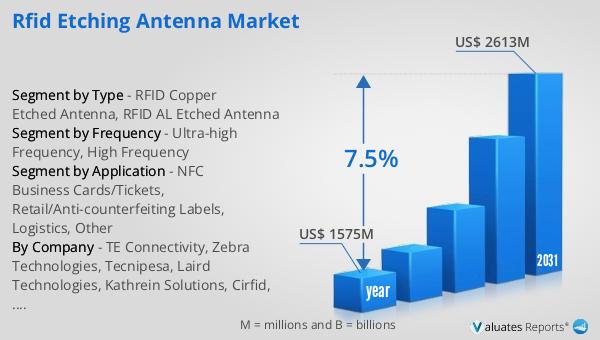

In 2024, the global market for RFID Etching Antennas was valued at approximately $1,575 million. This market is anticipated to expand significantly, reaching an estimated value of $2,613 million by the year 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 7.5% over the forecast period. The increasing adoption of RFID technology across various industries is a key driver of this growth. As businesses seek to enhance operational efficiency and security, the demand for RFID etching antennas is expected to rise. These antennas are crucial components of RFID systems, enabling accurate and efficient data transmission. The market's expansion is also fueled by continuous innovation in antenna design and manufacturing techniques, which are resulting in more efficient and cost-effective products. Companies are investing heavily in research and development to stay competitive and meet the evolving needs of their customers. This has led to a steady stream of new products and innovations, which are helping to drive the growth of the market. As industries continue to embrace RFID technology, the demand for high-quality, cost-effective antennas is expected to remain strong. The future of the Global RFID Etching Antenna Market looks promising, with significant opportunities for growth and innovation.

| Report Metric | Details |

| Report Name | RFID Etching Antenna Market |

| Accounted market size in year | US$ 1575 million |

| Forecasted market size in 2031 | US$ 2613 million |

| CAGR | 7.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Frequency |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TE Connectivity, Zebra Technologies, Tecnipesa, Laird Technologies, Kathrein Solutions, Cirfid, JADAK(Novanta), ONTIME, Shanghai Inlay Link Inc., Wuxi Grandtag Electronics Co., Ltd., Xiamen Innov Photoelectric Technology Co., Ltd., Wenzhou G.l.b Electronics Co., Ltd., YoungTek Electronics Corp., Smooth & Sharp Co., Ltd., Novatron Electronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |