What is Global AMOLED Screens Market?

The Global AMOLED Screens Market is a rapidly evolving sector within the display technology industry. AMOLED, which stands for Active Matrix Organic Light Emitting Diode, is a type of display technology that offers superior image quality, including better contrast, faster response times, and more vibrant colors compared to traditional LCD screens. This technology is increasingly being adopted across various consumer electronics due to its advantages, such as being thinner, lighter, and more flexible. The market for AMOLED screens is driven by the growing demand for high-quality displays in smartphones, televisions, wearable devices, and other electronic gadgets. As manufacturers continue to innovate and improve AMOLED technology, the market is expected to expand significantly. The increasing consumer preference for devices with better display quality and the ongoing advancements in AMOLED technology are key factors contributing to the growth of this market. Additionally, the shift towards more energy-efficient and environmentally friendly display solutions is further propelling the adoption of AMOLED screens globally. As a result, the Global AMOLED Screens Market is poised for substantial growth in the coming years, driven by technological advancements and increasing consumer demand for superior display quality.

AMOLED hard screen, AMOLED soft screen in the Global AMOLED Screens Market:

AMOLED screens are categorized into two main types: hard screens and soft screens, each with distinct characteristics and applications. Hard AMOLED screens are typically more rigid and are used in devices where durability and structural integrity are paramount. These screens are often found in products that require a sturdy display, such as certain models of smartphones and tablets. The hard AMOLED screens are known for their robustness and ability to withstand physical stress, making them ideal for devices that are frequently handled or subjected to rough conditions. On the other hand, soft AMOLED screens are more flexible and are used in applications where the display needs to be curved or bent. This flexibility allows for innovative designs and applications, such as foldable smartphones and wearable devices that conform to the shape of the user's wrist. The soft AMOLED screens are also lighter and thinner, contributing to the sleek and modern design of contemporary electronic devices. In the Global AMOLED Screens Market, the demand for both hard and soft screens is growing, driven by the increasing consumer preference for devices with advanced display features. Manufacturers are investing in research and development to enhance the performance and durability of both types of screens, ensuring they meet the evolving needs of consumers. The versatility of AMOLED technology, combined with its superior display quality, makes it a popular choice among manufacturers and consumers alike. As the market continues to grow, we can expect to see further innovations in both hard and soft AMOLED screens, leading to even more diverse applications and improved user experiences.

Mobile phone, Wearable device, Helmet type VR, TV, Other in the Global AMOLED Screens Market:

The Global AMOLED Screens Market finds extensive usage across various sectors, including mobile phones, wearable devices, helmet-type VR, TVs, and other electronic gadgets. In mobile phones, AMOLED screens are highly valued for their vibrant colors, deep blacks, and energy efficiency. These screens enhance the visual experience for users, making them a popular choice for high-end smartphones. The ability of AMOLED screens to produce sharp and clear images even in bright sunlight is another reason for their widespread adoption in mobile devices. In wearable devices, such as smartwatches and fitness trackers, AMOLED screens offer the advantage of being lightweight and flexible, allowing for comfortable wearability. The superior display quality of AMOLED screens also enhances the user interface of these devices, making them more appealing to consumers. Helmet-type VR devices benefit from AMOLED screens due to their fast response times and high refresh rates, which are crucial for providing an immersive virtual reality experience. The deep blacks and vibrant colors of AMOLED screens contribute to a more realistic and engaging VR environment. In the television sector, AMOLED screens are used in high-end models to deliver exceptional picture quality with vivid colors and excellent contrast ratios. The thin and lightweight nature of AMOLED screens also allows for sleek and modern TV designs. Beyond these applications, AMOLED screens are also used in other electronic devices, such as digital cameras, laptops, and automotive displays, where high-quality visuals are essential. The versatility and superior performance of AMOLED screens make them a preferred choice across various industries, driving the growth of the Global AMOLED Screens Market.

Global AMOLED Screens Market Outlook:

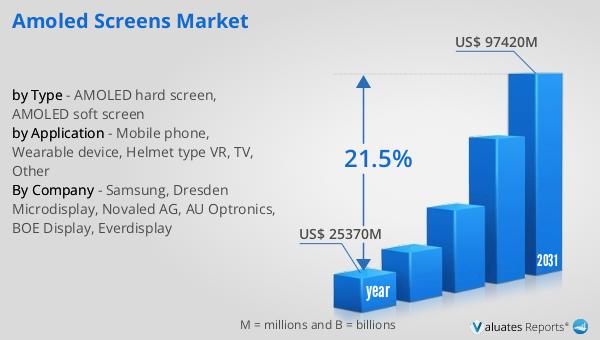

The global market for AMOLED screens was valued at approximately $25.37 billion in 2024, with projections indicating a significant increase to around $97.42 billion by 2031. This growth represents a compound annual growth rate (CAGR) of 21.5% over the forecast period. AMOLED technology, a specific type of thin-film display, has seen substantial advancements and adoption in recent years. Before 2016, the production capacity for flexible AMOLED screens was predominantly concentrated in South Korea, with Samsung holding over 90% of the market share. This dominance was due to Samsung's early investment in AMOLED technology and its ability to produce high-quality displays at scale. However, as the market has expanded, other manufacturers have entered the scene, contributing to the diversification and growth of the AMOLED screens market. The increasing demand for high-quality displays in consumer electronics, coupled with technological advancements, has fueled the market's rapid expansion. As more companies invest in AMOLED technology and production capabilities, the market is expected to continue its upward trajectory, offering new opportunities for innovation and growth. The shift towards more energy-efficient and environmentally friendly display solutions is also driving the adoption of AMOLED screens globally, further contributing to the market's positive outlook.

| Report Metric | Details |

| Report Name | AMOLED Screens Market |

| Accounted market size in year | US$ 25370 million |

| Forecasted market size in 2031 | US$ 97420 million |

| CAGR | 21.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Samsung, Dresden Microdisplay, Novaled AG, AU Optronics, BOE Display, Everdisplay |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |