What is Global FM Transmitter Market?

The Global FM Transmitter Market refers to the worldwide industry involved in the production, distribution, and sale of FM transmitters. FM transmitters are devices that convert audio signals into frequency modulated (FM) radio waves, which can then be broadcast over a specific range. These devices are crucial for radio broadcasting, allowing radio stations to transmit audio content to listeners over the airwaves. The market encompasses various types of FM transmitters, including low power, medium power, and high power transmitters, each serving different broadcasting needs and coverage areas. The demand for FM transmitters is driven by the need for reliable and efficient broadcasting solutions, especially in regions where radio remains a primary source of information and entertainment. The market is influenced by technological advancements, regulatory standards, and the growing popularity of digital broadcasting. As radio continues to be a vital medium for communication, the Global FM Transmitter Market plays a significant role in ensuring that broadcasters can reach their audiences effectively. The market is characterized by a diverse range of manufacturers and suppliers, offering products that cater to various broadcasting requirements and budgets.

Low Power FM Transmitter, Medium Power FM Transmitter, High Power FM Transmitter in the Global FM Transmitter Market:

In the Global FM Transmitter Market, FM transmitters are categorized based on their power output, which determines their coverage area and application. Low Power FM Transmitters are typically used for small-scale broadcasting needs, such as community radio stations, educational institutions, and local events. These transmitters have a limited range, usually covering a few kilometers, making them ideal for localized broadcasting. They are cost-effective and easy to operate, making them accessible to smaller organizations and communities. Medium Power FM Transmitters, on the other hand, are designed for larger coverage areas, such as city-wide or regional broadcasting. These transmitters offer a balance between power output and cost, providing a wider reach without the high expenses associated with high power transmitters. They are commonly used by regional radio stations and broadcasters looking to expand their audience reach. High Power FM Transmitters are the most powerful in the market, capable of covering vast areas, including entire countries or multiple regions. These transmitters are used by national broadcasters and large radio networks that require extensive coverage to reach a broad audience. High power transmitters are more expensive and require significant infrastructure and maintenance, but they offer unparalleled reach and signal quality. The choice of transmitter power depends on various factors, including the target audience, geographical area, and budget constraints. Each type of transmitter plays a crucial role in the Global FM Transmitter Market, catering to different broadcasting needs and ensuring that radio remains a vital medium for communication and entertainment.

Radio Station (National, Provincial, City, County), Rural and Other Radio Stations in the Global FM Transmitter Market:

The Global FM Transmitter Market finds extensive usage across various types of radio stations, each with unique broadcasting needs and challenges. National radio stations, for instance, require high power FM transmitters to ensure their signal reaches every corner of the country. These stations often broadcast a wide range of content, including news, music, and talk shows, and rely on high power transmitters to maintain a strong and consistent signal across vast geographical areas. Provincial and city radio stations, on the other hand, may opt for medium power FM transmitters, which provide sufficient coverage for their target audience without the high costs associated with national broadcasting. These stations often focus on regional content, catering to the specific interests and needs of their local listeners. County and rural radio stations typically use low power FM transmitters, which are ideal for covering smaller areas and serving niche audiences. These stations play a crucial role in providing localized content, such as community news, local events, and cultural programming, which may not be covered by larger broadcasters. In addition to traditional radio stations, the Global FM Transmitter Market also serves other broadcasting needs, such as emergency communication systems, educational institutions, and religious organizations. These entities use FM transmitters to reach specific audiences with targeted content, ensuring that important information is disseminated effectively. The versatility and adaptability of FM transmitters make them an essential tool for broadcasters of all sizes, enabling them to connect with their audiences and deliver content that informs, entertains, and engages.

Global FM Transmitter Market Outlook:

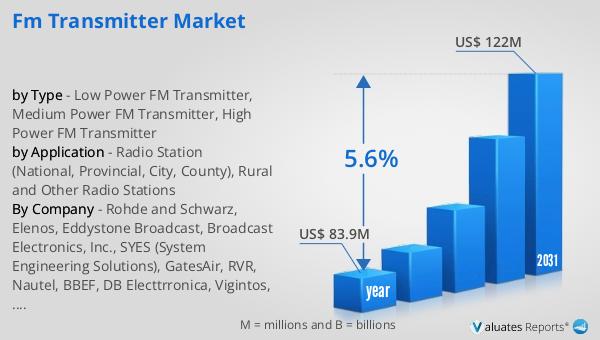

The global FM Transmitter Market was valued at approximately $83.9 million in 2024, and it is anticipated to grow significantly over the coming years. By 2031, the market is expected to reach an estimated size of $122 million, reflecting a compound annual growth rate (CAGR) of 5.6% during the forecast period. This growth can be attributed to several factors, including the ongoing demand for reliable broadcasting solutions, technological advancements in transmitter technology, and the continued importance of radio as a medium for communication and entertainment. As more regions around the world invest in improving their broadcasting infrastructure, the demand for FM transmitters is likely to increase, driving market growth. Additionally, the rise of digital broadcasting and the integration of FM transmitters with other communication technologies are expected to create new opportunities for market expansion. The market's growth trajectory underscores the enduring relevance of FM transmitters in the global broadcasting landscape, as they continue to play a vital role in ensuring that radio remains a powerful and accessible medium for reaching audiences worldwide.

| Report Metric | Details |

| Report Name | FM Transmitter Market |

| Accounted market size in year | US$ 83.9 million |

| Forecasted market size in 2031 | US$ 122 million |

| CAGR | 5.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Rohde and Schwarz, Elenos, Eddystone Broadcast, Broadcast Electronics, Inc., SYES (System Engineering Solutions), GatesAir, RVR, Nautel, BBEF, DB Electtrronica, Vigintos, Worldcast Ecreso, Vimesa, ZHC(China)Digital Equipment, OMB, Tredess, Sielco, Electrolink S.r.l, RFE Broadcast, WaveArt |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |