What is Veterinary Surgical Otoscope - Global Market?

The Veterinary Surgical Otoscope is a specialized instrument used in veterinary medicine to examine the ears of animals. This tool is essential for diagnosing ear infections, blockages, and other ear-related issues in pets and livestock. The global market for veterinary surgical otoscopes is expanding as pet ownership increases and the demand for quality veterinary care rises. These otoscopes are designed to provide veterinarians with a clear view of the ear canal and eardrum, allowing for accurate diagnosis and treatment. The market is driven by technological advancements that have led to the development of more sophisticated and user-friendly otoscopes. Additionally, the growing awareness among pet owners about the importance of regular ear check-ups for their pets is contributing to the market's growth. As more people adopt pets and seek professional veterinary services, the demand for veterinary surgical otoscopes is expected to continue rising, making it a vital component of modern veterinary practice.

With Speculum, Without Speculum in the Veterinary Surgical Otoscope - Global Market:

Veterinary surgical otoscopes come in two main types: with speculum and without speculum. The speculum is a funnel-shaped attachment that helps to direct light and provide a clearer view of the ear canal. Otoscopes with speculum are commonly used in veterinary practices because they allow for a more detailed examination of the ear. The speculum can be adjusted to fit different sizes of ear canals, making it versatile for use with various animal species. This type of otoscope is particularly useful for diagnosing conditions such as ear infections, foreign bodies, and tumors. On the other hand, otoscopes without speculum are simpler in design and are often used for quick examinations or in situations where a detailed view is not necessary. These otoscopes are more portable and easier to use, making them ideal for fieldwork or emergency situations. Both types of otoscopes are essential tools in veterinary medicine, and the choice between them depends on the specific needs of the examination and the preference of the veterinarian. The global market for veterinary surgical otoscopes is influenced by factors such as technological advancements, increasing pet ownership, and the growing demand for quality veterinary care. As more people become aware of the importance of regular ear check-ups for their pets, the demand for these instruments is expected to rise. Additionally, the development of more advanced otoscopes with features such as digital imaging and wireless connectivity is likely to drive market growth. These innovations allow for more accurate diagnoses and improved treatment outcomes, making them attractive to veterinarians and pet owners alike. The veterinary surgical otoscope market is also impacted by regional factors, such as the prevalence of certain ear conditions in different animal populations and the availability of veterinary services. In regions with a high prevalence of ear infections or other ear-related issues, the demand for otoscopes is likely to be higher. Similarly, in areas where veterinary services are readily available and accessible, the market for otoscopes is expected to grow. Overall, the global market for veterinary surgical otoscopes is poised for growth as the demand for quality veterinary care continues to rise.

Hospital, Pet Shop, Others in the Veterinary Surgical Otoscope - Global Market:

The usage of veterinary surgical otoscopes spans various settings, including hospitals, pet shops, and other environments where animal care is provided. In veterinary hospitals, otoscopes are indispensable tools for diagnosing and treating ear conditions in animals. Veterinarians rely on these instruments to perform thorough examinations of the ear canal and eardrum, which are crucial for identifying infections, foreign bodies, and other issues. The use of otoscopes in hospitals is often accompanied by other diagnostic tools and procedures, allowing for comprehensive care and treatment planning. In pet shops, otoscopes may be used by trained staff to perform preliminary ear checks on animals before they are sold or adopted. This practice helps ensure that pets are healthy and free from ear-related issues, providing peace of mind to potential pet owners. Additionally, pet shop staff may use otoscopes to educate pet owners about the importance of regular ear care and the signs of potential problems. In other settings, such as animal shelters or rescue organizations, otoscopes are used to assess the health of animals upon intake and during routine check-ups. These organizations often deal with animals that have been neglected or abandoned, making regular health assessments crucial for their well-being. The use of otoscopes in these environments helps identify and address ear conditions early, improving the overall health and quality of life for the animals. Overall, the versatility and importance of veterinary surgical otoscopes make them essential tools in various animal care settings, contributing to the health and well-being of animals worldwide.

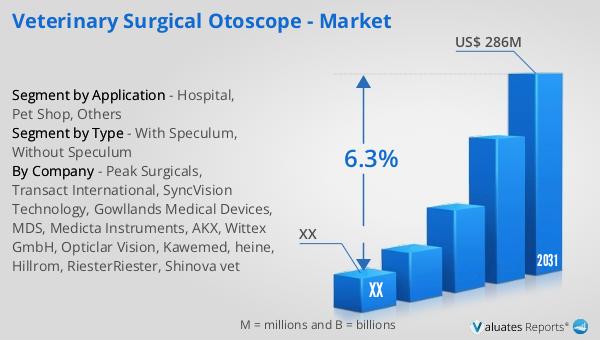

Veterinary Surgical Otoscope - Global Market Outlook:

The global market for veterinary surgical otoscopes was valued at approximately $185 million in 2024. It is projected to grow to a revised size of $286 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.3% during the forecast period from 2025 to 2031. This growth is driven by several factors, including the increasing demand for quality veterinary care and the rising awareness among pet owners about the importance of regular ear check-ups for their pets. As more people adopt pets and seek professional veterinary services, the demand for veterinary surgical otoscopes is expected to continue rising. Additionally, technological advancements in otoscope design and functionality are contributing to market growth. The development of more advanced otoscopes with features such as digital imaging and wireless connectivity allows for more accurate diagnoses and improved treatment outcomes, making them attractive to veterinarians and pet owners alike. The market is also influenced by regional factors, such as the prevalence of certain ear conditions in different animal populations and the availability of veterinary services. In regions with a high prevalence of ear infections or other ear-related issues, the demand for otoscopes is likely to be higher. Similarly, in areas where veterinary services are readily available and accessible, the market for otoscopes is expected to grow. Overall, the global market for veterinary surgical otoscopes is poised for growth as the demand for quality veterinary care continues to rise.

| Report Metric | Details |

| Report Name | Veterinary Surgical Otoscope - Market |

| Forecasted market size in 2031 | US$ 286 million |

| CAGR | 6.3% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Peak Surgicals, Transact International, SyncVision Technology, Gowllands Medical Devices, MDS, Medicta Instruments, AKX, Wittex GmbH, Opticlar Vision, Kawemed, heine, Hillrom, RiesterRiester, Shinova vet |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |