What is N-acetylcysteine- Global Market?

N-acetylcysteine (NAC) is a compound that has gained significant attention in the global market due to its versatile applications and health benefits. It is a derivative of the amino acid cysteine and is known for its antioxidant properties. NAC is primarily used as a supplement to boost the levels of glutathione, a powerful antioxidant in the body, which helps in combating oxidative stress and maintaining cellular health. The global market for N-acetylcysteine is driven by its extensive use in the pharmaceutical industry, particularly in the treatment of conditions like chronic obstructive pulmonary disease (COPD), acetaminophen overdose, and other respiratory ailments. Additionally, NAC is utilized in the production of nutritional supplements aimed at enhancing immune function and detoxification processes. The demand for NAC is also fueled by its potential benefits in mental health, as studies suggest it may aid in managing psychiatric disorders such as depression and anxiety. With the increasing awareness of health and wellness, the market for N-acetylcysteine is expected to grow, as consumers seek natural and effective solutions for maintaining their health. The compound's multifaceted applications make it a valuable asset in both the medical and wellness industries, contributing to its expanding global market presence.

Injection, Granule for Oral Solution, Oral Inhalation, Effervescent Tablets, Others in the N-acetylcysteine- Global Market:

N-acetylcysteine is available in various forms, each catering to different needs and preferences in the global market. One of the most common forms is the injection, which is primarily used in medical settings for the treatment of acetaminophen overdose. This form of NAC is administered intravenously, allowing for rapid absorption and immediate therapeutic effects. It works by replenishing glutathione levels in the liver, thereby preventing liver damage. Another form is the granule for oral solution, which is often prescribed for respiratory conditions like chronic obstructive pulmonary disease (COPD) and cystic fibrosis. This form is mixed with water to create a solution that can be easily ingested, providing relief from mucus build-up and improving lung function. Oral inhalation is another method of administering NAC, particularly for patients with severe respiratory issues. This form allows the compound to be delivered directly to the lungs, offering targeted relief and improving breathing. Effervescent tablets are a popular choice for those who prefer a convenient and palatable way to consume NAC. These tablets dissolve in water, creating a fizzy drink that is easy to consume and quickly absorbed by the body. Effervescent tablets are often used as a dietary supplement to boost antioxidant levels and support overall health. Lastly, there are other forms of NAC available in the market, including capsules and powders, which offer flexibility in terms of dosage and administration. These forms are favored by individuals who incorporate NAC into their daily supplement regimen for its antioxidant and detoxification benefits. The diverse range of N-acetylcysteine products available in the global market reflects the compound's versatility and its ability to cater to various health needs and preferences.

Medicine, Nutritional Supplements, Others in the N-acetylcysteine- Global Market:

N-acetylcysteine is widely used in the global market across various sectors, including medicine, nutritional supplements, and other industries. In the medical field, NAC is primarily used as a mucolytic agent, helping to break down and thin mucus in the airways, making it easier for patients with respiratory conditions to breathe. It is commonly prescribed for chronic obstructive pulmonary disease (COPD), cystic fibrosis, and bronchitis. Additionally, NAC is used as an antidote for acetaminophen overdose, a critical application that can prevent severe liver damage and potentially save lives. Its ability to replenish glutathione levels in the liver makes it an essential treatment in emergency medicine. Beyond its medical applications, NAC is also popular in the nutritional supplement industry. It is marketed as an antioxidant supplement, promoting detoxification and supporting immune function. Many consumers take NAC supplements to enhance their overall health, protect against oxidative stress, and improve mental well-being. Studies have shown that NAC may have potential benefits in managing psychiatric disorders, such as depression and anxiety, further increasing its appeal as a supplement. In addition to its use in medicine and supplements, NAC is also utilized in other industries, such as cosmetics and food preservation. Its antioxidant properties make it a valuable ingredient in skincare products, where it helps to protect the skin from environmental damage and promote a youthful appearance. In the food industry, NAC is used as a preservative to extend the shelf life of products by preventing oxidation. The diverse applications of N-acetylcysteine across various sectors highlight its versatility and the growing demand for this compound in the global market. As awareness of its benefits continues to rise, the use of NAC is expected to expand, further solidifying its position as a valuable asset in health and wellness.

N-acetylcysteine- Global Market Outlook:

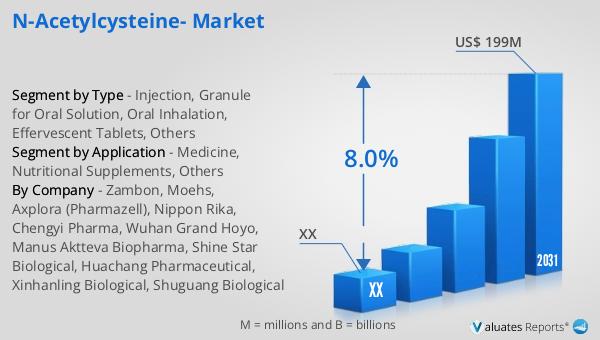

The global market for N-acetylcysteine was valued at approximately $117 million in 2024, with projections indicating a growth to around $199 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 8.0% from 2025 to 2031. The market is dominated by three major players: Zambon, Axplora, and Wuhan Grand Hoyo, which collectively hold about 64% of the market share. Europe stands as the largest market for N-acetylcysteine, accounting for approximately 47% of the global share. Following Europe, the Asia-Pacific region and North America hold significant portions of the market, with shares of 32% and 18%, respectively. Among the various product types, effervescent tablets represent the largest segment, making up 28% of the market. This data underscores the growing demand for N-acetylcysteine across different regions and product types, driven by its diverse applications and health benefits. The market's expansion is indicative of the increasing recognition of NAC's potential in promoting health and wellness, as well as its critical role in medical treatments. As the market continues to evolve, the key players and regions will likely play pivotal roles in shaping the future of N-acetylcysteine's global presence.

| Report Metric | Details |

| Report Name | N-acetylcysteine- Market |

| Forecasted market size in 2031 | US$ 199 million |

| CAGR | 8.0% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Zambon, Moehs, Axplora (Pharmazell), Nippon Rika, Chengyi Pharma, Wuhan Grand Hoyo, Manus Aktteva Biopharma, Shine Star Biological, Huachang Pharmaceutical, Xinhanling Biological, Shuguang Biological |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |