What is Global Aluminum Hydroxide Market?

The Global Aluminum Hydroxide Market is a significant segment within the chemical industry, characterized by its diverse applications and growing demand across various sectors. Aluminum hydroxide, a white crystalline powder, is primarily used as a flame retardant, filler, and antacid. Its versatility stems from its chemical properties, which allow it to act as a neutralizing agent and a source of aluminum in various chemical reactions. The market for aluminum hydroxide is driven by its extensive use in industries such as plastics, pharmaceuticals, and chemicals. In the plastics industry, it is used as a flame retardant to enhance the safety of products by reducing their flammability. In pharmaceuticals, it serves as an antacid to relieve symptoms of indigestion and heartburn. The chemical industry utilizes aluminum hydroxide in the production of aluminum compounds and as a raw material in various processes. The market is influenced by factors such as technological advancements, regulatory policies, and the increasing demand for environmentally friendly and sustainable products. As industries continue to seek safer and more efficient materials, the demand for aluminum hydroxide is expected to grow, making it a crucial component in the global market landscape.

Industrial Grade, Pharmaceutical Grade, Others in the Global Aluminum Hydroxide Market:

The Global Aluminum Hydroxide Market is segmented into various grades, each serving distinct purposes and industries. Industrial Grade Aluminum Hydroxide is primarily used in manufacturing processes where its properties as a flame retardant and filler are highly valued. This grade is essential in the production of plastics, rubber, and coatings, where it enhances the material's resistance to fire and improves its mechanical properties. The industrial grade is also used in the production of glass and ceramics, where it acts as a fluxing agent, reducing the melting point of the raw materials and facilitating the formation of the final product. Its role in water treatment processes is also noteworthy, as it helps in the removal of impurities and the stabilization of pH levels. Pharmaceutical Grade Aluminum Hydroxide is of high purity and is used in the medical and healthcare industries. It is a key ingredient in antacid formulations, providing relief from acid indigestion and heartburn by neutralizing stomach acid. This grade is also used in the production of vaccines, where it acts as an adjuvant to enhance the body's immune response to the vaccine. The pharmaceutical grade is subject to stringent quality control measures to ensure its safety and efficacy in medical applications. Its use extends to the cosmetics industry, where it is used in the formulation of various skincare products due to its soothing and protective properties. Other grades of Aluminum Hydroxide include those used in specialized applications such as flame retardants for textiles and paper, as well as in the production of aluminum chemicals. These grades are tailored to meet the specific requirements of different industries, ensuring optimal performance and compatibility with other materials. The versatility of aluminum hydroxide across these grades highlights its importance in modern industrial and consumer applications. The market for these grades is influenced by factors such as technological advancements, regulatory standards, and the growing demand for sustainable and environmentally friendly products. As industries continue to innovate and seek safer alternatives, the demand for aluminum hydroxide across its various grades is expected to rise, reinforcing its position as a vital component in the global market.

Chemicals, Pharmaceuticals, Others in the Global Aluminum Hydroxide Market:

The Global Aluminum Hydroxide Market finds extensive usage across various sectors, including chemicals, pharmaceuticals, and others, due to its versatile properties and applications. In the chemical industry, aluminum hydroxide is primarily used as a raw material in the production of aluminum compounds such as aluminum sulfate and aluminum chloride. These compounds are essential in various industrial processes, including water treatment, paper manufacturing, and the production of synthetic zeolites. Aluminum hydroxide also serves as a flame retardant in the production of plastics and rubber, where it helps to reduce the flammability of materials and enhance their safety. Its role as a filler in coatings and adhesives further underscores its importance in the chemical sector. In the pharmaceutical industry, aluminum hydroxide is a critical component in the formulation of antacids, which are used to relieve symptoms of acid indigestion and heartburn. Its ability to neutralize stomach acid makes it an effective treatment for these conditions. Additionally, aluminum hydroxide is used as an adjuvant in vaccines, where it enhances the body's immune response to the vaccine, improving its efficacy. The pharmaceutical grade of aluminum hydroxide is subject to rigorous quality control measures to ensure its safety and effectiveness in medical applications. Its use in the cosmetics industry is also notable, where it is incorporated into skincare products for its soothing and protective properties. Beyond chemicals and pharmaceuticals, aluminum hydroxide is used in a variety of other applications. In the construction industry, it is used as a flame retardant in building materials, contributing to the safety and durability of structures. Its role in water treatment processes is also significant, as it aids in the removal of impurities and the stabilization of pH levels. The versatility of aluminum hydroxide extends to the production of glass and ceramics, where it acts as a fluxing agent, facilitating the formation of the final product. The demand for aluminum hydroxide in these diverse applications is driven by factors such as technological advancements, regulatory standards, and the increasing emphasis on sustainability and environmental safety. As industries continue to innovate and seek safer alternatives, the usage of aluminum hydroxide is expected to grow, reinforcing its importance in the global market landscape.

Global Aluminum Hydroxide Market Outlook:

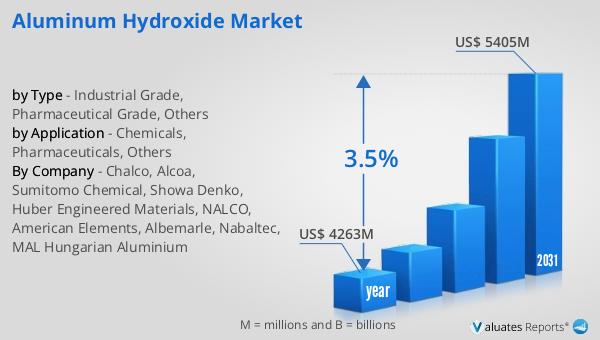

The global market for Aluminum Hydroxide was valued at approximately $4,263 million in 2024, and it is anticipated to expand to a revised size of around $5,405 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 3.5% over the forecast period. The steady increase in market size reflects the rising demand for aluminum hydroxide across various industries, driven by its versatile applications and beneficial properties. As a key component in sectors such as chemicals, pharmaceuticals, and construction, aluminum hydroxide's role in enhancing product safety and performance is increasingly recognized. The market's growth is also influenced by the ongoing shift towards sustainable and environmentally friendly materials, as aluminum hydroxide offers a non-toxic and effective solution for flame retardancy and other applications. Additionally, advancements in technology and manufacturing processes are expected to further boost the market, enabling the production of high-quality aluminum hydroxide that meets the stringent requirements of different industries. As the global economy continues to recover and industrial activities resume, the demand for aluminum hydroxide is likely to increase, supporting the market's positive outlook and reinforcing its significance in the global chemical industry.

| Report Metric | Details |

| Report Name | Aluminum Hydroxide Market |

| Accounted market size in year | US$ 4263 million |

| Forecasted market size in 2031 | US$ 5405 million |

| CAGR | 3.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Chalco, Alcoa, Sumitomo Chemical, Showa Denko, Huber Engineered Materials, NALCO, American Elements, Albemarle, Nabaltec, MAL Hungarian Aluminium |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |