What is Global PN and PIN Photodiode Market?

The Global PN and PIN Photodiode Market is a significant segment within the broader photodetector industry, focusing on devices that convert light into electrical signals. These photodiodes are essential in various applications due to their ability to detect light with high precision and speed. The market encompasses a wide range of industries, including telecommunications, consumer electronics, automotive, and medical sectors, among others. PN photodiodes are typically used in applications where cost-effectiveness is a priority, while PIN photodiodes are preferred for their superior performance in terms of speed and sensitivity. The market is driven by the increasing demand for high-speed internet, advancements in medical imaging technologies, and the growing adoption of photodiodes in automotive safety systems. As technology continues to evolve, the Global PN and PIN Photodiode Market is expected to expand, offering new opportunities for innovation and application across various sectors. The market's growth is also supported by ongoing research and development efforts aimed at enhancing the efficiency and functionality of photodiodes, making them more versatile and effective in meeting the needs of modern technology.

PIN Photodiodes, PN Photodiodes in the Global PN and PIN Photodiode Market:

PIN photodiodes and PN photodiodes are two types of semiconductor devices used to detect light and convert it into an electrical signal. PIN photodiodes are characterized by their structure, which includes an intrinsic layer sandwiched between the p-type and n-type layers. This intrinsic layer enhances the device's ability to absorb light and improves its response time, making PIN photodiodes highly suitable for high-speed and high-frequency applications. They are commonly used in fiber optic communications, where rapid data transmission is crucial, as well as in medical imaging equipment, where precise detection of light is necessary. On the other hand, PN photodiodes have a simpler structure, consisting of a p-n junction without the intrinsic layer. While they may not offer the same level of performance as PIN photodiodes, PN photodiodes are often more cost-effective and are used in applications where speed and sensitivity are less critical. They are commonly found in consumer electronics, such as remote controls and light meters, where their ability to detect light is sufficient for the intended purpose. The choice between PIN and PN photodiodes depends largely on the specific requirements of the application, including factors such as speed, sensitivity, and cost. In the Global PN and PIN Photodiode Market, both types of photodiodes play a crucial role, catering to a diverse range of industries and applications. As technology continues to advance, the demand for both PIN and PN photodiodes is expected to grow, driven by the increasing need for efficient and reliable light detection solutions. This growth is further supported by ongoing research and development efforts aimed at improving the performance and functionality of photodiodes, making them more versatile and effective in meeting the needs of modern technology.

Aerospace and Defense, Consumer Electronics, Automotive, Medical, Other in the Global PN and PIN Photodiode Market:

The Global PN and PIN Photodiode Market finds extensive usage across various sectors, including aerospace and defense, consumer electronics, automotive, medical, and other industries. In the aerospace and defense sector, photodiodes are used in a variety of applications, such as missile guidance systems, laser range finders, and optical communication systems. Their ability to detect light with high precision and speed makes them ideal for these applications, where accuracy and reliability are critical. In consumer electronics, photodiodes are commonly used in devices such as remote controls, light meters, and optical sensors. Their ability to detect light and convert it into an electrical signal is essential for the functioning of these devices, making them an integral part of the consumer electronics industry. In the automotive sector, photodiodes are used in a variety of applications, including adaptive lighting systems, collision avoidance systems, and driver assistance systems. Their ability to detect light and respond quickly is crucial for the safe and efficient operation of these systems, making them an essential component of modern automotive technology. In the medical field, photodiodes are used in a range of applications, including medical imaging equipment, pulse oximeters, and blood glucose monitors. Their ability to detect light with high precision and sensitivity is essential for the accurate diagnosis and monitoring of medical conditions, making them a vital part of the medical industry. In addition to these sectors, photodiodes are also used in a variety of other applications, such as environmental monitoring, industrial automation, and telecommunications. Their versatility and reliability make them an essential component of modern technology, driving the growth of the Global PN and PIN Photodiode Market.

Global PN and PIN Photodiode Market Outlook:

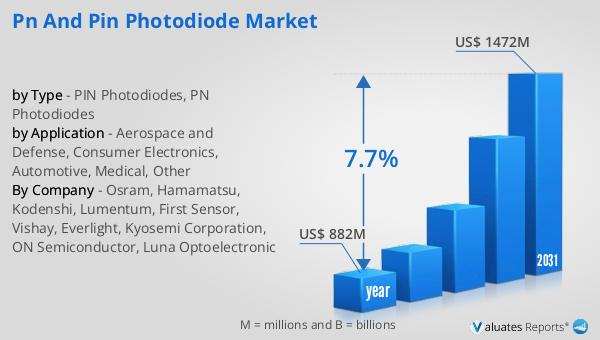

The global market for PN and PIN photodiodes was valued at approximately $882 million in 2024, and it is anticipated to expand significantly, reaching an estimated $1,472 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 7.7% over the forecast period. The increasing demand for high-speed internet, advancements in medical imaging technologies, and the growing adoption of photodiodes in automotive safety systems are key factors driving this market expansion. As technology continues to evolve, the Global PN and PIN Photodiode Market is expected to offer new opportunities for innovation and application across various sectors. The market's growth is also supported by ongoing research and development efforts aimed at enhancing the efficiency and functionality of photodiodes, making them more versatile and effective in meeting the needs of modern technology. This positive market outlook reflects the increasing importance of photodiodes in a wide range of applications, from telecommunications to consumer electronics, automotive, and medical sectors. As the demand for efficient and reliable light detection solutions continues to rise, the Global PN and PIN Photodiode Market is poised for significant growth in the coming years.

| Report Metric | Details |

| Report Name | PN and PIN Photodiode Market |

| Accounted market size in year | US$ 882 million |

| Forecasted market size in 2031 | US$ 1472 million |

| CAGR | 7.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Osram, Hamamatsu, Kodenshi, Lumentum, First Sensor, Vishay, Everlight, Kyosemi Corporation, ON Semiconductor, Luna Optoelectronic |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |