What is Global RF Spectrum Recording and Playback System Market?

The Global RF Spectrum Recording and Playback System Market is a specialized segment within the broader technology and telecommunications industry. This market focuses on systems that can capture, store, and reproduce radio frequency (RF) signals. These systems are crucial for various applications, including testing and development of wireless communication devices, spectrum monitoring, and interference analysis. The ability to record and playback RF signals allows engineers and researchers to analyze and troubleshoot wireless systems effectively. This market is driven by the increasing demand for advanced communication systems and the need for efficient spectrum management. As wireless technologies continue to evolve, the importance of RF spectrum recording and playback systems is expected to grow, providing valuable tools for industries such as aerospace, defense, telecommunications, and broadcasting. These systems help ensure that wireless devices operate efficiently and without interference, which is critical in today's interconnected world. The market is characterized by technological advancements and innovations aimed at improving the accuracy, speed, and capacity of these systems. Companies operating in this market are continually developing new solutions to meet the growing needs of their customers.

Maximum Frequency Less than 3 GHz, Maximum Frequency between 3-13 GHz, Maximum Frequency between 13-26.5 GHz, Maximum Frequency More than 26.5 GHz in the Global RF Spectrum Recording and Playback System Market:

The Global RF Spectrum Recording and Playback System Market is categorized based on the maximum frequency capabilities of the systems, which are crucial for different applications. Systems with a maximum frequency of less than 3 GHz are typically used for applications that require lower frequency ranges, such as certain types of broadcasting and telecommunications. These systems are often more affordable and are suitable for applications where high-frequency capabilities are not necessary. On the other hand, systems with a maximum frequency between 3-13 GHz are used in more advanced applications, including some defense and aerospace applications. These systems offer a balance between cost and performance, making them suitable for a wide range of uses. Systems with a maximum frequency between 13-26.5 GHz are used in more specialized applications, such as certain types of radar and satellite communications. These systems are more expensive but offer higher performance and are capable of handling more complex signals. Finally, systems with a maximum frequency of more than 26.5 GHz are used in the most advanced applications, including cutting-edge research and development in telecommunications and defense. These systems are the most expensive but offer the highest performance and are capable of handling the most complex signals. The choice of system depends on the specific needs of the application, with higher frequency systems offering greater capabilities but at a higher cost. As technology continues to advance, the demand for higher frequency systems is expected to grow, driving innovation and development in this market. Companies operating in this market are continually developing new solutions to meet the growing needs of their customers, with a focus on improving the accuracy, speed, and capacity of these systems.

Aerospace, Defense, Telecommunications, Broadcasting, Scientific Research Institution, Others in the Global RF Spectrum Recording and Playback System Market:

The Global RF Spectrum Recording and Playback System Market finds applications across various sectors, each with unique requirements and challenges. In the aerospace industry, these systems are used for testing and development of communication systems, ensuring that aircraft can communicate effectively and without interference. They are also used in the development of radar systems, which are critical for navigation and safety. In the defense sector, RF spectrum recording and playback systems are used for a wide range of applications, including electronic warfare, surveillance, and communication. These systems help ensure that military communication systems are secure and reliable, which is critical for national security. In the telecommunications industry, these systems are used for testing and development of wireless communication devices, ensuring that they operate efficiently and without interference. They are also used for spectrum monitoring, helping to manage the increasingly crowded radio frequency spectrum. In the broadcasting industry, RF spectrum recording and playback systems are used to ensure that broadcasts are transmitted clearly and without interference. They are also used for testing and development of new broadcasting technologies. In scientific research institutions, these systems are used for a wide range of applications, including research and development of new communication technologies and studying the effects of radio frequency signals on various materials and systems. Finally, in other industries, RF spectrum recording and playback systems are used for a wide range of applications, including testing and development of new technologies and ensuring that communication systems operate efficiently and without interference. As technology continues to advance, the demand for these systems is expected to grow, driving innovation and development in this market. Companies operating in this market are continually developing new solutions to meet the growing needs of their customers, with a focus on improving the accuracy, speed, and capacity of these systems.

Global RF Spectrum Recording and Playback System Market Outlook:

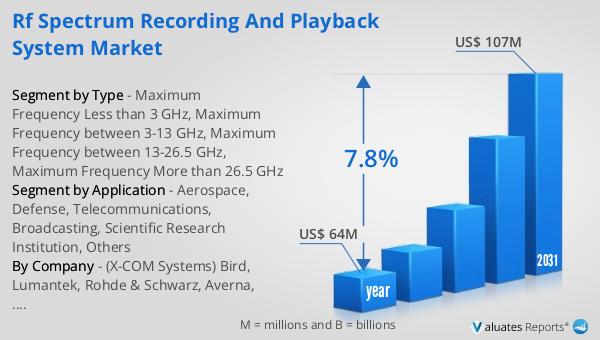

The global market for RF Spectrum Recording and Playback System was valued at $64 million in 2024 and is anticipated to expand to a revised size of $107 million by 2031, reflecting a compound annual growth rate (CAGR) of 7.8% during the forecast period. This growth is indicative of the increasing demand for advanced RF spectrum recording and playback systems across various industries. The market's expansion is driven by the need for efficient spectrum management and the development of new wireless communication technologies. As industries such as aerospace, defense, telecommunications, and broadcasting continue to evolve, the demand for these systems is expected to grow. Companies operating in this market are focused on developing new solutions to meet the growing needs of their customers, with a focus on improving the accuracy, speed, and capacity of these systems. The market is characterized by technological advancements and innovations aimed at improving the performance of these systems. As the demand for higher frequency systems continues to grow, companies are investing in research and development to create new solutions that meet the needs of their customers. The market's growth is also driven by the increasing complexity of wireless communication systems and the need for efficient spectrum management. As the world becomes more interconnected, the importance of RF spectrum recording and playback systems is expected to grow, providing valuable tools for industries such as aerospace, defense, telecommunications, and broadcasting.

| Report Metric | Details |

| Report Name | RF Spectrum Recording and Playback System Market |

| Accounted market size in year | US$ 64 million |

| Forecasted market size in 2031 | US$ 107 million |

| CAGR | 7.8% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | (X-COM Systems) Bird, Lumantek, Rohde & Schwarz, Averna, Spirent Federal Systems, Tektronix, Sinolink, Wideband Systems, Inc, Giga-Tronics, IZT GmbH, Novator Solutions, CRFS, Vitrek, Pentek, Sample Shanghai, Chengdu KSW Technologies, Chengdu .Jiujin, ADIVIC, Hunan Satellite Navigation Information Technology Co., Ltd., SignalEdge, TRANSCOM, Anritsu, Deviser Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |