What is Global All-In-One Kitchen Appliances Market?

The Global All-In-One Kitchen Appliances Market refers to a segment of the home appliance industry that focuses on multifunctional kitchen devices designed to perform multiple cooking tasks. These appliances combine various cooking functions such as blending, chopping, mixing, steaming, and even baking into a single unit, offering convenience and space-saving benefits to consumers. The market for these appliances is driven by the increasing demand for efficient and time-saving cooking solutions, especially among urban populations with busy lifestyles. As more people seek to simplify their kitchen routines without compromising on the quality of their meals, the popularity of all-in-one kitchen appliances continues to rise. These devices are particularly appealing to those living in smaller spaces, such as apartments, where kitchen space is limited. Additionally, the growing trend of smart home technology has led to the integration of advanced features in these appliances, such as touchscreens, programmable settings, and connectivity with other smart devices. This market is characterized by a wide range of products, from entry-level models to high-end appliances with sophisticated features, catering to different consumer needs and budgets. As a result, the Global All-In-One Kitchen Appliances Market is a dynamic and evolving sector within the broader home appliance industry.

<1000 Watts, 1000~1500 Watts, >1500 Watts in the Global All-In-One Kitchen Appliances Market:

In the Global All-In-One Kitchen Appliances Market, power consumption is a critical factor that influences the design and functionality of these devices. Appliances are typically categorized based on their wattage, which affects their performance and energy efficiency. The first category, <1000 Watts, includes appliances that are generally more energy-efficient and suitable for basic cooking tasks. These devices are ideal for consumers who prioritize energy savings and have less demanding cooking needs. They are often compact and designed for simple tasks such as blending, chopping, or steaming small quantities of food. Despite their lower power, these appliances can still offer a range of functionalities, making them a popular choice for individuals or small households. The second category, 1000~1500 Watts, represents a middle ground in terms of power and functionality. Appliances in this range are versatile and capable of handling a wider variety of cooking tasks compared to their lower-wattage counterparts. They are suitable for consumers who require more robust performance for tasks such as kneading dough, grinding, or cooking larger meals. These appliances strike a balance between energy efficiency and power, making them a practical choice for medium-sized households or those who frequently cook at home. The increased power allows for faster cooking times and the ability to handle more complex recipes, which can be a significant advantage for busy families. The third category, >1500 Watts, includes high-power appliances designed for heavy-duty cooking tasks. These devices are equipped with powerful motors and advanced features, making them suitable for professional chefs or avid home cooks who demand high performance and precision. Appliances in this category can handle large quantities of food and perform tasks such as grinding tough ingredients, baking, or even sous-vide cooking. While they consume more energy, the efficiency and speed they offer can be a worthwhile trade-off for those who prioritize performance over energy savings. These high-wattage appliances often come with premium features such as multiple cooking modes, programmable settings, and connectivity options, catering to tech-savvy consumers who seek the latest in kitchen technology. Overall, the wattage of an all-in-one kitchen appliance is a crucial consideration for consumers, as it directly impacts the appliance's capabilities and suitability for different cooking needs. Manufacturers in the Global All-In-One Kitchen Appliances Market continue to innovate and offer a diverse range of products across these wattage categories, ensuring that there is an option available for every type of consumer, from the energy-conscious to the performance-driven.

in the Global All-In-One Kitchen Appliances Market:

The Global All-In-One Kitchen Appliances Market serves a wide array of applications, catering to diverse consumer needs and preferences. These multifunctional devices are designed to simplify and enhance the cooking experience by combining several kitchen tasks into one appliance. One of the primary applications of these appliances is meal preparation, where they are used for chopping, slicing, and dicing ingredients quickly and efficiently. This is particularly beneficial for busy individuals or families who need to prepare meals in a short amount of time. The ability to perform multiple tasks with a single device reduces the need for multiple kitchen tools, saving both time and space. Another significant application is in the realm of healthy cooking. Many all-in-one kitchen appliances come equipped with steaming and blending functions, allowing users to prepare nutritious meals with minimal effort. This is especially appealing to health-conscious consumers who prioritize fresh and wholesome ingredients in their diets. The convenience of steaming vegetables or blending smoothies with a single appliance encourages healthier eating habits and makes it easier for individuals to incorporate more fruits and vegetables into their meals. Baking is another area where all-in-one kitchen appliances excel. With features such as dough kneading and precise temperature control, these devices can simplify the baking process for both novice and experienced bakers. The ability to mix, knead, and bake with one appliance reduces the complexity of baking and makes it more accessible to a wider audience. This versatility is particularly valuable for those who enjoy experimenting with different recipes and baking techniques. In addition to these applications, all-in-one kitchen appliances are also used for specialized cooking techniques such as sous-vide and slow cooking. These advanced features allow users to explore new culinary methods and achieve restaurant-quality results at home. The integration of smart technology in some models further enhances their functionality, enabling users to control and monitor their cooking remotely via smartphone apps. This level of convenience and innovation appeals to tech-savvy consumers who seek to streamline their cooking processes and enjoy a more connected kitchen experience. Overall, the Global All-In-One Kitchen Appliances Market offers a wide range of applications that cater to various cooking needs and preferences. From meal preparation and healthy cooking to baking and advanced culinary techniques, these multifunctional devices provide a convenient and efficient solution for modern kitchens. As consumer demand for versatile and time-saving kitchen appliances continues to grow, the market is poised to expand and evolve, offering even more innovative solutions for home cooks around the world.

Global All-In-One Kitchen Appliances Market Outlook:

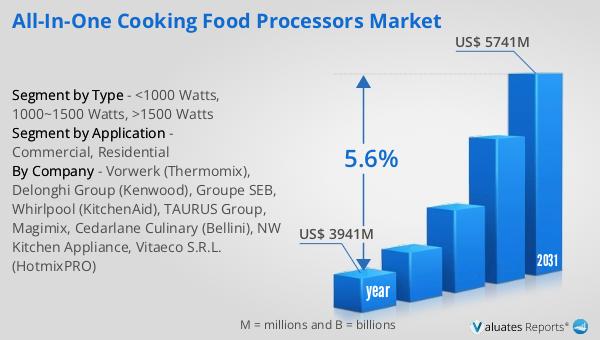

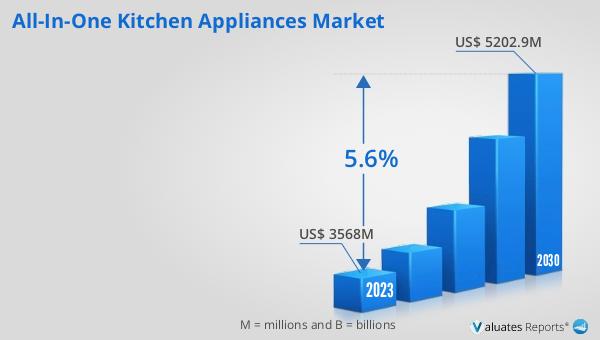

In 2024, the global market for All-In-One Kitchen Appliances was valued at approximately $3,941 million. This market is anticipated to experience significant growth over the coming years, with projections indicating that it will reach an estimated size of $5,741 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 5.6% during the forecast period. The increasing demand for multifunctional kitchen appliances that offer convenience and efficiency is a key driver of this market expansion. As consumers continue to seek out products that simplify their cooking processes and save time, the market for all-in-one kitchen appliances is expected to flourish. The integration of advanced features and smart technology in these appliances further enhances their appeal, attracting a broader range of consumers. This growth is also supported by the rising trend of urbanization and the increasing number of smaller households, where space-saving solutions are highly valued. As a result, the Global All-In-One Kitchen Appliances Market is poised for continued growth and innovation, offering a wide range of products that cater to the evolving needs of modern consumers.

| Report Metric | Details |

| Report Name | All-In-One Kitchen Appliances Market |

| Accounted market size in year | US$ 3941 million |

| Forecasted market size in 2031 | US$ 5741 million |

| CAGR | 5.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Sales Channel |

|

| Consumption by Region |

|

| By Company | Vorwerk (Thermomix), Magimix, Delonghi Group (Kenwood), Tefal (Groupe SEB), Whirlpool (KitchenAid), TAURUS Group, Conair Corporation(Cuisinart), BSH Home Appliances, All-Clad, Cedarlane Culinary (Bellini), NW Kitchen Appliance, Vitaeco S.R.L. (HotmixPRO), CookingPal, Chef Robot, HendiChef, Monsieur Cuisine, Tokit Omni Cook, Kogan ThermoBlend Elite |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |