What is Vape- Global Market?

The global vape market is a rapidly evolving sector that has captured the attention of consumers and businesses worldwide. Vaping refers to the use of electronic devices, such as e-cigarettes, to inhale vaporized liquid, often containing nicotine, flavorings, and other chemicals. This market has seen significant growth due to increasing awareness of the potential health risks associated with traditional smoking and the perception of vaping as a less harmful alternative. The market is characterized by a wide range of products, including disposable e-cigarettes, rechargeable devices, and advanced personal vaporizers. Technological advancements have led to the development of more efficient and user-friendly devices, further driving market growth. Additionally, the introduction of various flavors and customizable options has attracted a diverse consumer base, from young adults to older smokers looking to quit. The global vape market is also influenced by regulatory changes, with governments worldwide implementing policies to control the sale and use of vaping products. Despite these challenges, the market continues to expand, driven by innovation and consumer demand for alternative nicotine delivery systems. As the industry evolves, it is expected to see further diversification in product offerings and increased competition among manufacturers.

E-vapor, Heated Not Burn in the Vape- Global Market:

E-vapor and heated not burn (HNB) products are two significant segments within the global vape market, each offering unique features and benefits to consumers. E-vapor products, commonly known as e-cigarettes or vapes, work by heating a liquid solution, often containing nicotine, to create an aerosol or vapor that users inhale. These devices come in various forms, including disposable e-cigarettes, pod systems, and advanced personal vaporizers, catering to different consumer preferences. E-vapor products are popular due to their perceived reduced harm compared to traditional cigarettes, as they do not involve combustion and the associated harmful byproducts. The availability of a wide range of flavors and nicotine strengths also appeals to a broad audience, from those seeking to quit smoking to recreational users. On the other hand, heated not burn products represent a newer category in the vape market. These devices heat tobacco to a temperature below combustion, releasing a nicotine-containing aerosol without burning the tobacco. This process is believed to produce fewer harmful chemicals than conventional smoking, making HNB products an attractive alternative for smokers looking to reduce their exposure to toxic substances. HNB products often mimic the experience of smoking a traditional cigarette more closely than e-vapor products, which can be a significant factor for smokers transitioning to these alternatives. The global market for e-vapor and HNB products is driven by technological advancements, changing consumer preferences, and regulatory developments. Manufacturers are continually innovating to improve device performance, battery life, and user experience, while also expanding their product portfolios to include a variety of flavors and nicotine levels. Regulatory frameworks play a crucial role in shaping the market landscape, with governments worldwide implementing policies to control the sale, marketing, and use of these products. Despite regulatory challenges, the e-vapor and HNB segments continue to grow, fueled by increasing consumer demand for alternative nicotine delivery systems. As the market evolves, it is expected to see further diversification in product offerings and increased competition among manufacturers, ultimately benefiting consumers with more choices and improved products.

in the Vape- Global Market:

The global vape market finds applications across various sectors, driven by the diverse needs and preferences of consumers. One of the primary applications is in smoking cessation, where vaping products serve as an alternative to traditional cigarettes. Many smokers turn to vaping as a means to reduce or quit smoking, attracted by the perception of reduced harm and the ability to control nicotine intake. The availability of nicotine-free options and a wide range of flavors further supports this application, providing smokers with a customizable experience that can aid in their transition away from combustible tobacco products. Another significant application of vaping products is in recreational use, particularly among young adults and non-smokers. The appeal of vaping as a trendy and socially acceptable activity has led to its adoption as a lifestyle choice for many individuals. The variety of flavors, sleek device designs, and the ability to perform tricks with vapor have contributed to the popularity of vaping in social settings. This recreational use has also spurred the growth of vape culture, with enthusiasts sharing their experiences and preferences through online communities and social media platforms. In addition to smoking cessation and recreational use, the vape market also finds applications in the medical and pharmaceutical sectors. Researchers are exploring the potential of vaping devices as delivery systems for therapeutic compounds, such as cannabinoids and other medications. The precise control over dosage and the rapid onset of effects make vaping an attractive option for patients seeking alternative methods of administration. This application is still in its early stages, but it holds promise for the future of personalized medicine and targeted drug delivery. The global vape market's diverse applications highlight its adaptability and potential for growth across various sectors. As the industry continues to evolve, it is likely to see further innovation and expansion into new areas, driven by consumer demand and technological advancements. The ongoing development of new products and applications will play a crucial role in shaping the future of the vape market, offering consumers a wide range of options to suit their individual needs and preferences.

Vape- Global Market Outlook:

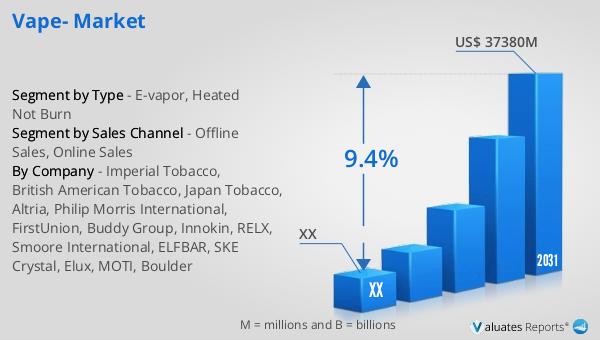

The global vape market is poised for significant growth in the coming years, with its value projected to increase substantially. In 2024, the market was estimated to be worth approximately $20,060 million, and by 2031, it is expected to reach a readjusted size of $37,380 million. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 9.4% during the forecast period from 2025 to 2031. North America stands out as the largest consumption region, accounting for about 57% of the global market. This dominance can be attributed to the region's early adoption of vaping products and the presence of key market players. In terms of product type, e-vapor is the largest market segment, holding a share of more than 94%. This segment's popularity is driven by the wide range of products available, from disposable e-cigarettes to advanced personal vaporizers, catering to diverse consumer preferences. When it comes to sales channels, offline sales dominate the market, with a share of approximately 83%. This preference for offline purchases can be linked to consumers' desire to physically inspect products and seek advice from knowledgeable staff before making a purchase. As the market continues to grow, it is expected to see further diversification in product offerings and increased competition among manufacturers, ultimately benefiting consumers with more choices and improved products.

| Report Metric | Details |

| Report Name | Vape- Market |

| Forecasted market size in 2031 | US$ 37380 million |

| CAGR | 9.4% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Sales Channel |

|

| By Region |

|

| By Company | Imperial Tobacco, British American Tobacco, Japan Tobacco, Altria, Philip Morris International, FirstUnion, Buddy Group, Innokin, RELX, Smoore International, ELFBAR, SKE Crystal, Elux, MOTI, Boulder |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |