What is Global Cloud Document Management Software Market?

The Global Cloud Document Management Software Market refers to the worldwide industry focused on providing digital solutions for managing documents via cloud technology. This market encompasses a range of software services that allow businesses and individuals to store, manage, and access documents online, eliminating the need for physical storage and enabling remote access. The software typically includes features such as document storage, version control, collaboration tools, and security measures to protect sensitive information. The growth of this market is driven by the increasing need for efficient document management solutions that support remote work and digital transformation initiatives. As businesses continue to digitize their operations, the demand for cloud-based document management systems is expected to rise, offering flexibility, scalability, and cost-effectiveness. This market is characterized by a diverse range of providers, from large tech companies to specialized software developers, each offering unique features and integrations to cater to various industry needs. The adoption of cloud document management software is particularly prevalent in sectors such as healthcare, finance, and education, where secure and efficient document handling is critical. Overall, the Global Cloud Document Management Software Market plays a crucial role in modernizing document management practices across the globe.

Public Cloud, Private Cloud, Hybrid Cloud in the Global Cloud Document Management Software Market:

In the realm of the Global Cloud Document Management Software Market, understanding the distinctions between public, private, and hybrid cloud solutions is essential for businesses seeking to optimize their document management strategies. Public cloud services are offered by third-party providers over the internet, allowing organizations to access and store their documents on shared infrastructure. This model is highly scalable and cost-effective, as users only pay for the resources they consume. Public clouds are ideal for businesses that require flexibility and do not have stringent data security requirements. However, concerns about data privacy and compliance can be a drawback for some organizations. On the other hand, private cloud solutions are dedicated environments tailored to a single organization. These clouds offer enhanced security and control, as the infrastructure is either hosted on-premises or by a third-party provider exclusively for the organization. Private clouds are suitable for businesses with strict regulatory requirements or those handling sensitive information, as they provide greater data protection and customization options. However, they can be more expensive to implement and maintain compared to public clouds. Hybrid cloud solutions combine elements of both public and private clouds, offering a balanced approach that allows organizations to leverage the benefits of both models. In a hybrid setup, businesses can store sensitive data in a private cloud while utilizing the public cloud for less critical operations. This flexibility enables organizations to optimize costs and resources while maintaining control over their most important data. Hybrid clouds are particularly advantageous for businesses with fluctuating workloads or those undergoing digital transformation, as they provide the agility to scale resources as needed. The choice between public, private, and hybrid cloud solutions in the Global Cloud Document Management Software Market depends on various factors, including an organization's size, industry, regulatory requirements, and budget. Each model offers unique advantages and challenges, making it crucial for businesses to carefully assess their needs and objectives before selecting the most suitable cloud strategy. As the market continues to evolve, advancements in cloud technology and security measures are expected to further enhance the capabilities and appeal of these cloud models, driving increased adoption across different sectors.

SMEs, Large Enterprises, Individuals in the Global Cloud Document Management Software Market:

The Global Cloud Document Management Software Market serves a wide range of users, including small and medium-sized enterprises (SMEs), large enterprises, and individuals, each benefiting from the unique advantages offered by cloud-based document management solutions. For SMEs, cloud document management software provides an affordable and scalable solution to manage their documents efficiently. These businesses often face budget constraints and lack the resources to invest in extensive IT infrastructure. Cloud-based solutions eliminate the need for costly hardware and maintenance, allowing SMEs to focus on their core operations. Additionally, the flexibility of cloud services enables SMEs to scale their document management capabilities as their business grows, ensuring they can adapt to changing needs without significant upfront investments. Large enterprises, on the other hand, benefit from the robust features and integrations offered by cloud document management software. These organizations often deal with vast amounts of data and require sophisticated tools to manage, store, and retrieve documents efficiently. Cloud solutions provide large enterprises with the ability to centralize their document management processes, improve collaboration across departments, and enhance data security through advanced encryption and access controls. Furthermore, the integration capabilities of cloud software allow large enterprises to connect their document management systems with other business applications, streamlining workflows and improving overall productivity. For individuals, cloud document management software offers a convenient and secure way to store and access personal documents from anywhere with an internet connection. Whether it's managing personal finances, storing important legal documents, or organizing digital media, individuals can benefit from the ease of use and accessibility provided by cloud solutions. The ability to share documents with others and collaborate in real-time also enhances personal productivity and communication. Overall, the Global Cloud Document Management Software Market caters to a diverse range of users, each leveraging the benefits of cloud technology to improve their document management practices. As the demand for digital solutions continues to grow, the market is expected to expand, offering even more innovative features and capabilities to meet the evolving needs of businesses and individuals alike.

Global Cloud Document Management Software Market Outlook:

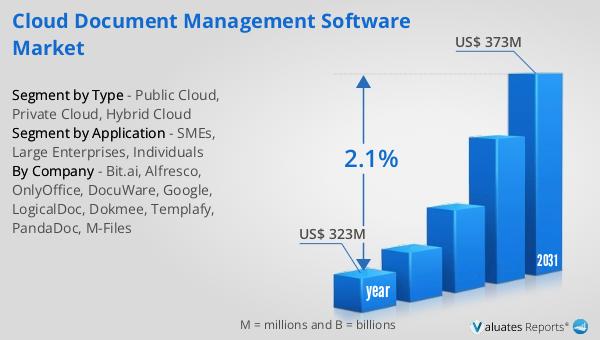

In 2024, the global market for Cloud Document Management Software was valued at approximately $323 million. Looking ahead, this market is anticipated to grow, reaching an estimated size of $373 million by 2031. This growth trajectory reflects a compound annual growth rate (CAGR) of 2.1% over the forecast period. This steady increase underscores the rising demand for cloud-based document management solutions as businesses and individuals continue to embrace digital transformation. The market's expansion is driven by the need for efficient, scalable, and secure document management systems that support remote work and collaboration. As organizations across various sectors seek to streamline their operations and enhance productivity, the adoption of cloud document management software is expected to rise. This growth also highlights the importance of cloud technology in modernizing document management practices, offering users the flexibility to access and manage their documents from anywhere with an internet connection. As the market evolves, advancements in cloud technology and security measures are likely to further enhance the capabilities and appeal of these solutions, driving increased adoption across different industries. Overall, the Global Cloud Document Management Software Market is poised for continued growth, reflecting the ongoing shift towards digital solutions in today's fast-paced business environment.

| Report Metric | Details |

| Report Name | Cloud Document Management Software Market |

| Accounted market size in year | US$ 323 million |

| Forecasted market size in 2031 | US$ 373 million |

| CAGR | 2.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Bit.ai, Alfresco, OnlyOffice, DocuWare, Google, LogicalDoc, Dokmee, Templafy, PandaDoc, M-Files |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |